Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Yields are at some of their highest levels in over a decade. This means that if you own fixed income in your portfolio, there is a good chance that you are seeing unrealized losses on your monthly statements (fixed income math = yields higher, prices lower). Being comfortable with seeing losses on your individual bond holdings starts with answering one question: Why do you own fixed income?

For most investors, the fixed income allocation is intended to be the ballast of the portfolio. They purchase a bond for the stable and known attributes that are unique to fixed income: a known maturity date, a known maturity value, a known yield, and known cash flows over the life of the bond. These key characteristics are locked in from the date of purchase. A lot of things can change over the holding period of the bond, but as long as the investor holds the bond until the maturity date, any market activity (price and yield changes) are just background noise that has no effect on these key attributes*.

Yes, the price of your bond will change over the course of time, meaning that your monthly or quarterly statements will likely show gains and/or losses. The most important thing to keep in mind is that these gains or losses are unrealized. They are estimated gains or losses should you choose to sell the bond prior to maturity. The bond is going to be redeemed at par* making any price movement along the way irrelevant. The key benefits of the bond do not change because the price changed.

This is a concept that is unique to individual bonds and causes stress for many investors, so let’s draw a comparison that many will be more familiar with. Say you purchased a house a year ago for $500,000. Today, you visit a real estate website and see that the estimated value of your home has increased to $600,000. Does this change anything with the benefits that your home is providing for you? No. Your house didn’t gain an extra bedroom and shorten your commute by 15 minutes. It still has the same number of beds and baths, the same square footage, and is in the same neighborhood. It is still serving the same purpose that it served a year ago when you made the purchase: it is providing a roof over your family’s head. The same holds true if the estimated price of you home were to move in the opposite direction. If the estimated price of your home falls to $400,000, you don’t lose a bedroom and your home doesn’t move 15 minutes further away from work; it is still providing a roof over your family’s head.

This same idea holds true for the bond holdings in your portfolio. If you purchased a bond a year ago and when you open up your statement today, you see a loss of 5%, that doesn’t change a single thing about the benefit that the bond is providing you. It is still providing the same annual cash flow, the same yield, and will be redeemed on the same date and at the same price*. Just like in the house example above, if the price of your bond falls, none of the characteristics of the bond change. The same is true if the price of your bond rises and your statement shows that you have gains. Seeing gains on your statement might make you feel warm and fuzzy inside and seeing losses might make you feel morose, but for a buy and hold investor, neither of these scenarios changes anything about the benefit that the bond is providing for you and your portfolio.

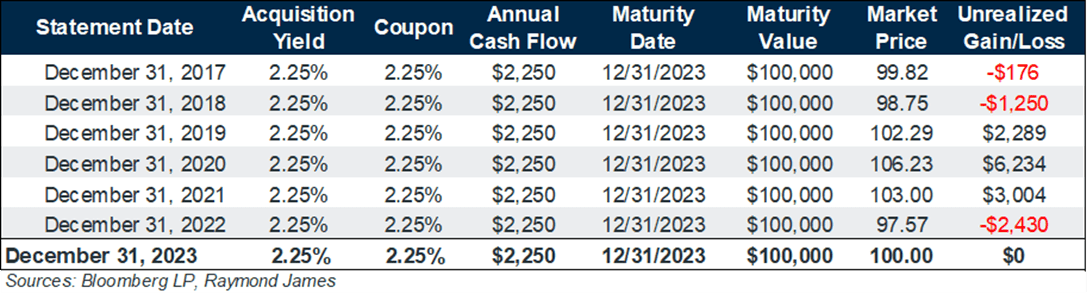

Let’s take a look at a real example. The chart below shows the data points that you would have seen on annual statements assuming you had bought $100,000 of the new issue 7-year Treasury in January of 2017 at par (100) that matures on 12/31/2023 with a coupon of 2.25%.

Notice that the key characteristics of the bond do not change over the life of the bond. The annual cash flow, redemption value, and maturity date do not change. Yes, the price is going to move on a daily basis and your corresponding gain/loss will adjust, but assuming you are a buy and hold investor, all of this movement and fluctuating between gains and losses has no effect, because on December 31, 2023, the Treasury is going to mature at par and you will receive every coupon payment that you are owed between the date you purchased the bond and the date the bond matures. Just because you had a $6,234 gain when you opened your statement on December 31, 2020, doesn’t change the cash flow or maturity value of the bond, just like having a loss of $2,430 on December 31, 2022, doesn’t change anything either. This is the role that fixed income plays in a portfolio: known aspects that you can plan your portfolio and your life around.

*Barring a default or other extraordinary circumstances.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Raymond James

Read more commentaries by Raymond James