Last week's economic data presented a mixed picture, emerging against the backdrop of a record market rally. Inflation surprisingly heated up in May, reports on consumer attitudes showed conflicting signals, and the economy’s first quarter contraction was deeper than expected. Meanwhile, the S&P 500 climbed throughout the week, flirting with a record high before finally achieving that new milestone on Friday.

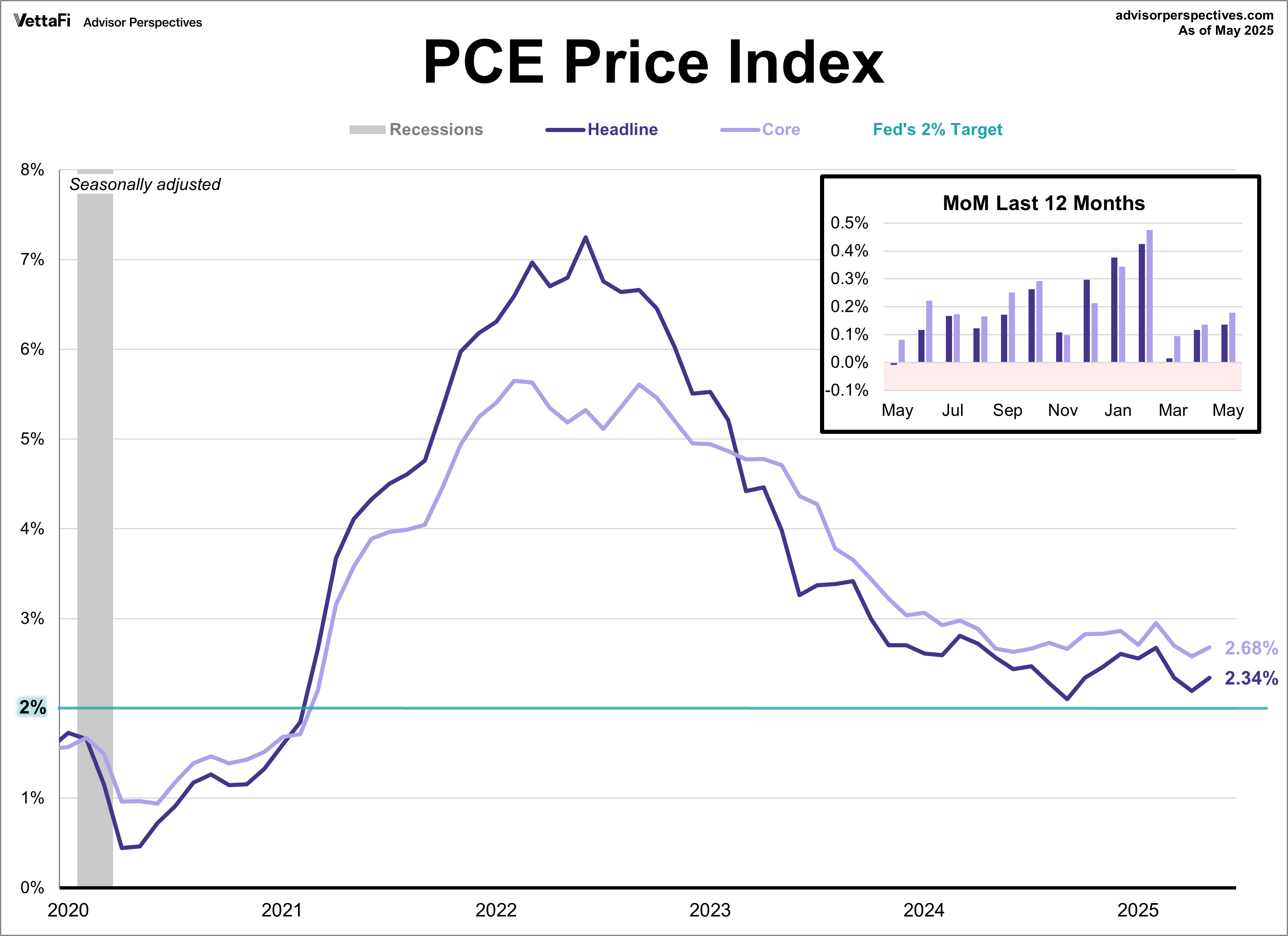

PCE Price Index

Inflation, as measured by the Federal Reserve's preferred metric, was higher than anticipated last month, inching further away from the Fed’s 2% target. The Core Personal Consumption Expenditures (PCE) Price Index, which excludes volatile food and energy costs, rose 2.7% year-over-year in May. The latest reading was higher than the expected 2.6% growth and marked a slight pick up from April’s 2.6% reading. On a monthly basis, core prices rose 0.2%. This was also higher than expected, surpassing the projecting 0.1% monthly growth. Meanwhile, the headline PCE Price Index saw a 2.3% annual increase. This was consistent with the forecast, but was up from April’s 2.2% growth. Monthly. The headline index also rose by 0.1%, as expected. Despite the latest report showing price increases accelerating, Fed Chair Jerome Powell testified to Congress earlier in the week that the central bank will remain in “wait-and-see” mode until they have more clarity on tariffs’ impact on inflation and the economy’s trajectory.

Consumer Attitudes

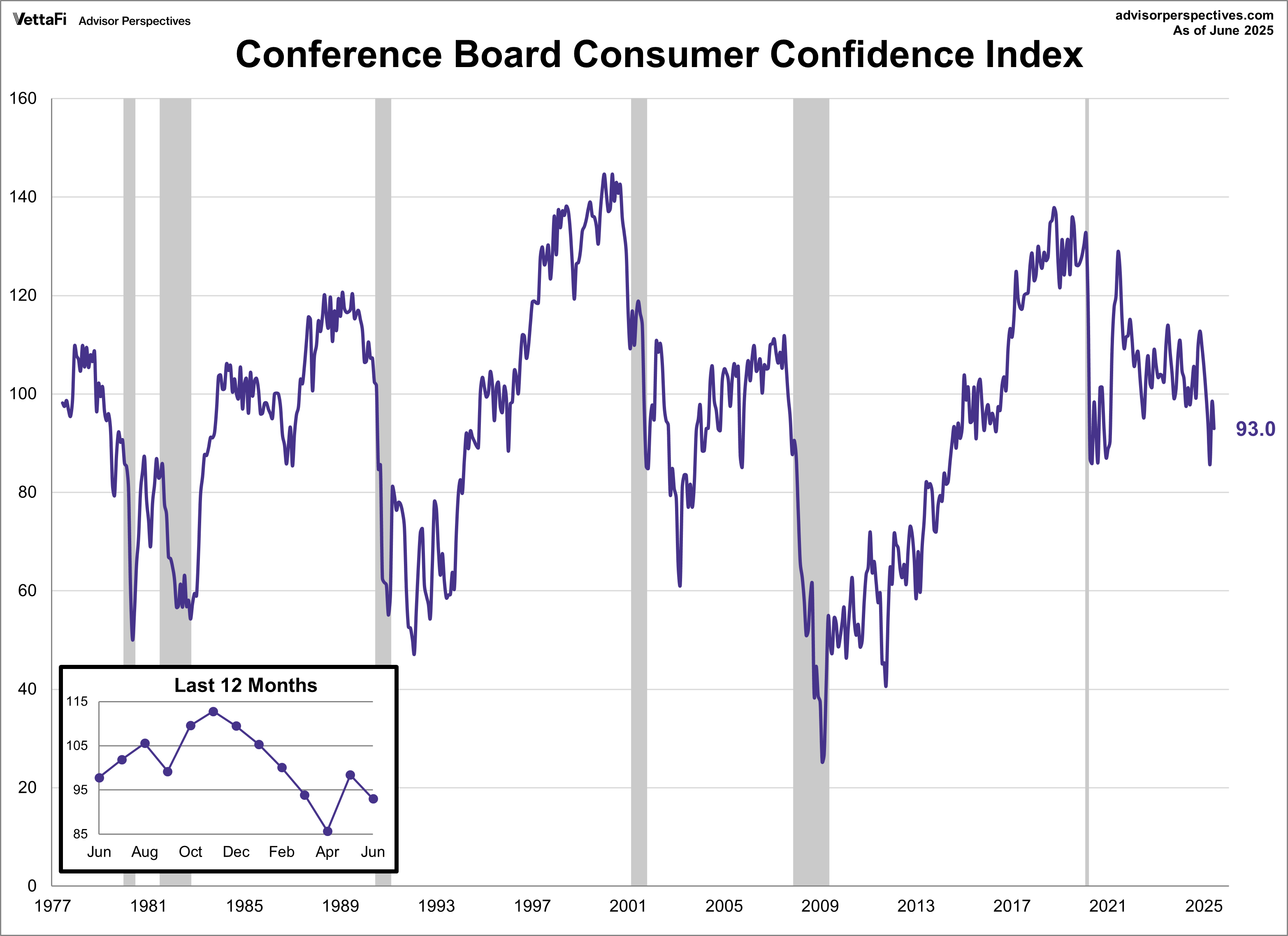

Conference Board Consumer Confidence Index

Consumer confidence unexpectedly retreated in June, with the Conference Board Consumer Confidence Index® falling 5.4 points to 93.0. This decline pared back nearly half of May's gains and marks the sixth monthly decrease in consumer confidence in the past seven months. The latest reading was worse than the expected forecast of 99.4 and puts the index at its second lowest reading in over four years, surpassing only April's 85.7.

The drop in consumer confidence this month was widespread, as all five components tracking attitudes toward current and future economic conditions worsened. While perceptions of the current labor market softened for the sixth consecutive month, they held positive, suggesting the labor market remains solid. Additionally, the Expectations Index fell even further below the threshold that typically signals an impending recession.

Other notable takeaways from June’s survey revealed that tariffs and inflation are still primary concerns for consumers. However, there were some mentions of easing inflation, which led to 12-month inflation expectations cooling further to 6.0% (down from 6.4% in May and 7.0% in April). And lastly, despite ongoing geopolitical tensions, consumer references to the topic remained low on the list of factors affecting their views.

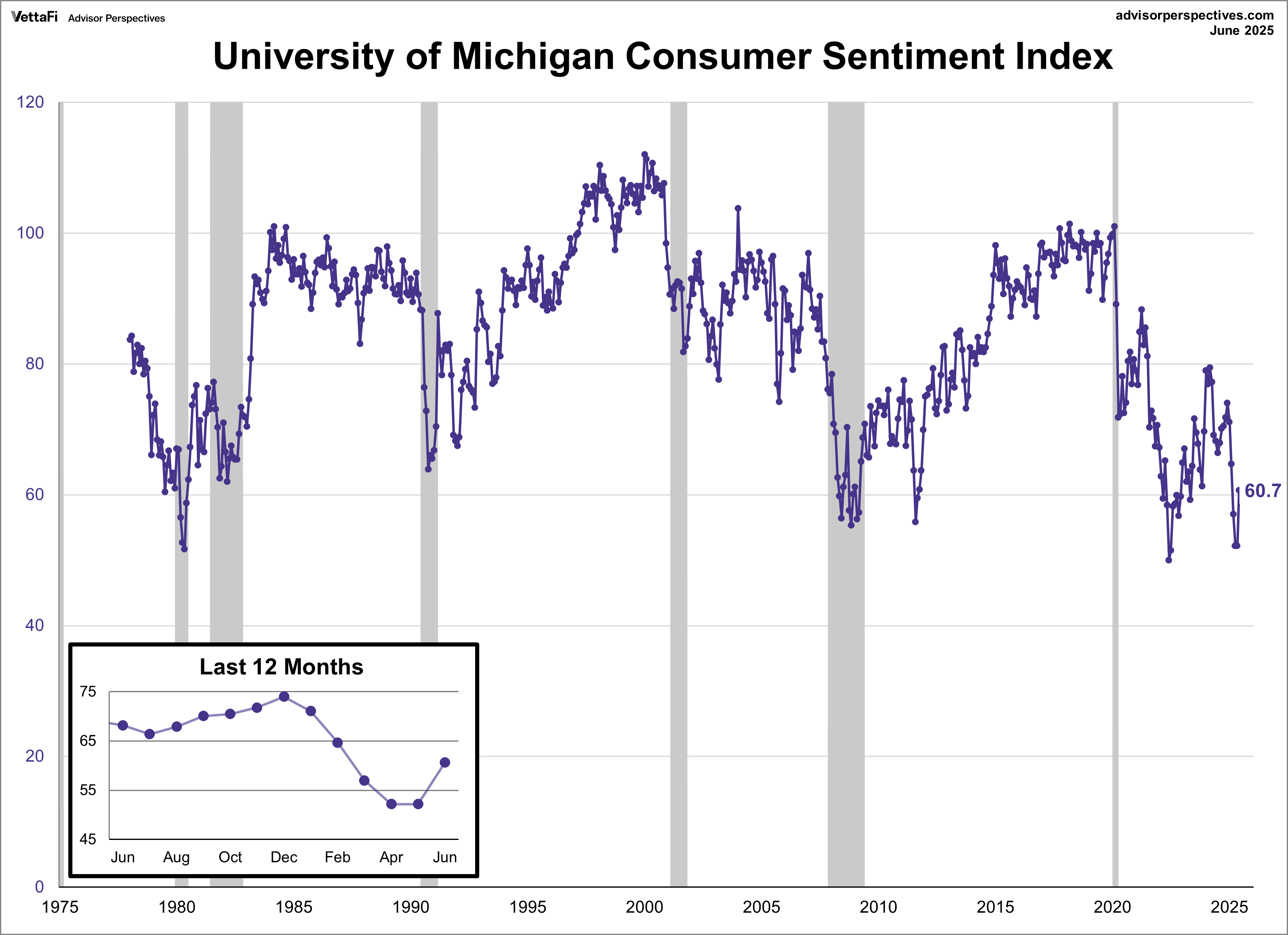

University of Michigan Consumer Sentiment Index

Consumer sentiment rebounded in June, improving for the first time in six months. The Michigan Consumer Sentiment Index increased 8.5 points to 60.7 this month, its highest level since February but still reflecting historically low levels of optimism. This represents a 16.3% increase from May’s final reading. The largest monthly increase in over thirty years still marks an 11.0% drop from one year ago. Despite this month’s surge in sentiment, the index remains well below levels from six months ago following the presidential election.

The current conditions index increased for the first time in six months, while the expectations index rose for a second straight month. Notably, expectations for personal finances and business conditions improved significantly, soaring about 20% or more. With that said, consumers remain guarded about the economy’s trajectory and many of their views are consistent with an economic slowdown.

Inflation expectations eased for both near and long term. Year ahead expectations cooled for the first time in seven months, from 6.6% in May to 5.0% in June. Meanwhile, five-year expectations edged lower for a second consecutive month, to 4.0%. Despite softening expectations this month, both series remain historically high, reflecting consumers’ beliefs that tariffs and trade policy remain a risk to future prices.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer confidence.

Gross Domestic Product

The U.S. economy contracted for the first time in three years to start off 2025. According to the third estimate, real GDP — the inflation-adjusted measure of all goods and services produced in the U.S. — contracted at an annual rate of 0.5% in the first quarter of this year. This reflects a sharp downturn from Q4’s 2.5% growth and was lower than the -0.2% forecast.

In Q1, two of the four components made negative contributions to real GDP. Net exports were the primary driver behind the contraction, as imports surged in the first three months of the year ahead of anticipated tariffs, though less than previously reported. Government spending also declined. Partially offsetting these declines were increases in consumer spending, business investment, and exports. While still positive, consumer spending was significantly weaker than reported in the previous estimates. Business investment and exports were also downwardly revised.

Market Reactions

The S&P 500 finished the week at a new record high. The index posted a 3.4% weekly gain, snapping its two-week losing streak. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 3.4% last week. Meanwhile, the S&P Equal Weight Index was up 2.2% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 1.8%.

The 10-year Treasury yield finished the week at 4.29%, while the 2-year note finished at 3.73%.

The CME FedWatch Tool currently shows an 81% likelihood that the Fed will hold rates steady at their meeting at the end of July. Markets are pricing in three 25 basis point cuts this year coming at the September, October, and December meetings. Additionally, two 25 basis point cuts are projected in 2026.

Economic Data in the Week Ahead

The labor market will be in focus this week, with the highly anticipated June jobs report as the main event on Friday. Alongside this report, the JOLTS data, ADP's private payroll data, and initial jobless claims, will provide insights into the labor market’s health. Additionally, S&P Global and the Institute for Supply Management will release June’s Manufacturing and Services PMI readings, offering a glimpse into the economic activity of both sectors.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Read more commentaries by Advisor Perspectives