From investing to economics to politics, patterns emerge, lessons resurface and the past becomes a powerful guide for navigating today’s unpredictable landscape. Timing, perspective and adaptability can make all the difference in managing the complexities of modern markets.

As the global economy navigates a complex landscape, investors are left wondering: are they right to be optimistic or are they being complacent? This article from Franklin Templeton Institute explores the signs of resilience as well as numerous risks.

Though some urge rate cuts, doing that won't necessarily reduce borrowing costs if the market doesn't agree with the timing. It could raise inflation fears, hurting Treasuries.

Sharp U.S. policy shift and elevated uncertainty reflect an evolution of the new macro regime. What matters: getting a grip on uncertainty by identifying its core features.

Some say private credit hasn’t been tested. We disagree…and stress can sharpen the senses.

Treasuries tumbled after a stronger-than-expected jobs report for June prompted traders to exit bets on an interest-rate cut by the Federal Reserve this month.

Proposed regulatory changes involving the Supplementary Leverage Ratio may have benefits for both large banks and the Treasury market.

Equity markets continued to march higher in June, seemingly unfazed by heightened Middle East tensions (which were short-lived) and the looming July 8 deadline for the administration’s pause on reciprocal tariffs.

We began the year optimistic that an environment of slowing growth, disinflation and easier monetary policy would be favorable for fixed income markets. Now at midyear, we maintain that view, while acknowledging that policy uncertainty and geopolitical risks may likely result in continued volatility.

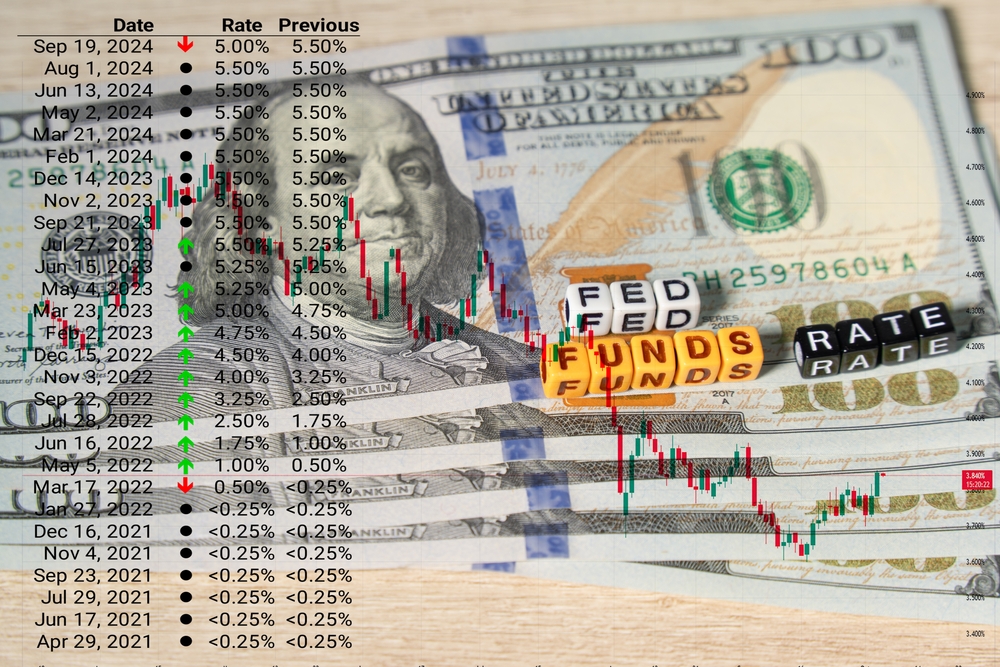

It has been over six months since the FOMC has made a change to the Fed Funds rate. While the debate continues as to when the next cut will be, market consensus (per Bloomberg calculations) is currently for a 25 basis point cut in September.

An economy cannot subsist on services alone.

On the latest edition of Market Week in Review, Global Chief Investment Strategist Paul Eitelman explored key drivers behind the strong performance in markets. He also provided an update on a proposed U.S. tax measure.

The US economy is important, but it’s not the only one in a global approach.

In recent months, markets have whipsawed amid changes in trade policy, geopolitical shocks, concerns about fiscal sustainability, challenges to central bank independence, technological advancements, and earnings surprises in both directions. Despite this, stocks and bonds in much of the world are close to where they began the year.

For good reasons, many investors have a love-hate relationship with commodity investments. Operationally, the annoying K-1 form complicates tax filing, although thankfully the industry has started to launch “no K-1” funds.

Treasuries are set for a second daily drop heading into a double whammy of labor data, following an unexpected jump in US job opening numbers.

The marathon Senate budget vote took center stage early and stocks slipped from yesterday's all-time highs. Job openings, Powell, and manufacturing data are top of mind.

Markets notched fresh all-time highs on Friday with a positive tone and geopolitical outlook. Swift retreat in oil back to pre-strike levels, combined with friendlier NATO negotiations and de-escalated fighting in Iran restored risk appetite.

For sophisticated investors, this technical shift marks a subtle but powerful pivot in monetary mechanics. It could create demand for Treasuries, improve market liquidity, and push yields lower at a time when the economy is slowing.

With the market roughly at the midpoint for 2025, investors and advisors are still assessing how changing macroeconomic conditions could affect their fixed income portfolio.

Easing trade tensions and hopes the Senate could pass a budget gave stocks an early lift after Friday's record highs. The week is packed with jobs news and Powell talks tomorrow.

Victory Capital’s Lance Humphrey walks through the VictoryShares ETF lineup and shares his perspective on the current market environment. VettaFi’s Kirsten Chang highlights key takeaways from the firm’s Mid-Year Market Outlook Symposium, offering insight into how advisors are approaching portfolio allocations for the remainder of the year.

The United States’ tariff announcement on April 2, 2025, created significant market volatility, as the tariffs were perceived as higher, broader, and more punitive than expected, and the implementation sooner.

Stocks are wrapping up a stellar quarter at all-time highs amid signs of progress in US trade talks while hopes the Federal Reserve will resume its rate cuts drove Treasuries toward their biggest first-half stretch in five years. The dollar eyed its longest monthly slide since 2017.

Treasury Secretary Scott Bessent indicated it wouldn’t make sense for the government to ramp up sales of longer-term securities given where yields are today, though he held out hope that interest rates across maturities will be falling as inflation slows.

The S&P 500 Index just rallied back to all-time highs, brushing off the April tariff shock, the conflict with Iran and the insidious and persistent increase in US continuing jobless claims.

We continue to suggest an "up in quality" fixed income bias for the short run, but investors can still consider some of the riskier parts of the fixed income market in moderation.

Until recently, commercial real estate appeared poised for a long-awaited rebound. However, 2025 has revealed a new reality: Uncertainty has become structural.

Last week's economic data presented a mixed picture, emerging against the backdrop of a record market rally and rising inflation.

Index futures inched upward premarket as the headline May PCE data landed in line with expectations, though the core data and annual figures were up slightly.

Today’s investment landscape, shaped by persistently above-target inflation, structurally higher debt and deficits, and reduced global dollar recycling into US financial markets, has contributed to elevated market volatility alongside historically high policy uncertainty.

The Fed left rates unchanged and signaled it’s still in wait-and-see mode, even as inflation risks and policy uncertainty persist.

Former Federal Reserve Vice Chair Richard Clarida explains where yields may be headed, as well as positioning considerations for the long-run by charting the relationship between r* and term premium.

Jeff Chang, CFA, President of Vest, a pioneer of Target Outcome Investments with some $50 billion under management, examines how geopolitical events like U.S. airstrikes can create ripple effects across global markets, and why the actual impact often depends more on context than headlines suggest.

The dollar fell and US Treasuries rallied after a report that President Donald Trump is considering naming Federal Reserve Chair Jerome Powell’s successor well before the incumbent’s term is scheduled to end next May.

It's not often that UK stocks are singled out as a "favorite geopolitical hedge," as Citigroup Inc. strategists boldly stated last week. So perhaps the elegant stance would be to simply take the rare praise when it's so kindly offered.

Tensions in the Middle East and their effect on oil prices have dominated the recent news headlines—and for good reason. A rise in oil prices, especially if it lasts, can push up inflation and slow down economic growth.

The Federal Funds Rate (FFR) is the interest rate banks charge each other to borrow money overnight. It's set by the FOMC and is one of the Federal Reserve's primary tools to implement monetary policy and is a key driver of economic activity. This video examines the Federal Funds Rate and reviews the Fed's latest interest rate meeting.

Just when the International Monetary Fund sees slower growth around the globe, the economy the World Bank ranks 112 out of 196 based on gross domestic product is leading everyone – with the opposite outlook.

Froth in the red-hot private credit marketplace is creating opportunities in the world of public high-yield debt, according to George Gatch, JPMorgan Asset Management’s chief executive officer.

How do direct indexing ideas fit into a fixed income portfolio? These two powerful strategies make one compelling combination with potential tax and risk management opportunities.

Foreign demand for U.S. Treasuries remains intact.

The recent decline in the dollar relative to other currencies is well within historical norms. Notably, previous declines were much larger without the “fear-mongering” from the “experts of doom.”

CEFs stand out due to their fixed capital structure, allowing portfolio managers to focus on long-term investment strategies without the need to manage daily inflows and outflows.

Portfolio Managers John Kerschner and John Lloyd and Client Portfolio Manager Steve Preikschat investigate the case for multisector bond funds as a core fixed income allocation.

When investors approach the financial markets, there’s a tendency to imagine that conditions can be judged as favorable or unfavorable based on one single measure or another. The fact is that market conditions at any moment in time are a composite of interdependent forces.

The yield curve for U.S. government bonds is currently very unusual — it’s U-shaped. In addition to the changes in shape, also note the level of interest rates.

While the bond market is in general pretty efficient in its pricing, there may be times when it can be significantly out of line with investor expectations. At such moments, investors should be well-rewarded for making the effort to decode what the bond market is saying.

It may seem as if Treasuries are the better bet these days with the US stock market back near record highs and government securities offering respectable yields again. But stocks are still likely to pay more.

The rush of cash into the US money-market funds is showing few signs of slowing as it secured a record $7.4 trillion in assets.