Signs of recovery in smartphone and computer demand have yet to provide the next tailwind for chip stocks as they languish below the heights of this year’s artificial intelligence rally.

Whether retirement savers in TDFs know it or not, and I presume most don't, they are mindlessly investing their wealth.

In smart beta, we find that factor returns—net of changes in valuation levels—are much lower than recent performance suggests. In fact, many of the most popular new factors (some 458 at last count) have succeeded solely because they have become more expensive.

It’s been a great year for alternative income strategies as inflation, interest rate, and recession risk fears dominated markets. Garrett Paolella of NEOS and Christian Magoon of Amplify ETFs joined VettaFi’s Tom Lydon to discuss alternative income opportunities at the Income Strategy Symposium hosted by VettaFi on October 27.

The US Federal Reserve thinks it can take a break. As Fed officials see it, they need only sit back and wait while the monetary tightening they’ve already done gradually takes hold, slowing the economy and pushing inflation back down to the central bank’s 2% target.

Recently, I was asked by a client what my return expectations are for the next three years.

The US Treasury increased its planned sales of longer-term securities by slightly less than most major dealers expected in its quarterly debt-issuance plan, in a move that signals officials may be concerned about the surge in yields over the past several months.

Yields are at some of their highest levels in over a decade. This means that if you own fixed income in your portfolio, there is a good chance that you are seeing unrealized losses on your monthly statements (fixed income math = yields higher, prices lower).

The renewed opportunity set in fixed income is enabling investors to achieve attractive returns while taking on less risk.

Michael Gladchun, Associate Portfolio Manager, estimates underlying core PCE is already running at or near a 2% annualized inflation rate, and he sees progress ongoing if imbalances continue to normalize.

To have a shot at taming inflation, the Federal Reserve is intent on tightening financial conditions across the economy. But they haven’t made much of a dent in corporate America yet.

The US Treasury reduced its estimate for federal borrowing for the current quarter thanks to stronger-than-expected revenues, offering some relief for investors concerned about the rapidly widening fiscal deficit.

US blue-chip companies unleashed a wave of bond sales on Monday as borrowers look to sell new debt in a week jam-packed with bond auctions, central bank meetings and fresh economic data.

The yield on 10-year Treasuries went above 5% last week for the first time since July 2007, when the first Transformers movie was topping the box office and the Dow Jones Industrial Average surpassed 14,000 for the first time in history.

With the Federal Reserve poised to change direction, investors who have been investing in very short-term securities may soon face "reinvestment risk."

With 10-year Treasury yields hovering around 4.84%, the flirtation with 5% is ongoing and dangerous, spooking many fixed income investors in the process.

In our latest fixed income insight, we highlight four compelling investments for the remainder of 2023 and into 2024.

Much like Halloween, it has been a scary time for investors.

Credit volumes witnessed some strong highs and lows in the third quarter. Notably, July—a month where trading volumes are generally steady—saw very inconsistent flows over the month. September, meanwhile, followed historical trends with an increase in primary market supply, reflecting higher volumes in the secondary.

US stocks carry too much risk and buying Treasuries will pay off, according to M&G Plc as the $402 billion fund house navigates the brutal selloff in global markets.

Bitcoin has jumped on bets that the first US exchange-traded funds investing directly in the token are set to be approved. The question now is whether an actual green light for the products would spur some profit-taking.

Rising yields have undoubtedly done a number on bond prices, but they open up bearish opportunities in certain inverse leverage exchange traded funds (ETFs).

Embattled debt investors like the look of 5% Treasury yields as they weigh the risk-versus-reward scales for the world’s biggest bond market.

There are periods of time in the investing world when contradictions and disagreement among “experts” run rampant. Often, those periods tend to coincide with inflection points in cycles, although you only really know that with the benefit of hindsight, in my opinion.

Private credit is being sought—with the goals of income and capital preservation—to achieve real capital growth and drive portfolio returns among retail and institutional clients alike.

Amazon.com Inc.’s run as one of the best stocks this year will likely come down to the performance of a single business line: cloud computing.

As 2023 enters the home stretch, I reflect on asset class performance for the year and discuss what my firm’s models are saying for the next 12 months.

While the article focuses mainly on the rise in bond yields, it applies to several current market events.

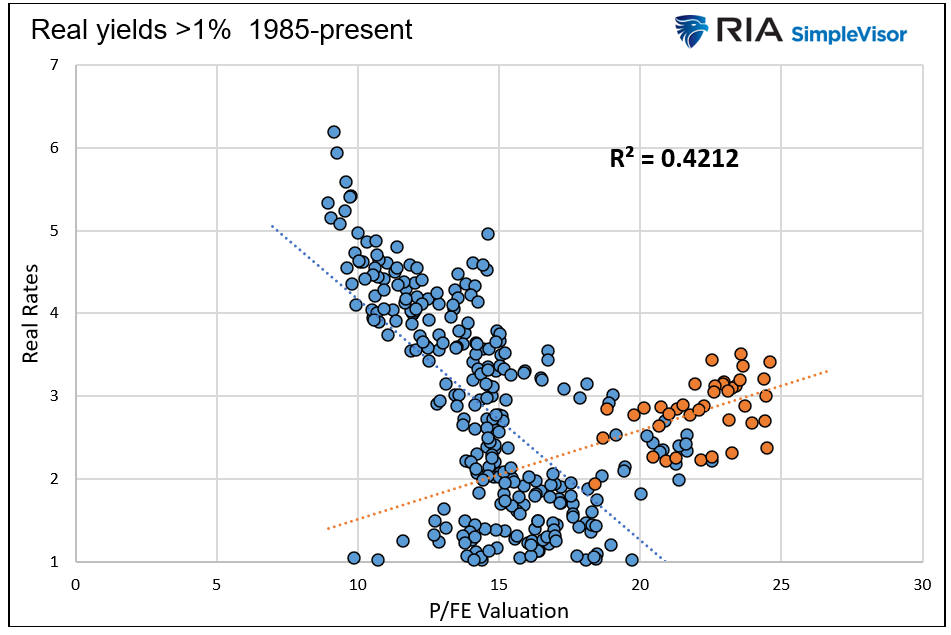

The relationship and the recent divergence between real rates and stock valuations is critical. Be ready for the historical trend to reassert itself.

In the fiscal year that just ended, the US government borrowed $1.7 trillion, more than 6% of gross domestic product. Bear in mind, that was with an economy running hot, with high inflation and more than full employment.

Municipal-bond yields at the highest in more than a decade are spurring optimism on the part of investment managers, who have been dealing with persistent fund outflows this year as the market has struggled along with the rest of fixed income.

The worst selloff of longer-term Treasuries in more than four decades is putting a spotlight on the market’s biggest missing buyer: the Federal Reserve.

Investors are accustomed to getting a snapshot of the market by looking at the latest index statistics. But today, average spreads and yields for investment-grade corporate bonds are deceptive. A look under the hood reveals that intermediate-maturity corporates are a much more compelling opportunity than long-maturity ones.

Lately, Federal Reserve officials have been paying greater attention to financial conditions – that is, to the influence that market phenomena such as stock prices, bond yields and housing prices have on economic activity, above and beyond the effect of the short-term interest rates that the central bank controls directly.

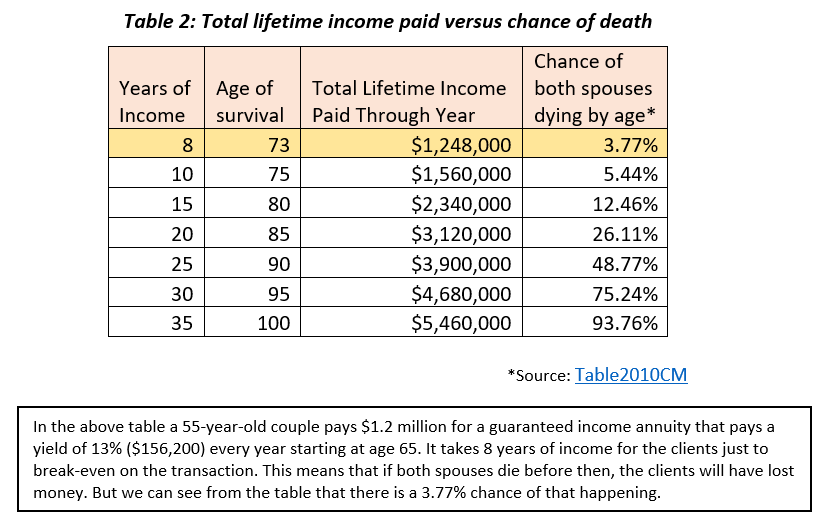

With interest rates at near 20-year highs, guaranteed lifetime income locks in those rates for the rest of one’s life, creating better retirement outcomes.

Wild swings in the “world’s safest asset” are once again acting as a driver for volatility across global markets.

Corporate America’s spending on share buybacks, a driver of the US stock market rally for over a decade, is slowing in the face of higher-for-longer interest rates and an uncertain economic backdrop.

On Monday, the 10-year Treasury yield climbed over 5%, a 16-year high. It’s a level few would have predicted during the long run of rock-bottom interest rates that followed the Great Financial Crisis.

Tight lending standards and rising yields, along with concern about an approaching turn in the business cycle, have put opportunistic credit in the spotlight. But what, exactly, does opportunistic credit mean? Here’s how we look at it—and what we think it may offer investors.

Greater stability in US Treasuries is needed for the smooth functioning of other segments of the financial market, housing and the economy more broadly, both in America and beyond.

Restrictive monetary conditions, from higher yields and tighter lending conditions, are the Fed’s “Waterloo.”

The odds of a year-end rally in US stocks are fading as investors face a multitude of risks from elevated profit estimates to the Federal Reserve’s policy tightening, according to Morgan Stanley’s Michael Wilson.

It feels like Groundhog Day, with yet another challenging quarter for muni investors. The index was down about 4%, bringing year-to-date returns to –1.4% for the year. So what happened in August and September?

Term premiums have been on the rise, but should investors be concerned? Stephen Dover, Head of Franklin Templeton Institute, explains what term premiums are, and why they are worth paying attention to.

The muni yield curve has been inverted before, but not for any meaningful length of time—until now. With yields on short-term muni bonds still significantly higher than those on intermediate-term munis, what’s an investor to do?

While surface-level economic data appear resilient, details below the surface are mixed.

Investor positioning in stocks has become so bearish that it’s triggered a “contrarian buy signal” in a custom Bank of America Corp. indicator, setting up the asset class for a short-term rally, according to strategist Michael Hartnett.

As investors face continued macroeconomic and market uncertainty, evolving the 60/40 portfolio of stocks and bonds to include alternative investments may help build portfolio resiliency.

The long history of business cycles illustrates that rising inflation precedes recessions. Inflation accelerations don’t just happen, they are caused.

The U.S. economy’s remarkable resilience is complicating the lives of investors and the Federal Reserve. Despite war-disrupted commodity markets and one of the most aggressive monetary tightening phases in modern history, economic activity has remained strong.