Five Reasons We Remain Optimistic on Equities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- Favorable seasonals should provide a tailwind

- The market may be misinterpreting mega earnings

- Contrarian catalyst as sentiment has turned bearish

Much like Halloween, it has been a scary time for investors – with the S&P 500 nearly entering correction territory (a decline of >10%), the NASDAQ down 12% from its recent highs, and the percentage of stocks below their 200-day moving average (~27%) at YTD lows. Equity pullbacks are never comfortable, but it is important to put them in perspective. The S&P 500 typically experiences three to four 5% declines a year – one of which is usually 10% or more – so the recent pullback is not unusual. Additionally, our directional views are based on where the equity market is relative to our fair-value target. When the equity market soared above our year-end target of 4,400 in July, we became more cautious. Fast forward to today, and the recent declines now provide S&P 500 upside of 6% and 12% into our year-end (4,400) and 12-month (4,650) targets, respectively. Below are five reasons we remain optimistic on equities.

- The Fed’s tightening cycle is coming to an end | While Fed Chair Jerome Powell has kept open the option to lift rates further if the data warrants, we believe the Fed’s historic tightening cycle is nearing an end (if not already over). Sure, the first estimate of real Q3 growth posted an impressive 4.9% gain, but this data is backward looking and not likely to be repeated – particularly with the sharp tightening in financial conditions over the last few months. More important, the core PCE indices showed further signs of inflation decelerating. This should give the Fed comfort to pause at their policy meeting next week. Given we expect growth to soften and the jobs market to cool further as we head into the final months of the year, the Fed’s job is likely done. If we’re correct, this should bode well for stocks as the S&P 500 typically gains 14% the 12 months after the Fed’s final rate hike.

- Lower interest rates should support stocks | The rise in 10-year Treasury yields to 5.0% has weighed on the equity market, with the S&P 500 down 9.8% from its July peak. This is not surprising given the inverse relationship between interest rates and price-earnings multiples. However, yields moving higher at the rapid pace we have seen appears inconsistent with slowing of the economy per the real-time economic indicators we follow. Yes, supply/demand dynamics have been driving interest rates lately, but the macro drivers of softer economic growth and continued disinflation should drive interest rates significantly lower over the coming months. And if this happens, it should support an improvement in the multiple, driving equity prices higher.

- The market may be misinterpreting mega earnings | The S&P 500 earnings recession (the past three quarters of earnings growth have been negative) is set to end with third quarter earnings growth expected to rise a paltry ~2% year-over-year. Admittedly, overall, it has been a fairly lackluster earnings season to date with the percentage of companies beating their revenue and earnings forecasts slightly below average, the magnitude of ‘beats’ trailing recent quarters and guidance highlighting increased uncertainty about the strength of the economy. But from our vantage point, there is an apparent disconnect between the actual results and the market performance of several of the mega cap tech names that reported this week. For example, despite posting blended EPS growth of 44% YoY and crushing estimates by ~13% in aggregate, a composite of MAGMAN** (the main driver of positive returns for the market year-to-date) declined 4% during the week and is now down 10% from recent highs. These price moves are inconsistent with fundamentals, and the positive results from these mega cap names (~18% EPS weight) combined with solid results from the financials (18% EPS weight) leave us confident in our 2024 S&P 500 earnings forecast of $220-225. Resilient earnings should allow for the equity market to move higher over the next 12 months.

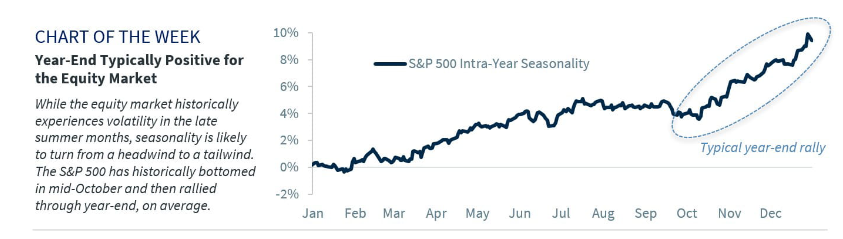

- Favorable seasonals should provide a tailwind | Recent equity market performance has followed the seasonal patterns seen over the last fifty years, declining in the months of August and September (historically the two weakest months of the year) with weakness extending into October. Fortunately for investors, the seasonal trend is set to turn to a tailwind as we enter two of the strongest months of the year with the S&P 500 up an average of 1.5% and 1.2% in November and December respectively.

- Contrarian catalyst as sentiment has turned bearish | With the S&P 500 off to its best start to a year through July since 1997, the summer months were filled with plenty of optimism as many Wall Street analysts raised their year-end forecasts. Investor sentiment also became very optimistic (i.e., bullish), with the percentage of bullish investors rising to the highest level since March 2021. This heightened optimism was one reason we highlighted in August that caused us to grow more cautious on the market. However, with the market nearing correction territory, this over-optimism has largely evaporated. In fact, bearish sentiment (measured by the AAII Investor survey) rose to a five month high this week, and technical indicators such as RSI reflect that the S&P 500 has declined into oversold territory (a level <30)—a level that has historically provided a reliable contrarian signal. As a result, cautious sentiment leaves us more optimistic that the market can move higher over the next 12 months.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All