My good friend Marc Lichtenfeld from the Oxford Club has always been savvy in following such strategies. I invite you to learn from his investment journey in this special Q&A.

Every summer for the past several decades, I have been organizing lunches for serious investors who spend at least part of their vacation time in eastern Long Island. Those attending include hedge fund wizards, real estate titans, corporate chiefs, thoughtful academics and a few others.

Many investors have started to scrutinize the shape of the US Treasury yield curve, worried that a potential yield-curve inversion would mean imminent recession. In our view, things aren’t that simple.

A review of last month’s market-moving events across countries and asset classes.

Japanese government bonds yield virtually zero. Yields on German bunds remain stuck below 50 basis points (bps). U.K. gilts yield only about 125 bps. Do non-U.S. bonds such as these hold any value to dollar-based investors?

Stocks hit the ground running to start the second half of 2018.

For three important reasons, leveraged U.S. Treasury bonds make sense as an ordinary investment.

This report may end up being the first in an ongoing series. I think of it as a “look inside my notebook,” as it literally represents a synopsis of the recent notes I put together for our latest Asset Allocation Working Group meeting. These represent a number of budding risks for the economy with which the markets are grappling. There are offsetting positives of course, but let’s leave this report to a look at some of the possible negatives.

So, as most of you know we were on a road trip last week. We flew into Albany, New York on Sunday only to be greeted with hotter temperatures than what we left in Florida. The mountain drive to Manchester, Vermont was spectacular, but hereto the temperatures were hotter than Florida.

The number of publicly listed companies in the U.S. has fallen steadily since 1997. More companies have delisted, in fact, than gone public in every year of the past 20 years except one, 2013. Put another way, the pool is getting smaller even while the population and economy are expanding.

Value investing is a proven long-term investing strategy that produces above-average results at below-average risk – if engaged in properly. However, there are four primary advantages to investing in undervalued dividend growth stocks that facilitate strong long-term performance while simultaneously lowering risk.

In a new white paper on GMO’s website, Jeremy Grantham updates his discussion of the threats posed by climate change, population growth and increasing environmental toxicity, and his perspective on the role investors can play in combating these threats. In “The Race of Our Lives Revisited” Grantham summarizes the current state of affairs and the likely impact on the future ability to feed the 11 billion people projected to live on Earth by 2100.

Portfolio managers Dan Ivascyn and Alfred Murata discuss the impact of higher market volatility and how they are positioning the Income Strategy for change ahead.

In this issue, Research Affiliates discusses positioning in emerging markets and why investors should care about the distinction between real and nominal returns.

The U.S. economy is going through a hot summer, but will cool off later this year.

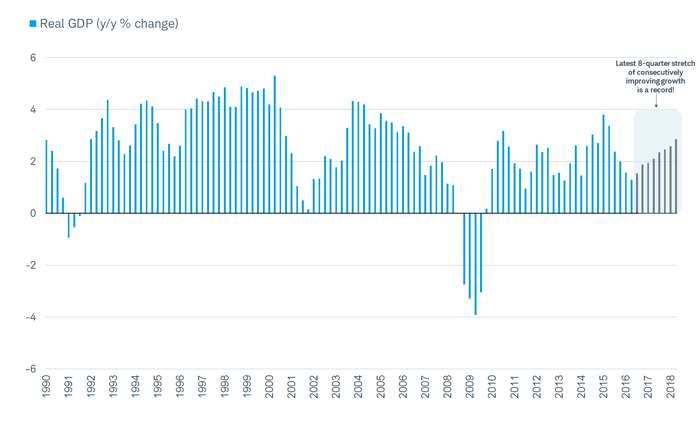

Synchronized global growth was one of the main themes coming into 2018. In the second quarter GDP in the U.S. was the strongest since 2014, even as growth around the world downshifted. While global growth will be decent in the second half of this year, growth has already slowed in the U.K, Europe, China, and Japan.

We don’t know how long ago we met Frederick “Shad” Rowe, but we are glad we did, because our conversations with him have been net worth changing.

Last month in Venezuela’s capital city of Caracas, a cup of coffee would have set you back 2 million bolivars. That’s up from only 2,300 bolivars 12 months ago, meaning the price of a cup of joe has jumped nearly 87,000 percent, according to Bloomberg’s Café Con Leche Index. And you thought Starbucks was expensive.

The macro data from the past month continues to mostly point to positive growth. On balance, the evidence suggests the imminent onset of a recession is unlikely. The largest risk to the economy is the escalation in trade war rhetoric.

Introduction Relative to historical norms the overall stock market as measured by the S&P 500 is overvalued with the current blended P/E ratio of 19.2. Historically, the S&P 500 would be considered fairly-valued when its P/E ratio was between 15 to 16.

Amid overall caution on credit, we believe short-dated investment grade corporate bonds offer a compelling risk/reward profile today.

The Fed acted as expected by not acting on interest rates; and although there was no associated press conference, the statement had a few nuggets of note.

In 2018, President Trump’s tweets on international trade have led to bouts of market volatility and concerns of a global economic slowdown. Against this backdrop, Franklin Templeton Multi-Asset Solutions’ Matthias Hoppe explains why he thinks economic fundamentals will determine the fate of the global economy more than Trump’s words will.

A landmark study looked back at more than 100 years of data and 23 countries to determine if there are reasons to believe the cross-sectional patterns in factor returns will persist, or whether they were just anomalies that tended to disappear after publication.

A single line chart is keeping an awful lot of investors up at night: the US Treasury yield curve. It’s been flattening steadily since the end of 2016 and is nearly the flattest it’s been since 2007. We all remember what happened after that.

In 2018, rising inflation, higher US interest rates and escalating trade tensions have led to concerns about global economic growth and bouts of equity-market volatility.

The Northern Trust Economics team shares its monthly perspective on the growth prospects and challenges ahead for key markets.

Rieder and Brownback argue that as we depart the era of QE, where rising tides lifted all boats, the income component of total return becomes ever more vital to investor prospects.

“Do you have the mental fortitude to accept huge gains?” is a line from The Elliott Wave Theorist’s Robert Prechter in an era gone by. But it is as true today as it was when first penned in the 1970s. And to do that, one has to ignore the ticker and hold stocks through a long market swing.

This article compares the performance of the premier investment-grade bond index, the AGG, to the performance of its subset U.S. Treasury index. Surprisingly, the long-term performance of the Treasury index is nearly that of the AGG, and outperformed it in several crucial periods.

The price of bitcoin surged above $8,000 on Tuesday for the first time since May after the Group of 20 (G20) meeting in Argentina concluded last weekend with little urgency to take regulatory action on cryptocurrencies. In a communiqué, finance ministers and central bank governors expressed confidence that the technology underlying alt-coins “can deliver significant benefits to the financial system and the broader economy.”

Evidence shows that the yield-curve slope and equity returns provide signals of similar direction in the economy, allowing investors to nowcast with relative confidence. Today, those signals indicate that several developed markets—in particular, Japan, Germany, and the United States—are ominously close to entering a correction phase.

Ultimately, we think the sell-off will prove transient and that the relationship of real yields to gold observed over the past decade will prevail.

It almost every article I have ever published, I talk about valuation in one manner or another. So much so, that readers have dubbed me Mr. Valuation. The primary reason I am so obsessed about valuation is because I believe it is one of the most important and yet mostly ignored and overlooked concepts in the investing world.

We see key factors beyond Brexit affecting the medium-term economic outlook for the U.K.

Market returns and economic growth have underlying drivers. At their core, extended periods of extraordinary growth and disappointing collapse reflect large moves in those drivers from one extreme to another. Extrapolation becomes a very bad idea once those extremes are reached.

Has President Trump introduced a Trump Put by lashing out about rising interest rates and calling for a weaker dollar? The market reacted swiftly - and rationally - albeit not the way Trump had intended. Let me explain.

The past quarter has had its fair share of market moving events, including another Federal Reserve (Fed) hike, a flattening yield curve, geo-political events and potential tariff wars. As we wrote last quarter, separating the signal from the noise remains challenging, but we feel it is the key to keeping perspective.

Readers of these missives know that we have been favorable on the midstream Master Limited Partnership (MLP) space for a number of months. The reasons for that strategy have often been mentioned in these letters. First, the midstream MLPs sold off when the upstream MLPs blew up with most of them going bankrupt.

Master limited partnership (MLP) investors received some good news last week. The Federal Energy Regulatory Commission (FERC) issued a final ruling that clarifies and softens a previous order issued in March, which would have disallowed a long-standing policy enabling MLPs to earn an income tax allowance in their pipeline rates.

We answer some of today’s most pressing investor questions—from the effect of trade wars with China to our expectations for rising rates and a correction in high yield.

We think the US economy remains in good shape, with the rate of growth potentially picking up, a labor market that is tight but attracting new workers, and inflation that still seems relatively subdued. Boosted by tax cuts and spending increases, these favorable conditions could continue for some time.

Despite plenty of news, there was little market reaction. In a summer week including many vacations, we have a modest economic calendar but plenty of earnings news.

With fears of a trade war looming over global large-cap stocks, the small-cap factor emerged as the clear winner of the second quarter. Specifically, small-cap low volatility/high dividend was the best-performing factor, followed by the small-cap versions of value, growth, equal weight and momentum.

An active manager worth his or her salt will manage risk as part of the deal, and risk management is exactly what you need when you live on a railroad track. It doesn’t have to be perfect, just good enough to mitigate the major drawdowns. If everybody else loses 40% and you only lose 25%, you’ll be way ahead of the crowd. And the right manager should avoid even that scenario and keep you near break-even.

There has been considerable discussion lately about the slowly inverting yield curve and what it may signal for growth prospects going forward. Commonly used as a proxy for the yield curve is the spread between 10-Year US Treasury yields and 2-Year US Treasury yields.

For much of this recovery and expansion, many have opined that this economic cycle would ultimately end very differently than those of the past. We have resisted this narrative and instead explained our belief that this cycle will indeed follow the same path and end like all others.

Topics of discussion are Economic Outlook – “It’s a Mad Mad Mad Mad World”, Market Outlook – “Volatility is the New Black”, Building “All Weather” Portfolios.

Will they or won’t they? With the U.S. yield curve flattening to new cycle lows, whether or not the Federal Reserve will stick to its planned rate-hike path is a key question – and could soon become the key question – for financial markets.

The yield spread between the 2-year and 10-year Treasury Note has narrowed to 25 basis points, its smallest spread since 2007. This has many investors worried the narrowing spread will lead to an inversion of the yield curve (when short-term rates exceed long-term rates) – which throughout history has often occurred prior to a recession.