Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Because Treasury bonds are the safest fixed-income securities, they have the lowest yields in the U.S. dollar universe. This can make them seem boring in a portfolio; something you must own to be prudent, but a drag on higher returns. The reality is different and will surprise you.

This article compares the performance of the premier investment-grade bond index, the Bloomberg Barclays Aggregate Bond Index (AGG), to the performance of its subset U.S. Treasury index. Surprisingly, the long-term performance of the Treasury index is nearly that of the AGG, and outperformed it in several crucial periods.

Treasury bonds perform nearly as well as investment-grade bonds over the long-term.

The AGG captures the performance of U.S. taxable investment-grade bonds. This includes Treasury bonds, investment-grade corporates, mortgage-backed bonds (MBS), commercial mortgage-backed bonds (CMBS), and other asset-backed bonds (ABS). Some of the largest and most familiar bond funds use the AGG as a benchmark, including the PIMCO Total Return Fund (PTTRX) and DoubleLine Total Return Bond Fund (DBLTX).

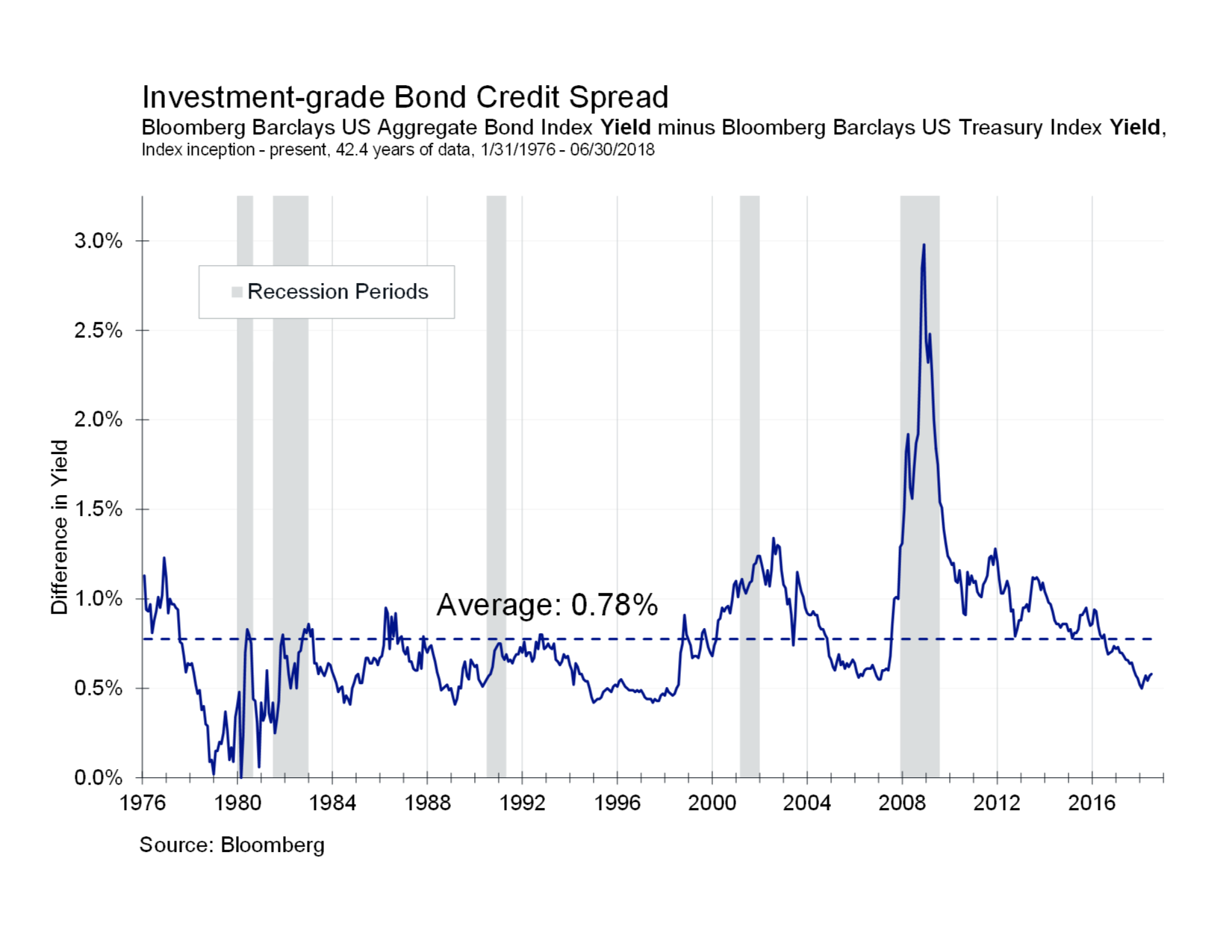

The performance of U.S. Treasury bonds, 38% of the index, is isolated in a subset index, the Bloomberg Barclays U.S. Treasury Index. As you might expect, because Treasury bonds have no credit risk, the yield of the Treasury index is less than that of the whole index. This yield difference (also known as the credit spread) varies as the perceived risk of default changes over time and averaged 0.78% over the full period (see chart below).

It is logical that the long-term performance difference of the two indices would be approximately the same, but it isn’t…not even close. Despite the Treasury index yielding 0.78% less, it performed just 0.15% annualized less over the full period (see chart below).

How could this be? There are three reasons. Bonds with credit only have higher yields because they have a chance of default. In the aggregate, if the market is efficient, the yield premium should compensate for the amount of bond defaults. Said another way: Over the long-term, there is no reason for the universe of credit bonds to outperform Treasury bonds; the performance loss from defaults should be equal to the yield premium. It is only when you bet on subsets of them that don’t default that an outperformance can develop.

Bonds may start in the index but, within their lifetime, may be downgraded to below investment grade and therefore are taken out of the index at distressed prices; regardless of whether they default.

The third reason is that, at any given time, the index is valued where all the bonds are marked-to-market and so their performance is the combination of cash flow as well as price changes from movements in interest rates.

No matter the reason, if Treasury bonds perform virtually as well as the AGG, what is the point of adding complexity where none is needed?

Credit bonds work against you when you need them most

It gets worse. The point of asset-class diversification is for one asset class to do well when others do poorly. In the case of bonds, they are needed and expected to perform the best when stocks do the worst. Said another way, bonds are expected to be counter-cyclical. But, the credit spread is pro-cyclical, which means that when the economy is doing poorly, the credit spread will tend to widen, putting pressure on credit-bond performance when stocks are performing poorly. In the credit-spread chart above, you will notice a general widening of the credit spread during recessions, and a general tightening outside them.

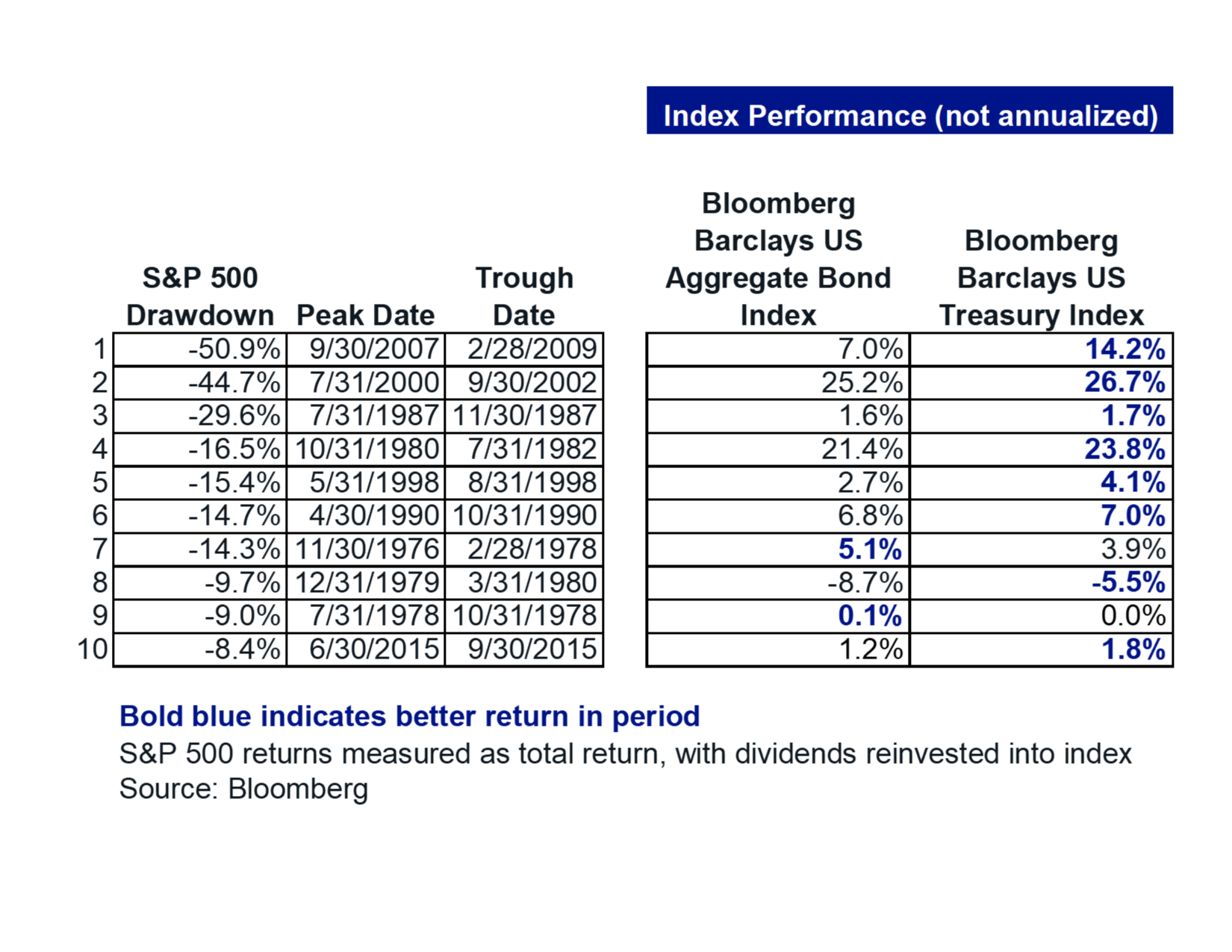

Consider performance between the two indices during large stock market losses. During the 10 largest S&P 500 drawdowns in the period since the index began, Treasury bonds have outperformed the AGG index in eight of those 10 (see table below).

10 largest S&P 500 drawdowns since 1976

Non-US Treasury investment-grade bonds bring with them a whole host of uncertainties an investor must bear. Without a meaningful performance boost, there is no reason to consider them. Treasury bonds do all the important fixed-income work investors need in a portfolio. Consider wisely whether other investment grade bonds belong in your portfolio. Are they just what the herd buys?

Eric Hickman is president of Kessler Investment Advisors, an advisory firm located in Denver, Colorado specializing in US Treasury bonds.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Read more articles by Eric Hickman