Greater stability in US Treasuries is needed for the smooth functioning of other segments of the financial market, housing and the economy more broadly, both in America and beyond. Such stability is unlikely to be anchored anytime soon by either clarity about economic prospects or an abundance of volatility-repressing financial flows. What is needed is a policy anchor that, at this stage, must necessarily have a significant monetary policy component.

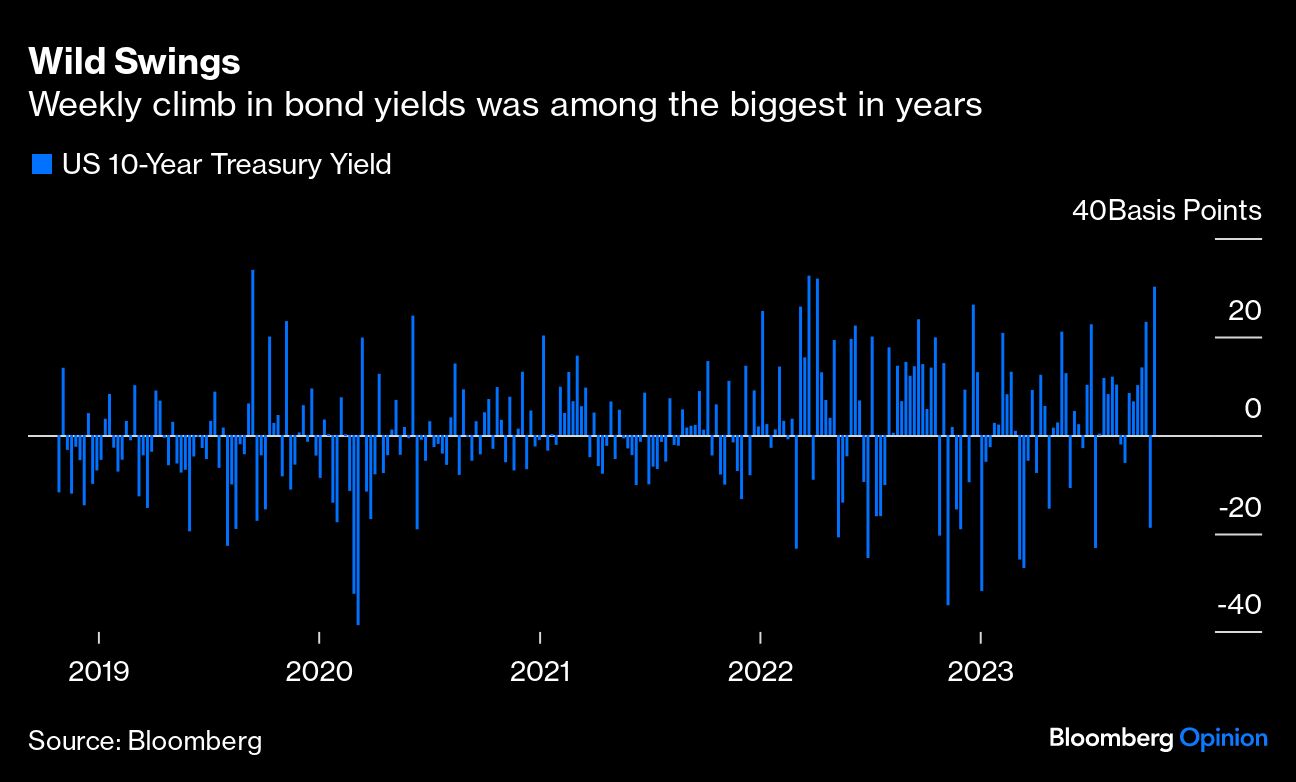

To say that the government bond market has been unusually unstable would be an understatement. Recent weeks have seen eye-popping intra-day moves in yields, uncertain auctions, and periodic concerns about liquidity and financial stability.

The Fed’s latest Financial Stability Report, released on Friday, addresses the issue of Treasury market liquidity, noting that it “is important because of the key role these securities play in the financial system.” The analysis documents how liquidity has been below historical norms and “may be less resilient than usual.”

Treasury yields serve as benchmarks for the pricing of a whole range of borrowing and lending by households, businesses and governments. They influence mortgage rates and the functioning of the housing market. They impact the stability of financial institutions and the system as a whole. And their moves spill over to other countries’ financial markets and economies, be they advanced or developing.

As I have detailed elsewhere, the recent bond volatility reflects both the loss of secular anchoring and the gradual weakening of short-term stabilizers. Specifically, the growth outlook is uncertain, and there are genuine questions about readily available buyers for Treasuries in the face of significantly higher supply occasioned by large budget deficits and mounting debt servicing. Together, they fuel periodic concerns about the health of regional banks and certain segments of the non-bank financial sector.

In such an environment, we would look to the Federal Reserve’s policy guidance to serve as an anchor.

Unfortunately, Fed communication has tended to impart volatility rather than stability in recent years. You need only look at last week’s event at the Economic Club of New York where, within less than an hour, comments by Fed Chair Jerome Powell drove the yield on the 10-year bond to fall below 4.90%, only to reverse course and surge up to 4.99% and subsequently change course yet again. This type of volatility during episodes of intense Fed communication has been shown by a Centre for Economic Policy Research study to be a substantial multiple of what has occurred under prior Fed chairs.

Fortunately for the bond market and beyond, the absence of longer-term stabilizers — economic, technical and policy-related — have been offset by short-term stabilizers. But, here too, things are far from reassuring.

Some investors have been willing to step in and buy on sudden surges in yields, looking to lock in for longer a stream of higher income. But this willingness is a function of the availability of funds and the ability to repeatedly overcome the fear of “catching a falling knife,” both of which erode the more often such surges occur.

On the other side, sudden dips in yields have enticed those sitting on large bond losses to reduce their excessive exposures at more attractive price levels. While it is far from clear how their risk appetite will evolve, the threat of large distress sales increases the higher yields go.

All this results in a configuration that calls for a stabilizing force in this crucial market. Unfortunately, it will not come from greater economic clarity given the competing winds buffeting the US economy. Nor will it come from assurances of large buyers for the increasing government bond issuance: The Fed is reducing its balance sheet, institutional buyers are nursing large losses, and foreign buyers appear hesitant.

What is needed is for the Fed to pivot from being volatility-inducing to being stability-enhancing. This will not happen unless, at the minimum, the world’s most powerful central bank does three things: Pivot its forward policy guidance from excessive dependence on backward-looking data to combining data dependency with a more clearly articulated economic vision; accelerate the revamping of an outdated Monetary Policy Framework to reflect the shift in the macro economy from a world of insufficient aggregate demand to one where supply is insufficiently flexible; and be more open-minded about the appropriate inflation target which, under current and expected conditions, may be closer to 3% than 2%.

The Fed will next have an opportunity to provide signals in these areas on Nov. 1 when it issues its policy statement and Chair Powell holds his regular press conference. Let us hope that this time around such communication helps reduce bond market volatility in a meaningful and durable manner. After all, this fundamentally speaks to both the Fed’s dual mandate and its responsibility to promote financial stability.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Real Estate Topics >