Equity markets continued to march higher in June, seemingly unfazed by heightened Middle East tensions (which were short-lived) and the looming July 8 deadline for the administration’s pause on reciprocal tariffs. Despite an interim bout of volatility, it was a record-breaking month for the S&P 500 and the tech-heavy NASDAQ as both indices ended the month with new all-time highs. The Dow Jones Industrial Average was up 4% for June.

Nine out of the 11 sectors delivered positive returns, with Consumer Staples and Real Estate lagging.

Signs of an economic slowdown continued to mount, fueled by weak housing data, further cooling in the labor market and an unexpected deceleration in consumer spending. Lower oil prices have put downward pressure on inflation in recent months; however, the impact from tariffs is still expected to affect prices in the months ahead. The risk of higher inflation has kept the Federal Reserve (Fed) in wait-and-see mode, with policymakers holding the benchmark interest rate steady at 4.25%-4.5% in June, as expected.

While this month’s decision was easy, future policy actions are likely to become more challenging as the Fed will need to balance the risks of softening growth and a murkier outlook for inflation. The market still has two rate cuts priced in by year-end 2025.

Bond yields edged lower in June, with the 10-year Treasury falling to a two-month low of 4.25% as signs of economic weakness began to emerge. Adding to the positive sentiment in the bond market were comments from several Fed officials, which pushed forward the expectations for a Fed rate cut to September, one month earlier than expected.

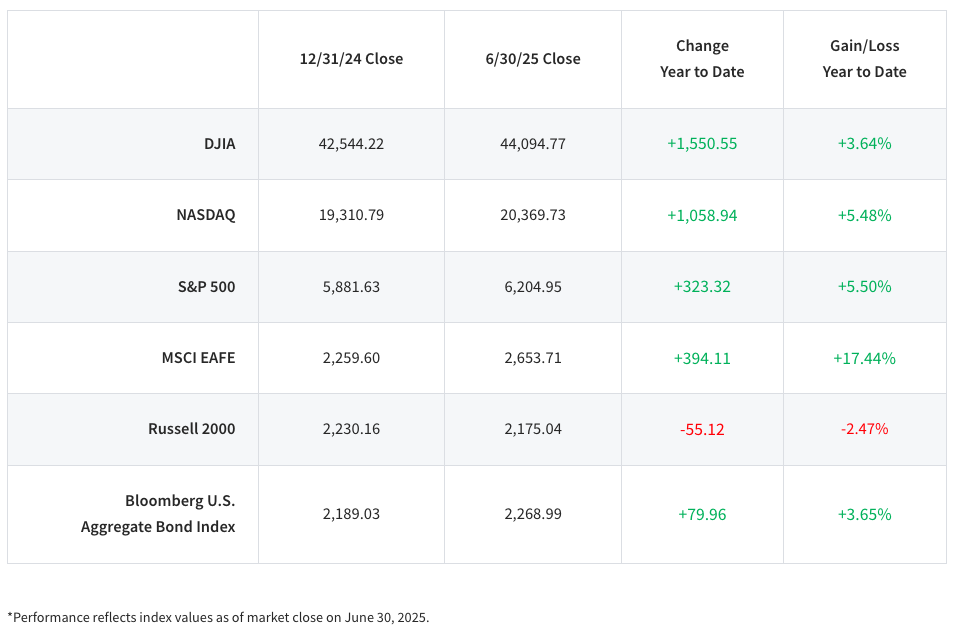

We’ll dive into the details below, but first, a look at the numbers year-to-date:

Equities grind higher

Equity markets have been in a slow grind over recent weeks, drifting slightly higher toward February’s all-time highs. Consensus GDP estimates have stabilized around 1.4% for 2025 and have moved toward 1.6% for 2026. Corporate earnings expectations are moderate, despite tariffs.

Oil prices spike temporarily

Amid nonstop news on Iran, oil prices briefly approached 52-week highs in June after hitting a four-year low in May. With a ceasefire in place, oil prices have receded.

Meanwhile, China has agreed to maintain a steady supply of rare earth exports to the US, reversing its earlier restrictions – but its commitment is limited to six months. The US already mines more than enough rare earths for its domestic needs, but doesn’t yet have sufficient processing capabilities, which leaves them as a bargaining chip for China.

US economy weakening but shows resilience

The large rebound in the stock market in May wasn’t enough for the Leading Economic Index to show a positive print last month. The Conference Board indicated it expects further weakening in economic activity for 2025 and 2026 under the pressure of tariffs, but is not expecting a recession this year.

The trade deficit in goods and services declined to levels not seen since 2023 as the front-loading of imports during the first quarter of the year gave way to more normal levels. The recent weakness in the US dollar is also benefiting goods exports, which increased last month. Import prices were higher than expected in May, but the year-over-year rate continued to fall, which is good news for inflation going forward.

The market for new homes is deteriorating faster than expected, but lower new housing inventories should keep home prices stronger than they would be otherwise. Existing home sales were better than expected in May, but prices showed signs of plateauing.

Job numbers were stronger than expected in April and the Employment Index improved in May. Despite a net downward revision of 95,000 jobs during the previous two months, job growth remains healthy.

Washington remains focused on tax cuts

The reconciliation bill was a key issue in June, with the Senate proposal permanently extending the 2017 Tax Cuts and Jobs Act, enhancing the Child Tax Credit and introducing provisions of no tax on tips and overtime. While the July 4 deadline for passing the provisions isn’t impossible, it is ambitious. Bill passage may be pushed closer to the debt limit “X date,” which is expected to fall between mid-August and early October.

Economic strain in the UK

As the July deadline nears, the UK and US are close to finalizing a largely symbolic trade deal which the UK is motivated to secure in light of its weakening economy. Chancellor of the Exchequer Rachel Reeves recently delivered a very tight Spending Review, sticking to previous budget plans but cutting most departmental budgets except for defense, healthcare and education. With little room left in the budget, tax hikes could be forthcoming this fall if productivity doesn’t improve. Meanwhile, the Bank of England held interest rates steady at 4.25% in June, signaling a possible rate cut in August to support the economy.

The bottom line

It’s safe to expect some give-and-take on tariffs and for the resulting negative headlines to spur volatility in the near future.

“Historically, when there’s a geopolitical event, the market reacts quickly and then tends to look through the ‘noise,’” said Raymond James Chief Investment Officer Larry Adam. “Ultimately, it’s the fundamentals that matter.”

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Raymond James Chief Investment Officer and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. Diversification does not guarantee a profit nor protect against loss. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australasia and Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small-cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges, which would reduce an investor’s returns. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification. A credit rating of a security is not a recommendation to buy, sell or hold the security and may be subject to review, revision, suspension, reduction or withdrawal at any time by the assigning Rating Agency. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Income from municipal bonds is not subject to federal income taxation; however, it may be subject to state and local taxes and, for certain investors, to the alternative minimum tax. Income from taxable municipal bonds is subject to federal income taxation, and it may be subject to state and local taxes. Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. Investing in small-cap stocks generally involves greater risks, and therefore, may not be appropriate for every investor. The prices of small company stocks may be subject to more volatility than those of large company stocks.

Material created by Raymond James for use by its advisors.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

J.D. Power 2025 U.S. Investor Satisfaction Study, which measures overall investor satisfaction with investment firms, was released 3/20/25, based on investors surveyed 1/24-12/24, who may be working with a financial advisor. Based on 7,876 responses from Advised Investors, 1 company out of 24 was chosen as the winner. The award is not representative of any one client’s experience, is not an endorsement, and is not indicative of an advisor’s future performance. The study is independently conducted, and the participating firms do not pay to participate. Use of study results in promotional materials is subject to a license fee. J.D. Power is not affiliated with Raymond James. For J.D. Power 2025 award information, visit jdpower.com/awards.

© 2025 Raymond James Financial, Inc. All rights reserved.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition - March 2025 (PDF)This website uses cookies to ensure you get the best experience on our website. By clicking ‘X’, you accept all cookies by default and exit the banner.

© Raymond James

Read more commentaries by Raymond James