Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

If you think the Fed may only lower rates by 50 or even 75 basis points, you are grossly underestimating them.

Currently, the December 2019 Fed Funds futures contract implies that the Fed will reduce the Fed Funds rate by nearly 75 basis points (0.75%) by the end of the year. While 75 basis points may seem aggressive, if the Fed does embark on a rate-cutting policy and history proves reliable, we should prepare ourselves for much more.

The prospect of three 25 basis point rate cuts is hard to grasp given that the unemployment rate is at 50-year lows, economic growth has begun to slow only after a period of above-average growth, and inflation remains near the Fed’s 2% goal. Interest rate markets are looking ahead and collectively expressing deep concerns based on slowing global growth, trade wars, and diminishing fiscal stimulus that propelled the economy over the past two years. Meanwhile, credit spreads and stock market prices imply a recession is not in the cards.

To make sense of the implications stemming from the Fed Funds futures market, it is helpful to assess how well it has predicted Fed Funds rates historically. With this analysis, we can hopefully avoid getting caught flat-footed if the Fed not only lowers rates but lowers them more aggressively than the market implies.

Fed Funds versus Fed Funds futures

Before moving ahead, let’s define Fed Funds futures. The futures contracts traded on the Chicago Mercantile Exchange (CME), reflect the daily average Fed Funds interest rate that traders, speculator, and hedgers think will occur for specific one calendar month periods in the future. For instance, the August 2019 contract, trades at 2.03%, implying the market’s belief that the Fed Funds rate will be .37% lower than the current 2.40 % Fed Funds rate. For pricing on all Fed Funds futures contracts, click here.

To analyze the predictive power of Fed Funds futures, I compared the Fed Funds rate in certain months to what was implied by the futures contract for that month six months earlier. The following example helps clarify this concept. The Fed Funds rate averaged 2.39% in May. Six months ago, the May 2019 Fed Funds future contract traded at 2.50%. Therefore, six months ago, the market overestimated the Fed Funds rate for May 2019 by .11%. As an aside, the difference is likely due to the recent change in the Fed’s IOER rate.

I was surprised by the conclusions drawn from my long term analysis of Fed Funds futures against the prevailing Fed Funds rate in the future.

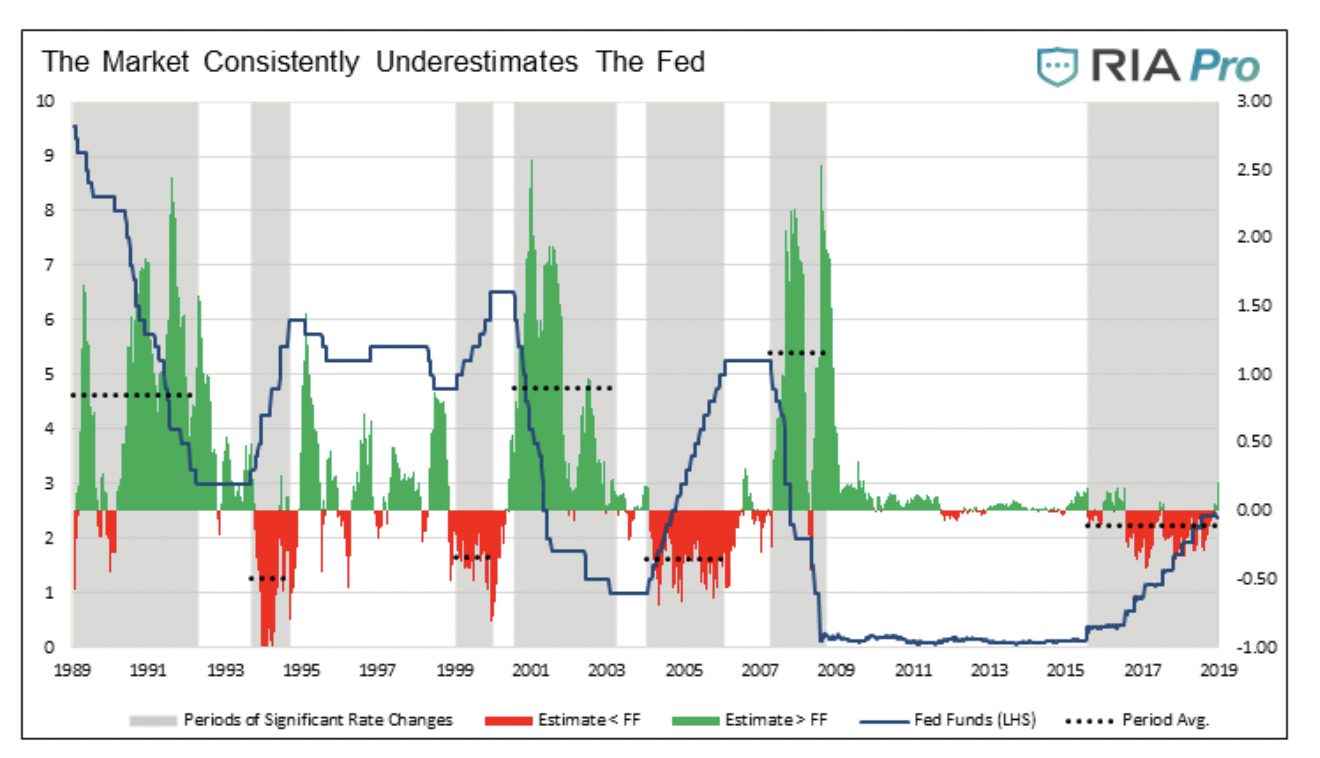

The graph below tracks the comparative differentials (Fed Funds vs. Fed Fund futures) using the methodology outlined above. The gray rectangular areas represent periods where the Fed was systematically raising or lowering the Fed funds rate (blue line). The difference between Fed Funds and the futures contracts, colored green or red, calculates how much the market over (green) or under (red) estimated what the Fed Funds rate would ultimately be. In this analysis, the term overestimate means Fed Funds futures thought Fed Funds would be higher than it ultimately was. The term underestimate, means the market expectations were lower than what actually transpired.

To further help you understand the analysis I provide two additional graphs below, covering the most recent periods when the Fed was increasing and decreasing the Fed Funds rate.

Data Courtesy Bloomberg

Data Courtesy Bloomberg

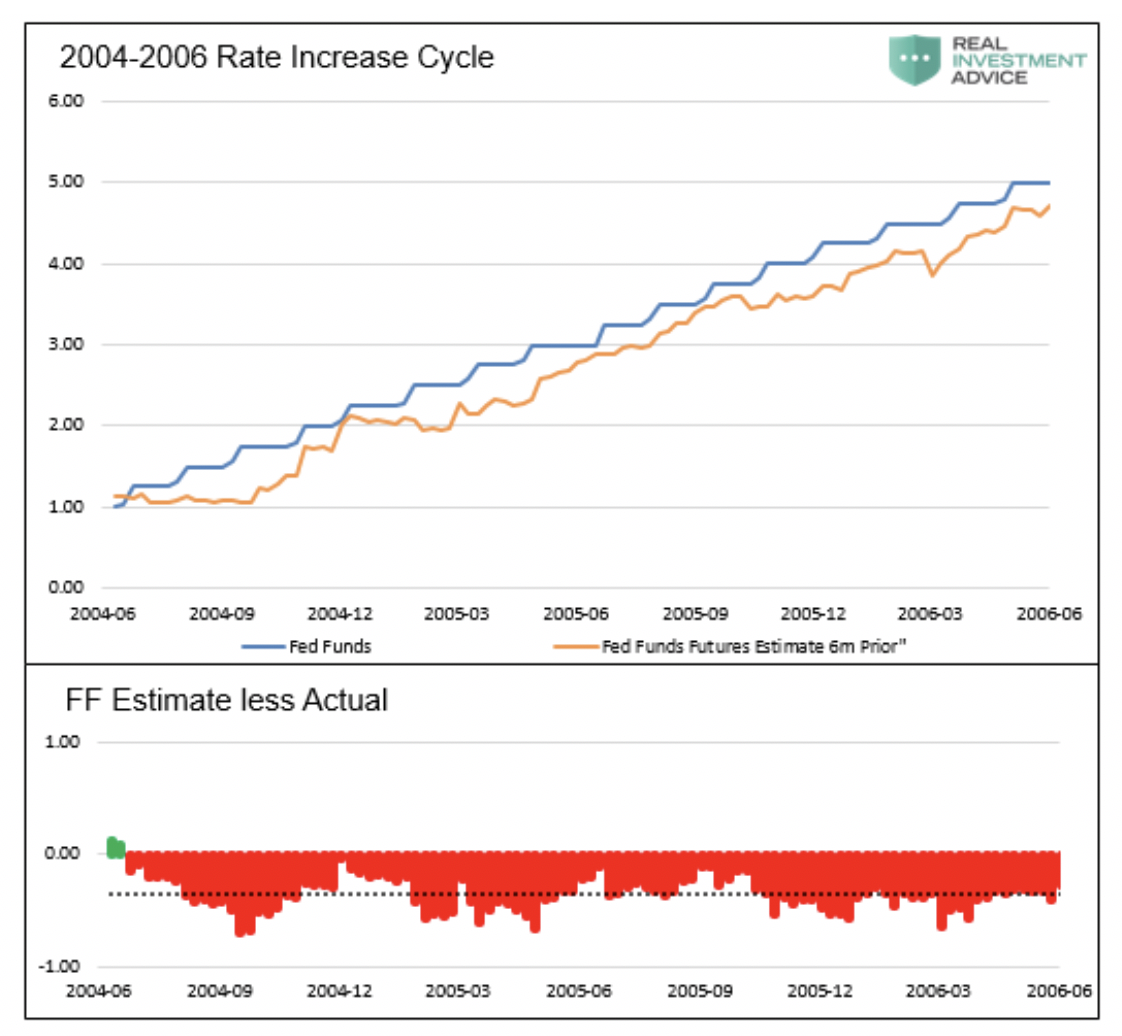

Looking at the 2004-2006 rate hike cycle above, we see that the market consistently underestimated (red bars) the pace of Fed Funds rate increases.

Data Courtesy Bloomberg

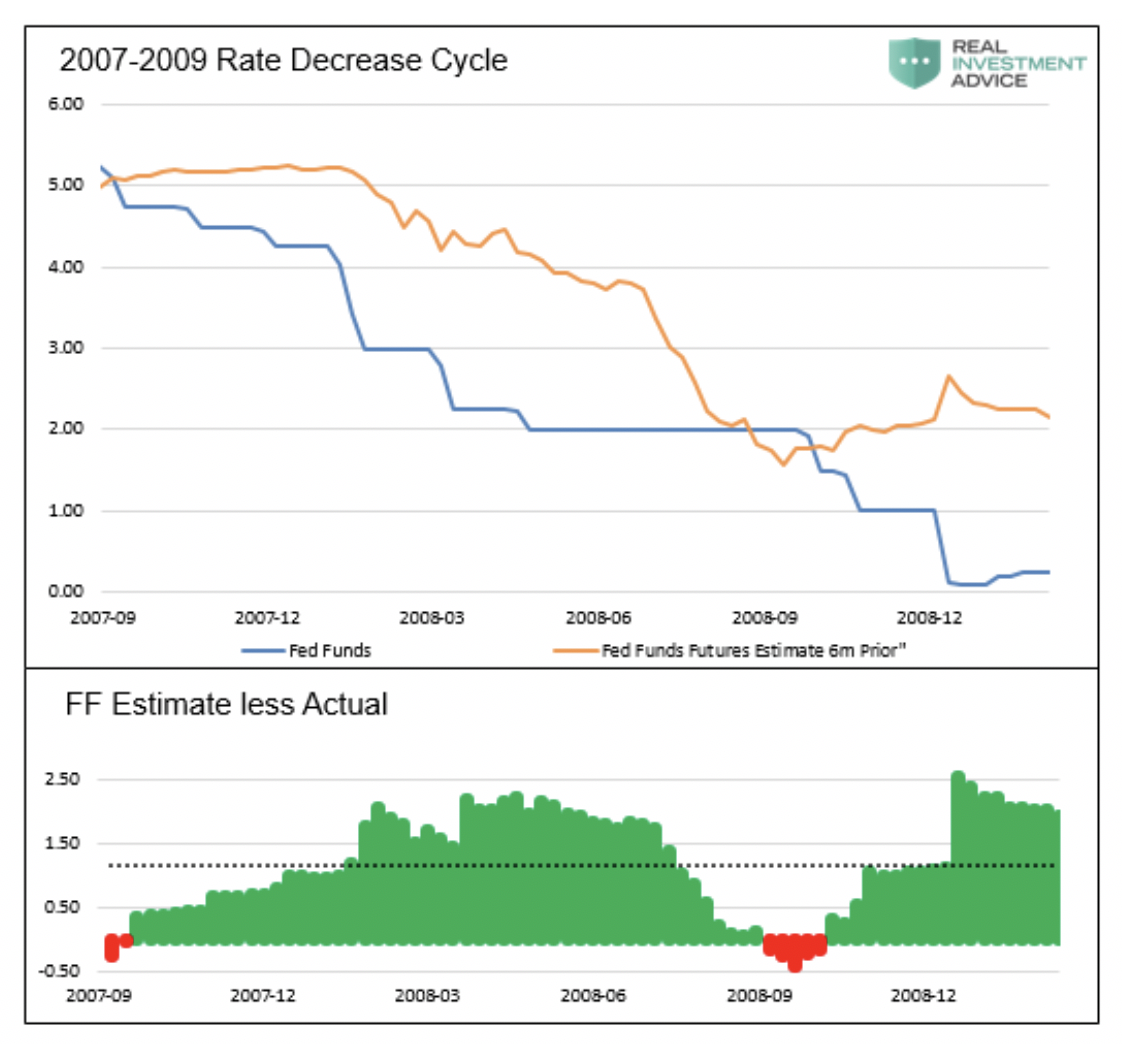

During the 2007-2009 rate cut cycle, the market consistently thought Fed Funds rates would be higher (green bars) than what truly prevailed.

As shown in the graphs above, the market has underestimated the Fed’s intent to raise and lower rates every single time they changed the course of monetary policy meaningfully. The dotted lines highlight that the market has underestimated rate cuts by 1% on average, but at times during the last three rate-cutting cycles, market expectations were short by over 2%. The market has underestimated rate increases by about 35 basis points on average.

Summary

If the Fed initiates rate cuts and if the data in the graphs prove prescient, then current estimates for a Fed Funds rate of 1.50% to 1.75% in the spring of 2020 may be well above what we ultimately see. Taking it a step further, it is not farfetched to think that that Fed Funds rate could be back at the zero-bound, or even negative, at some point sooner than anyone can fathom today.

Heading into the financial crisis, it took the Fed 15 months to go from a 5.25% Fed funds rate to zero. Given their sensitivities today, how much faster might they respond to an economic slowdown or financial market dislocation from the current level of 2.25%?

Equity valuations are at or near record highs, in many cases surpassing those of the roaring 1920s and butting up against those of the late 1990s. If the Fed needs to cut rates aggressively, it will likely be the result of an economy that is heading into an imminent recession if not already in recession. With the double-digit earnings growth trajectory currently implied by equity valuations, a recession would prove extremely damaging to stock prices.

Treasury yields have fallen sharply recently across the entire curve. If the Fed lowers rates and is more aggressive than anyone believes, the likelihood of much lower rates and generous price appreciation for high-quality bondholders should not be underestimated.

The market has a long history of grossly underestimating, in both directions, what the Fed will do. The implications to stocks and bonds can be meaningful. To the extent one is inclined and so moved to exercise prudence, now seems to be a unique opportunity to have a plan and take action when necessary.

Michael Lebowitz is the founding partner of 720 Global and partner with Real Investment Advice. We assist our clients in differentiating themselves from the crowd with a focus on value, performance and a clear, lucid assessment of global market and economic dynamics. For more information about our upcoming subscription service RIA Pro, please contact us at 301.466.1204 or email [email protected].

More Fixed Income Topics >