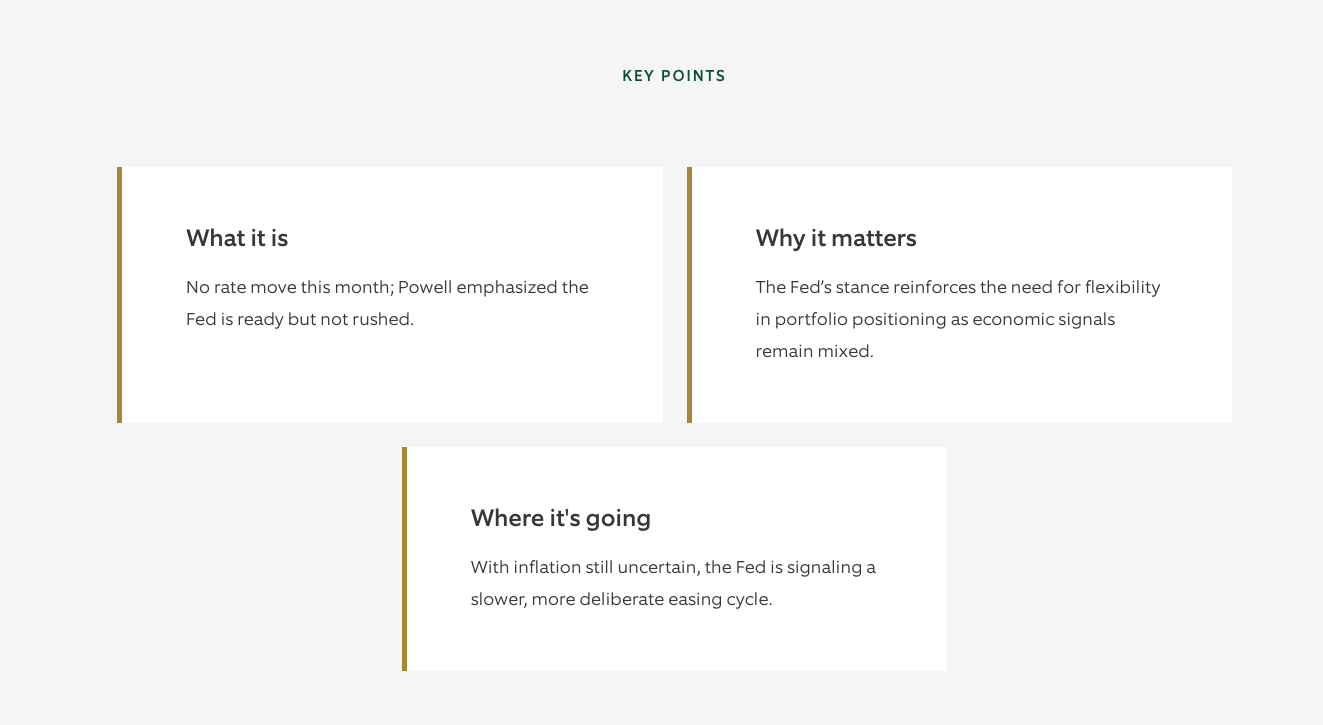

The Federal Open Market Committee’s (FOMC) decision Wednesday to leave the target range for the federal funds rate unchanged was widely anticipated. Market participants were keenly focused on any changes in the tone of Chair Powell’s press conference, as well as an updated Summary of Economic Projections (SEP), particularly the so-called ‘dot plot’. While a lot has transpired since the May FOMC meeting — including Moody’s downgrading of U.S. sovereign debt, various geopolitical and trade policy developments — the Committee’s stance on monetary policy hasn’t changed much. We, again, took the main message from Wednesday's meeting to be that, while uncertainty around the near-term path for the economy remains elevated — as are the risks to both sides of the FOMC’s dual mandate — the Committee still views its monetary policy as well positioned to wait for further clarity on the direction of the economy.

The post-meeting policy statement was little changed overall, but did clarify that, “Uncertainty about the economic outlook has diminished but remains elevated1 (our emphasis). The latest SEP continued to show the median participant expecting the equivalent of two 25-basis point (bp) cuts by the end of 2025, but by a narrower margin than in the previous dot-plot (March): Nine participants see only one cut or no cut this year as appropriate, one more than in March. The median projections for both 2026 (3.625%) and 2027 (3.375%) were both 25-bps higher relative to March, leaving the end-2027 dot even further above the long-term dot, which held steady at 3%.

The Chair’s press conference opened with prepared remarks that mostly repeated the language from the May press conference. The Committee believes that “the current stance of monetary policy leaves it well positioned to respond in a timely way to potential economic developments.”2 On the impact of trade policy, Powell posited that policymakers, “feel like [they’re] going to learn a great deal more over the summer on tariffs.”3 While at the same time saying, “the economy seems to be in solid shape … [and] the labor market is not crying out for a rate cut.”4 When asked about why they didn’t move policy towards a more neutral policy stance Wednesday, given elevated uncertainty, Powell countered that they, “have to be forward looking …”5 and take into account widely held expectations for inflation to increase in coming months. The Chair summarized future inflation passthroughs as, “very hard to predict … so that’s why [they] need to see some actual data to make better decisions…in the meantime [the Committee] can do that because the economy remains in solid condition.”6

Yields on U.S. Treasuries were little changed following Wednesday's FOMC statement and the Chair’s press conference, while equity markets gave back earlier gains. The futures-implied number of further rate cuts over the next twelve months was also little changed and remained at three to four 25-bp cuts.

What does this mean for portfolios we manage?

While the outcome of Wednesday's meeting was widely anticipated, we took Chair Powell’s comments throughout his press conference as consistent with our own view that the Committee remains attentive to risks on both sides of their mandate. While uncertainty has undoubtably remained elevated, we view current rates as not too far off fair value and are therefore neutral duration across the portfolios we manage.

1 Federal Reserve

2, 3, 4, 5, 6 ibid

Unless otherwise noted, all date is sourced from Bloomberg as of 06/18/2025.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee

© Northern Trust

Read more commentaries by Northern Trust