It's not often that UK stocks are singled out as a "favorite geopolitical hedge," as Citigroup Inc. strategists boldly stated last week. So perhaps the elegant stance would be to simply take the rare praise when it's so kindly offered. However, Citi’s Beata Manthey pointed to the wrong asset class. UK equities are hovering near an all-time high and seem incapable of making the next leap higher. Instead, a better alternative might be sterling corporate bonds, which offer juicy yields and better downside protection.

The main FTSE 100 index has risen 8% this year, and twice that in dollar-equivalent terms. That looks great versus a less-than 2% gain for the S&P 500 index. Nonetheless, it's only half the stellar gains seen in several euro indexes, and the more domestically representative FTSE 250 index is up less than 3%. But a longer perspective is needed. Despite a great first half, European gains remain puny versus the mighty US equity market, which has nearly doubled since the start of 2020, versus a 28% gain for the Stoxx 600 index, and just 16% for the moribund FTSE. It’s all about potential earnings growth, or the lack of it, as UK equities tread water with the sorry state of the economy.

It's worth remembering that after a parlous start to 2025, the S&P has powered back 20% since its tariff-induced early April nadir.

So choose your alternative investment destinations with care, as it's still all about how much relative exposure to the dollar makes sense. Some diversification is evidently prudent in these turbulent times. Sterling is nearly 10% higher versus the dollar this year, as is the euro, but this is very much predicated on greenback weakness. Even eight consecutive 25 basis-point rate cuts from the European Central Bank over the past year have failed to take the wind out of the euro’s sails; if the Bank of England becomes more proactive in cutting interest rates then the pound may well wilt fast.

The BOE referenced "slack" in the economy six times in its monetary policy summary last Thursday, triple the number in its prior report. According to Bloomberg Economics, policymakers will likely lower rates to 4% at its monetary policy review on August 7, and at least twice more out to February, but the risks are tilted toward them having to be more aggressive.

The FTSE 100 is stuffed full of old economy companies, big pharma and banks. There's definite value, as evidenced by 35 buyouts already this past year by private equity bargain hunters. But this makes the UK market much more a highly stock-selective environment, and less of a broad index bet. The compelling opportunities involve identifying the next hidden diamond to be acquired by foreign investors.

Though overseas interest is at the highest for three years, according to Goldman Sachs Group Inc., domestic investors have been net sellers all year, which is in direct contrast with European indexes. The new Labour government is making some noises about encouraging domestic pension funds to invest more at home, but none of it is remotely convincing — and there are zero incentives for retail equity investors.

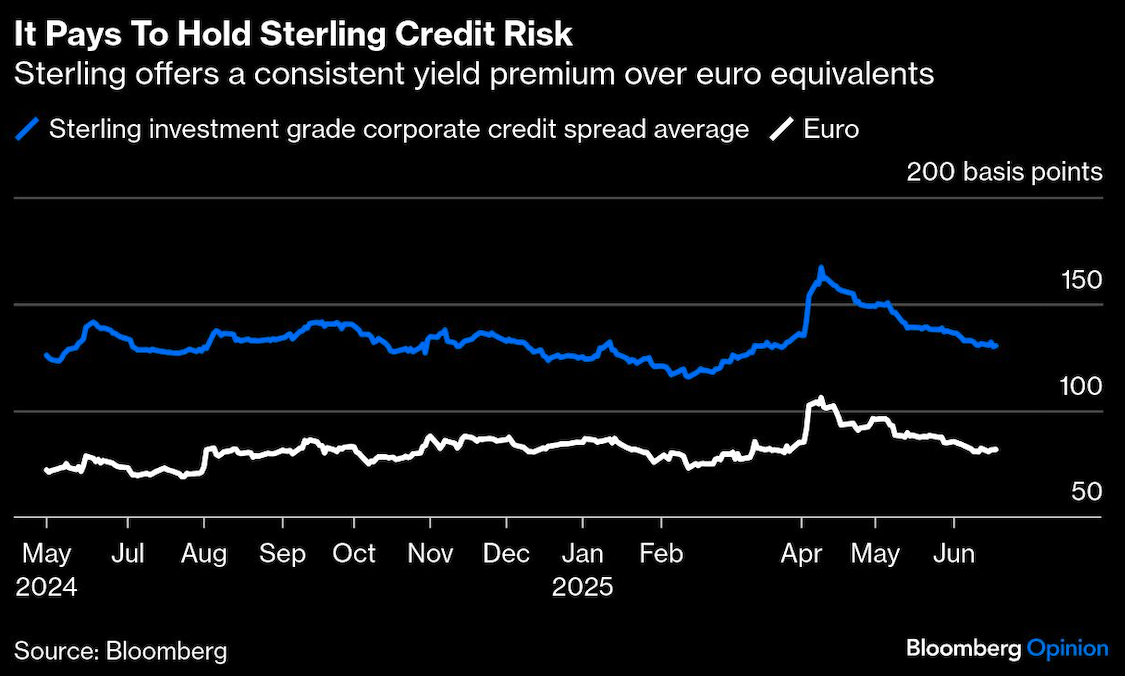

Fixed-income investors know there’s steady money to be had in a rate-cutting trend. Ten-year UK government bond yields at 4.5% are about the highest in the developed world, even surpassing US Treasuries, and nearly double German equivalents. Low-coupon gilts also have the advantage of being free of capital-gains taxes, and only incurring minimal dividend taxes. By playing safe in investment-grade sterling-denominated corporate bonds, there are relatively generous rewards, with an extra premium for a modest amount of credit risk. The yield premium offered over underlying gilt benchmarks is on average 130 basis points, considerably more than the euro equivalent of around 80 basis points.

Associated British Ports Holdings Ltd. (rated Baa2/A) sold a new £300 million ($400 million) 12-year bond earlier this month with a 5.875% coupon. It was five times oversubscribed and has tightened in credit spread a further 6 basis points since launch, after already being "walked in" by 22 basis points during the placing process.

Though there may be fewer new sterling bonds launched this year, the successful ABP deal illustrates investor demand is strong. High yields may deter some larger issuers, as there are cheaper arbitrage opportunities by issuing in either euros or dollars. But the opposite ought to be true for bond funds, with a cherry on top with wider credit spreads. Sterling is the third-largest global corporate bond market, and if interest rates fall as expected it's got to be one of the best value too. Buying UK equities might be compelling on an individual basis but being parked in safe corporate bonds is a lot less stressful.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.