One of my greatest pet peeves as a long-time investment professional is the industries’ notion that stocks can be generally categorized into only two styles commonly referred to as growth investing or value investing.

Game theory is a useful framework for modeling aspects of sovereign debt recoveries, given that it models the interactions among debtors and creditors in the lending/borrowing "game." While there is a long-established set of precedents for Paris Club (U.S. & European) and multilateral (IMF, etc) creditors’ actions, we still have little available information about how China will act in debt negotiations.

The Federal Reserve is poised to cut interest rates at its July meeting. But how much will it cut?

The story of the first half of 2019 was the Fed reversing its position on raising rates. The gig of short-term fixes is almost up though and now is the time for investors to consider the longer-term implications for monetary policy.

Commodities were on mostly sound footing in the first half of 2019. The S&P GSCI returned more than 13 percent as of June 30, one of the best first six months in recent memory. It was not without its challenges, though.

In early 2007, delinquencies in subprime mortgages began to spike but few took notice. The first real headlines were made in June 2007 when two Bear Stearns hedge funds specializing in the area went down, but few were worried about Bear itself.

In this past weekend's newsletter we discussed the bull/bear case for S&P 3300. We now look at the #complacency behind it.

In the second quarter, US equity markets followed a now familiar trajectory. The S&P 500 Index closed at a new high on 30 April, buoyed by a de-escalation in trade tensions and rising expectations that central banks will ease policy to support slowing growth globally.

The economic calendar is normal and includes several important reports. I am especially interested in the housing data and retail sales. More important than the economic data is the start of earnings season.

As we reach the midpoint of 2019, some investors could be feeling a little queasy from the market’s ups and downs. Our advice is to remain patient. Gain more insight from our latest client-approved Investment Outlook.

While investors appear exuberant about the prospect for Fed easing, they seem largely unaware that initial Fed easings have almost invariably been associated with U.S. recessions. They’re running toward the fire.

When the Fed began a new easing cycle while the economy was expanding, stocks went up 3 months, 6 months, 9 months and 12 months later

The decade of the 1990s in India was an era of rapid change. The sudden rise of new choices and shifts in consumer preferences was stunning, in hindsight.

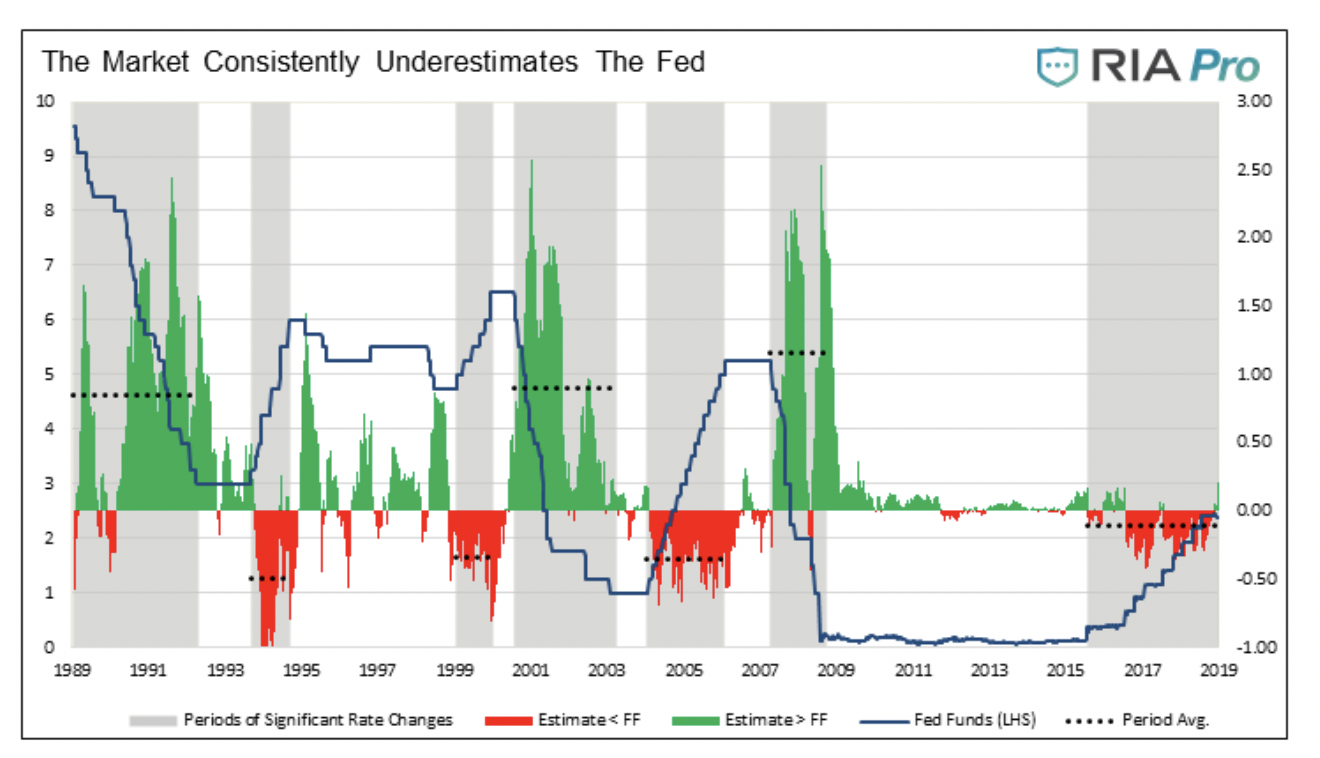

If you think the Fed may only lower rates by 50 or even 75 basis points, you are grossly underestimating them.

Yesterday BASF, the largest chemical company in the world, announced its earnings would fall well short of analyst estimates in the second quarter. Earnings season in the US begins in a few weeks. So, we ran through our charts to harvest any insights about how corporate earnings may play out.

Global equities advanced in the second quarter, but the path was rocky. Incoming earnings reports will provide important clues about how companies are coping with mounting challenges—from trade wars to global growth—and how investors should position.

Given their low yields, are TIPS are a good investment compared to nominal Treasury bonds?

The Northern Trust Economics team shares its outlook for U.S. economic growth, inflation, unemployment and interest rates.

We often get a sense of the relative uniformity in financial-market performance by looking at the indexes shown on Morningstar.com. Of the 145 stock, bond, target and commodity indexes, 131 were positive and 14 were negative for the second quarter of 2019.

Nonfarm payrolls rose more than expected in the initial estimate for June. The news sent equity futures lower, bond yields higher, and reduced the odds of more aggressive Fed policy action later this month.

A small "insurance" rate cut by the FOMC later this month appears warranted given ongoing weakness in housing, but the balance of the macro data remains positive, meaning a recession starting in 2019 is unlikely.

The S&P 500 is up 27% from its Christmas Eve low, and 19.3% this calendar year through the close on Friday – not including dividends. Last December, our forecast for 2019 was 3,100. We're just 3.7% away.

In this post we’ll highlight how this payroll report could either beat or miss expectations and what each case could mean for bonds, stocks, the USD and gold.

Investors to bond issuers: “We’ll pay you to borrow money from us.”

I’m very pleased to say that a satisfactory agreement was reached between HIVE and its strategic partner, Genesis Mining, so that the company can once again return to creating value for its shareholders.

Rick Rieder and Russ Brownback argue that while most investors are focusing primarily on trade-related supply chain disruptions today, they need to continue to situate this turmoil in the more fundamental changes at play in technology and demographic trends.

The quarter was a good one for investors, overcoming fears of an all-out U.S.-China trade war. The S&P 500 index rose roughly 4% for the quarter and was up ~17% for the year. It was the market’s best first half performance since 1997 and extended the more than decade long bull market.

US large banks announced significant dividend increases and share buyback authorizations following announcement of this year’s Federal Reserve stress test results on June 27th.

If you just woke from an 18-month slumber and looked at the market you might be fooled into thinking it’s gone nowhere; but what a ride it’s been.

Advocates of MMT insist that governments can and should print as much money as needed to fund massive public works, guarantee government jobs for the unemployed and much more. This is a recipe for runaway hyperinflation.

Trade tensions are felt around the world. Cautious central banks and flat yields don't stop a rally in equities. And more observations from a busy half year.

In the first half of 2019, major stock indexes including the S&P 500® reached new highs, yet the outlook for global economic growth softened. Recession risk has risen, and rising tariffs have created even more uncertainty.

Major secular drivers could disrupt the global economy and financial markets over the next three to five years. We share our views on risks and opportunities ahead.

In the following commentary, Portfolio Manager Ryan Kelley discusses the drivers behind the strong growth in the natural gas market in 2018, how tight inventories might cause more volatility in the gas price and the outlook for continued growth in natural gas exports.

As we review the general state of the global economy and investment markets, the word that keeps running through our mind is “asymmetrical”. We believe that the underlying fundamentals remain generally positive, but the market increasingly is “priced for perfection” and subject to downside shocks if what’s being priced in turns out differently than expected.

I have held AbbVie (ABBV) since it was originally spun off from Abbott Labs. Moreover, I have been aggressively adding to my position for clients needing current income and dividend growth.

An escalation in trade-war tensions between China and the U.S. has sparked a slowdown in global growth and a yield-curve inversion. Could global central bank easing and China stimulus turn the tide?

Earning income without taking excessive risk is a balancing act—and it can be hard to pull off in the late stages of a credit cycle. A credit barbell strategy can help investors stay on their feet.

With the price of gold trading above $1,430 an ounce as of June 25, now might be a good time for generalist investors to consider getting exposure to the yellow metal.

Of all the distinctions that investors might make in the coming few years, one that I expect will serve investors particularly well is the distinction between how the market responds to monetary policy when investors are inclined toward speculation, versus how the market responds when investors are inclined toward risk-aversion.

The last 18 months have been anything but boring, but if you had ignored the market over that time and only recently started paying attention, you may think that little has happened. The running in place analogy is probably better replaced by hiking a mountain.

After breaking out of a five-year trading range this week, gold surged above $1,400 for the first time since 2013 on expectations of a U.S. rate cut. Meanwhile, the global pool of negative-yielding bonds hit a fresh record high $13 trillion.

The narrative that the U.S. economy is in trouble – some say teetering on the edge of recession - has become so powerful and persuasive that few investors give it a second thought. So of course, they believe, the Fed should cut interest rates.

A few days of trading certainly does not make a trend, but we have our eyes on the nuanced message coming from the market – a message that has yet to give us an all clear signal.

On the latest edition of Market Week in Review, Quantitative Investment Strategist Dr. Kara Ng and Rob Cittadini, director, Americas institutional, discussed the recent rise in markets, deteriorating economic data and newfound optimism surrounding the China-U.S. trade war.

“Don’t tell me WHAT to buy, tell me WHEN to buy” is an old stock market “saw” that has survived the test of time. The reason it’s true is because a rising tide tends to lift all ships.

The march of demographics may be slow, but it is sure. And while the consequences of aging may seem far off into the future, they will be substantial. Unless we address them now, they will become much less manageable later.

I am a firm believer and ardent supporter of conducting comprehensive research and due diligence on any company (stock) you might consider investing in. However, I have also experienced the reality that far too many investors make their decisions based on opinions, emotions or vague ideas about a company...

Myriad economic, market and policy battles are raging today; providing some color, but lots of gray area as we look ahead to the second half of the year.