The US dollar (USD) has weakened over the last few months, fueling strong emerging-market (EM) stock and bond returns in 2025. Now, with more clarity around tariffs and the record-long US government shutdown resolved, will the greenback strengthen and flip the script on EM? We don’t think so.

In today’s complex financial landscape, taxable US institutions face unique challenges in balancing their investment objectives with tax efficiency. They simply cannot afford to overlook the impact of taxes on their portfolios.

Rob Tayloe discusses fixed income market conditions and offers insight for bond investors.

In the ten years prior to the onset of COVID, the consumer prices index rose at an average annual rate of 1.7%. Since the onset of COVID the overall CPI has risen at a 4.2% annual rate. Inflation peaked at about 9.0% back in 2022 but is still hovering between 2.5 and 3.0%, which is above the Federal Reserve’s official target of 2.0%.

State Street Investment Management (SSIM) has been the investment advisor for the Select Sector SPDR ETFs since 1998. It will now take over the distribution and marketing for these funds. The move brings 11 ETFs in-house under the SSIM umbrella to unify its product offerings and enhance the investor experience.

US Federal Reserve officials would rather “stick to their knitting” than confront the complex forces that are reshaping the economy. Unless the next Fed chair shakes the institution out of its complacency, continued policy-induced volatility and intensifying political attacks are all but guaranteed.

The recent Thanksgiving week provided a crucial snapshot of the changing economy, highlighted by a shift in holiday shopping to early online sales and a significant drop in the 10-year Treasury yield below 4%.

Yields on the bond market have incrementally adjusted to introduce a new variable: a fiscal premium. Yet, this is not a new form of risk; it represents a new form of information. Investors still believe they will get repaid; they just believe they are entitled to a higher return to facilitate it.

No matter how long you delay taking Social Security, it likely won’t cover all your living expenses. But that doesn't mean you should take it early.

History shows that the starting points of technological revolutions are not invariably followed by large stock market selloffs. The historical precedent we draw from Carlota Perez's 2002 book, "Technological Revolutions and Financial Capital," coupled with the macrohistory.net data, provides some guidance.

The Benetton family’s holding company Edizione is setting up an alternative investment firm with about €3 billion ($3.5 billion) in assets under management as it seeks to grow its private markets.

Goldman Sachs Group Inc. will pay $2 billion to buy Innovator Capital Management, a deal that combines the bank with an issuer of a relatively new type of exchange-traded fund that has caught the attention and ire of some on Wall Street.

In today’s markets, mentioning the “B-word” will get you thrown into the “permabear” camp, and everyone immediately assumes you mean the end of the world: death, disaster, and destruction. Yes, bear markets have terrible short-term impacts, but they also allow the system to reset for healthier growth in the future.

My friend David Bahnsen wrote a brilliant analysis in his weekly Dividend Café of the private credit market a few weeks ago and it really took off. I got his permission to share it with you today. This is a basic primer on the risks in the private market and something as an investor you should be familiar with.

While outright defaults in the private credit sector remain low, analysts are increasingly concerned about the deteriorating outlook for repayment problems. When factoring in "selective defaults"—like borrowers adding interest to the loan (PIK loans) or extending maturities—the true default rate climbs to a significantly higher 4.6%.

When new homes start selling at a discount to re-sale houses, it’s time to sit up and pay attention. Apollo Global Management’s Chief Economist Torsten Slok noted the anomaly in a recent note , the first time it’s happened in more than five decades.

In the ranks of the world’s 20 best-performing stock markets this year, every second index is European.

Whether in sports or financial markets, averages often grab headlines, but they can conceal as much as they reveal. Variation—including the dispersion of metrics like credit spreads for high-yield bonds—is the real story.

This has been a bumpy year for the US economy. Although there was a massive boom in AI-related investments in 2025, policy-induced uncertainties and disruptions to official data releases clouded the picture.

U.S. stocks, as measured by the S&P 500 Index, are on pace for 14% growth in earnings for Q3 2025. This marks the fourth consecutive quarter of double-digit growth and comes in well ahead of analysts’ Sept. 30 estimates of 7%.

Despite the increasing need for retirement income security, many defined contribution (DC) plan sponsors hesitate to adopt new lifetime income solutions due to concerns over fiduciary liability and plan flexibility.

Following a rocky start to the year, the municipal bond market has shown strong performance in Q3 2025, outperforming broader bond indexes due to factors like easing oversupply and growing demand.

This article argues that the Federal Reserve's decade of ultra-loose monetary policy following the 2008 crisis, including nearly ten years of near-zero rates, has warped the perception of a "normal" interest rate environment.

Despite an intra-year drawdown of 18.9%, the S&P 500 is poised for a strong 2025, currently up about 14%. This pattern of experiencing a large correction on the way to significant annual gains is common; since 1980, the average yearly drawdown has been over 14% while the index gained an average of 10.7%.

Nvidia's strong earnings initially squashed AI bubble fears but a deep dive into its financials, revealing high customer concentration, triggered a major tech sell-off.

As investors start to take sides in the AI race, Sam Altman’s buddies are getting burned.

The Federal Reserve's balance sheet has significantly shrunk from its peak of nearly $9 trillion in 2022, shifting the reserve environment from "abundant" to "ample." While some advocate for further reduction, arguing it would increase market volatility and allow for lower rates, this move would necessitate a major operational change in how the Fed conducts monetary policy and would not dramatically lower short-term rates.

Kostas Bintas, the high-profile head of metals at Mercuria Energy Group Ltd., has renewed his bullish prediction for copper prices as he warned that a rush to ship metal to the US risks draining the rest of the world’s inventories.

The article argues that the oil market is mistaken to predict long-term prices will remain near the current $60-per-barrel level through 2030, believing oil will be more expensive due to tightening supply/demand balance.

This article questions if the high valuation multiples are justified, arguing that investors will soon need to see actual cash flow results from this massive CapEx bonanza.This aggressive spending has caused their collective free cash flow growth to turn negative, raising concerns since stock valuation is based on future free cash flow.

Despite the "America First" focus of the current administration, international markets, particularly emerging markets (EM), have outperformed domestic financial markets. This surprising trend is highlighted by the strong performance of EM debt and equities, driven primarily by U.S. dollar weakness and corresponding monetary easing by EM central banks.

This month, the global investment community is celebrating the 25th anniversary of the world’s first fixed income ETFs, the iShares Core Canadian Short Term Bond Index ETF (XSB) and the iShares Core Canadian Universe Bond Index ETF (XBB).

The Chicago Mercantile Exchange (CME), a crucial hub for managing global risk, experienced a nine-hour trading halt due to a data center fault on Friday, disrupting markets from S&P 500 futures to crude oil. This major outage underscores the CME's integral role in global market machinery, where its platforms handle volumes exceeding 26 million derivatives contracts daily.

Nasdaq’s International Securities Exchange proposed quadrupling the daily trading limit for options tied to BlackRock Inc.’s iShares Bitcoin Trust ETF as demand from investors increases.

This article argues that the pursuit of high returns by institutional investors, like insurers and pension funds, through illiquid and opaque private market investments is a repeating mistake that risks underfunding future liabilities.

The dominance of Jensen Huang and Nvidia in the AI hardware market is facing a significant challenge, signaling a shift in the industry's power dynamic. This is driven by news of Google potentially selling billions of dollars in its own Tensor Processing Units (TPUs) to Meta, following a similar major deal with Anthropic.

With corporate bond spreads widening and Oracle Corp.’s credit default swap spiking to a multi-year high, Wall Street is getting worried that a flood of debt sales from Big Tech is overwhelming buyers and could blow up credit markets.

Financial planning helps families organize, save, and invest intentionally. It turns goals into a roadmap, budgeting for major purchases, setting aside for retirement, and aligning investments with life milestones. But at some point, the question shifts from how to grow wealth to how to protect and structure it.

This year has certainly been a significant one for me. For the markets and the economy, it has been a big year as well. Rate cuts and no recession have been positive for stocks and bonds.

As wealth continues to grow along with soaring equity markets, and technology enables customization and choices once reserved for a select few investors, financial advisors are tasked with constantly evolving to maintain their value position.

Interest rates are undergoing one of the steepest reversals in half a century. In 2020, governments could borrow for 30 years at just over 1%. Fast forward to 2025 and U.S. 30-year yields have risen above 5% for the first time since 2007.

According to market theory, persistent outperformance shouldn’t exist. However, companies with high and stable profitability, strong balance sheets, and disciplined capital allocation have demonstrated the ability to deliver superior returns with lower risk over time.

Multi-strategy hedge funds have been around for more than three decades. Will they make it to a half century? Ray Dalio, founder of 50-year-old hedge fund Bridgewater Associates has his doubts about this thriving subsector of asset management.

The trade dispute with the U.S. is proving to be a 'full-blown blizzard' for Canada, threatening to freeze cross-border commerce in a deeply integrated relationship. Despite the majority of goods remaining duty-free, new tariffs—reaching 35% in key sectors—have caused a sharp decline in Canadian exports, pushing the nation toward recession.

At Vanguard, we are always working to make our target-date funds (TDFs) better. That means regularly reviewing our glide-path design and diving into specific asset allocation topics to ensure that our strategies evolve with the market and continue to meet our clients' needs.

Corporate America delivered another exceptional earnings season, with third-quarter S&P 500 earnings growth tracking over 13% and achieving one of the highest beat rates ever recorded. Companies successfully adjusted to shifting macroeconomic pressures, including tariffs, as expectations continued to rise. The impressive results were bolstered by robust revenue growth and significant investment from mega-cap technology firms.

Although most economists have issued dire warnings about the damage tariffs and other ill-advised policies would cause, the US economy’s aggregate indicators have remained quite robust. Some of the costs may simply have been postponed, but rapid advances in AI could well offset them when they fall due.

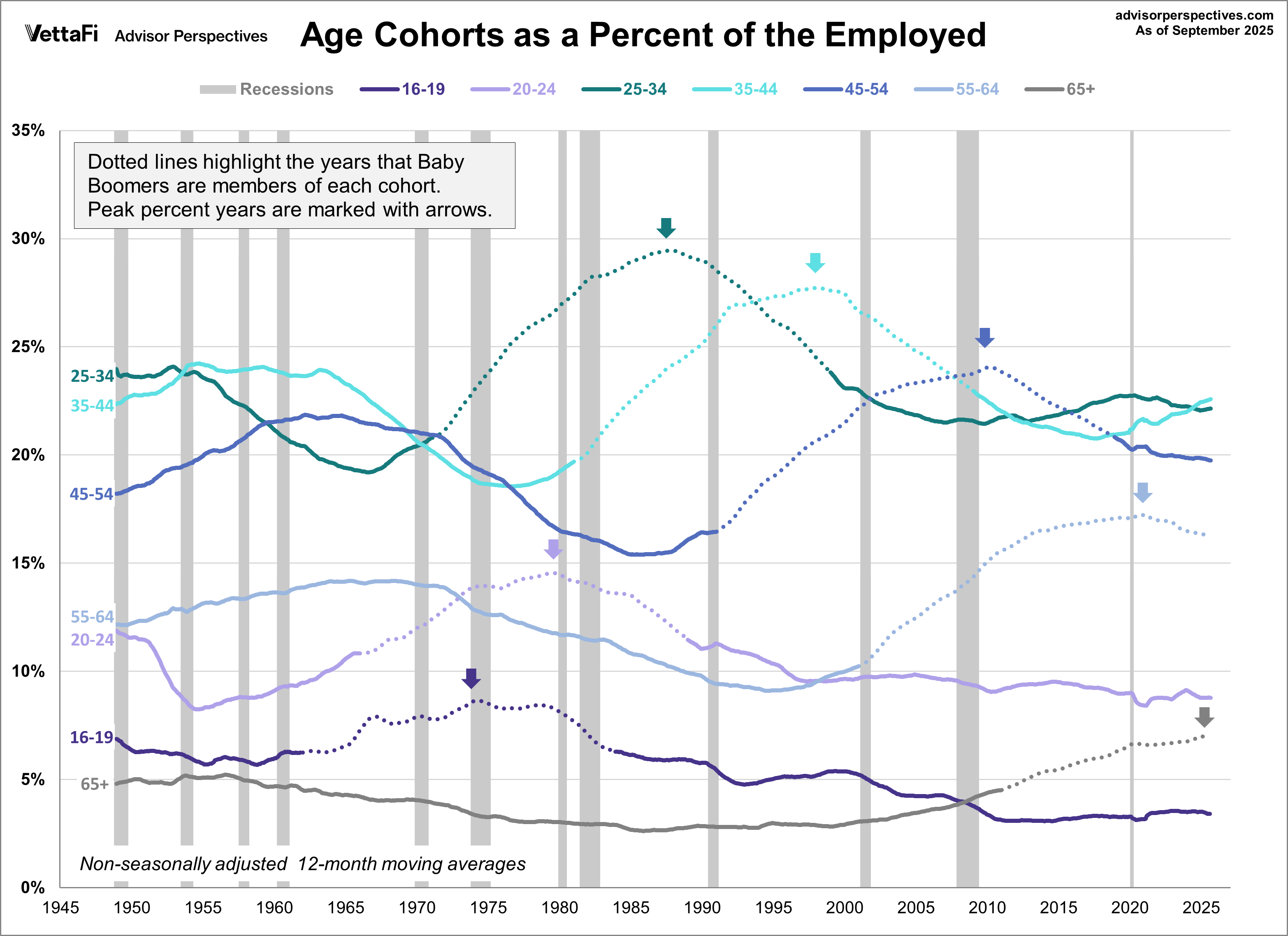

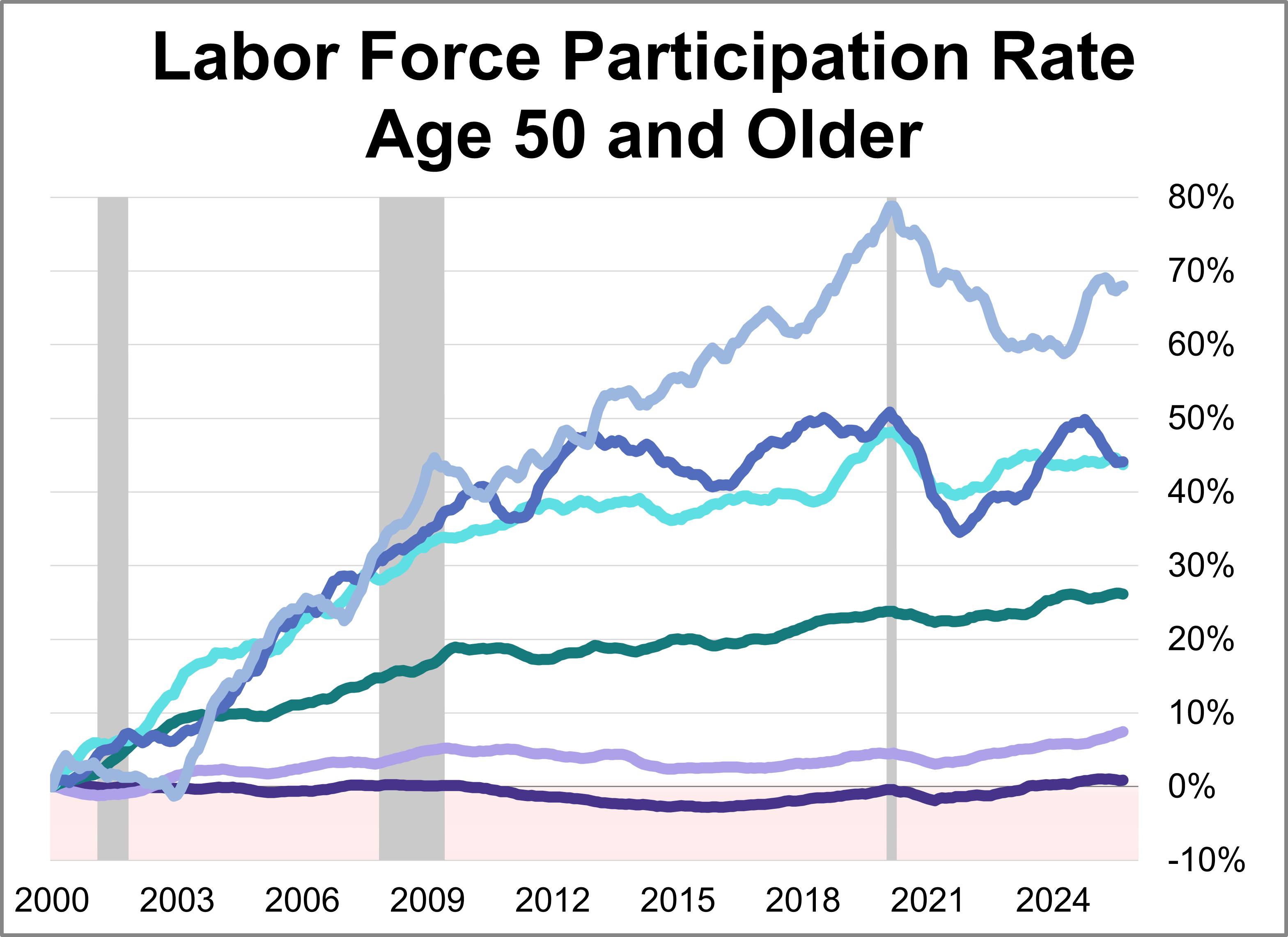

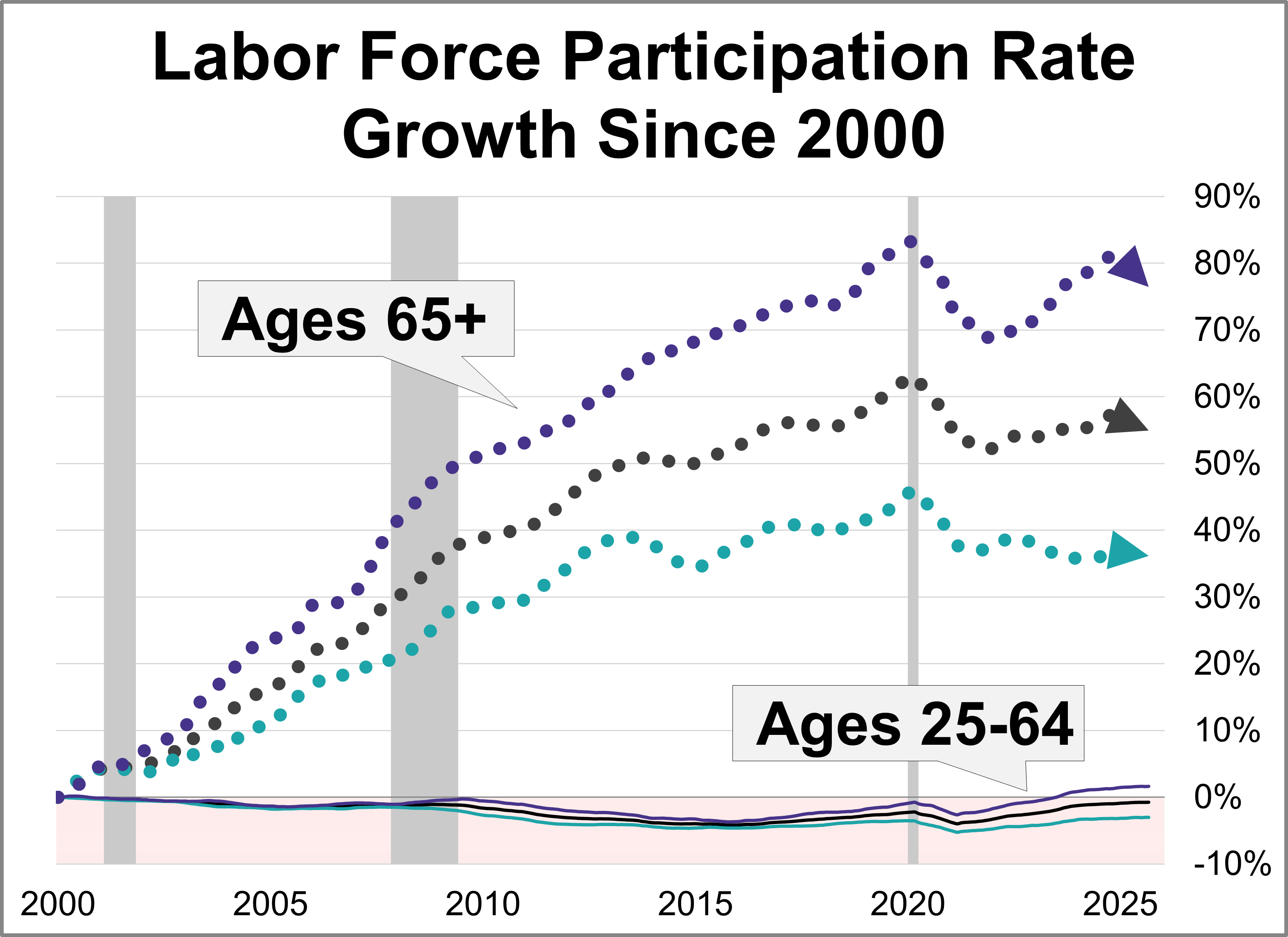

The 20th century Baby Boom was one of the most powerful demographic events in the history of the United States. We've created a series of charts to show seven age cohorts of the employed population from 1948 to the present.

Today, one in three of the 65-69 cohort, one in five of the 70-74 cohort, and one in ten of the 75+ cohort are in the labor force.

The labor force participation rate (LFPR) is a simple computation: You take the civilian labor force (people aged 16 and over employed or seeking employment) and divide it by the civilian non-institutional population (those 16 and over not in the military and or committed to an institution). As of September, the labor force participation rate is at 62.4%, up from 62.3% the previous month.