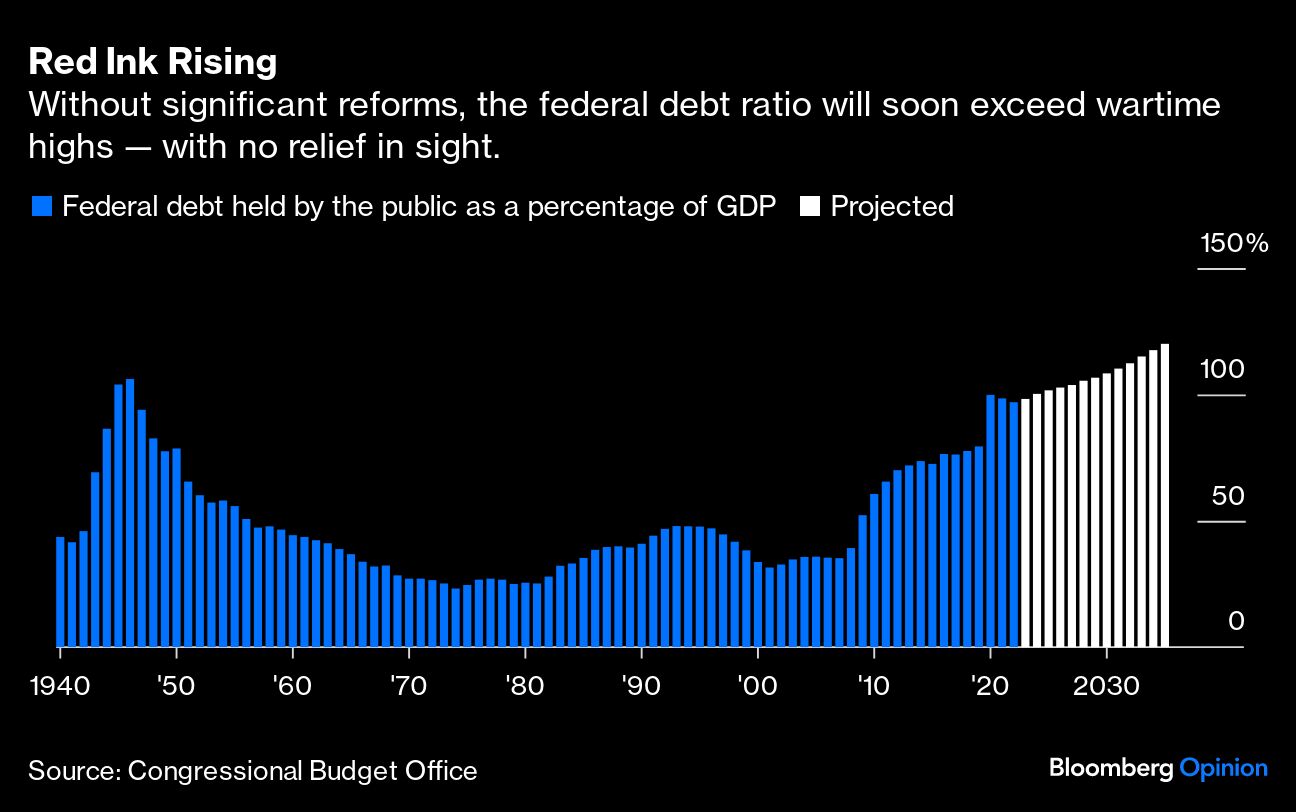

In the fiscal year that just ended, the US government borrowed $1.7 trillion, more than 6% of gross domestic product. Bear in mind, that was with an economy running hot, with high inflation, and more than full employment. On current policies, deficits are on track to grow further. Unless something is done, the ratio of net federal debt to GDP will soon surpass 106% — a level last reached at the end of World War II — and then keep on rising.

This outlook, largely ignored by Washington’s policymakers, points to a looming budget catastrophe. The question is whether the problem can be addressed before it’s too late.

In some ways, the new numbers understate the issue. Excluding timing shifts connected to President Joe Biden’s plan to cancel student loans (blocked by the Supreme Court this summer), the deficit was roughly $2 trillion, more than twice that of 2022. An economic slowdown, to say nothing of an outright recession, would push the forecast even higher. And standard projections assume that many of the tax reductions bundled into the 2017 Tax Cuts and Jobs Act will expire at the end of 2025, as that law provides. If Congress extends them (a decision that would win support on both sides of the aisle), deficits and the debt will grow even faster.

What’s going on? Pandemic-related spending subsided in 2023 — but the relentless pressure from growing entitlement spending (mainly Social Security and Medicare) pushed the other way. Adding to this is the newest driver of borrowing — higher long-term real interest rates.

Higher nominal rates raise the cost of servicing debt but don’t worsen the long-term debt position if they merely offset inflation, which causes both debt and nominal GDP to grow faster. Lately, the cost of borrowing has moved markedly higher in inflation-adjusted terms, adding to the gap between growth in debt and growth in output. What’s worse, the fiscal outlook may be one of the factors pushing bond yields up. A vicious circle is foreseeable — where concerns over mounting debt raise real interest rates, which worsen the future debt ratio, and so on.