“What, Me Worry?”

Alfred E. Neuman (1956-2019)

Fictitious mascot and cover boy of the American humor magazine Mad

In early 2007, delinquencies in subprime mortgages began to spike but few took notice. The first real headlines were made in June 2007 when two Bear Stearns hedge funds specializing in the area went down, but few were worried about Bear itself. By September 2007 the problems were widespread enough for the Fed to act aggressively and cut interest rates a full half point instead of the typical quarter point move, in an effort to make sure they weren't "behind the curve". Thankfully, due to these bold efforts, by early October 2007, well after the start of the troubles, the stock market was hitting all-time highs, and they all lived happily ever after. Just kidding.

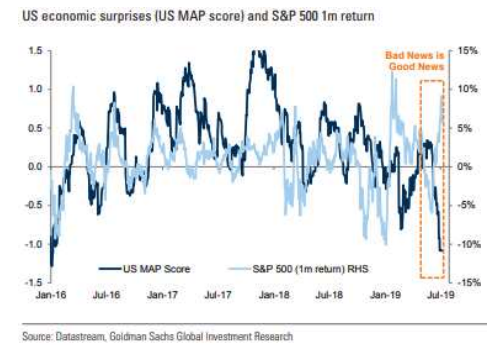

This is what today feels like. Not because we think we are about to have a financial crisis, but because there are (probably less serious1) economic clouds on the horizon, and the Fed has recognized them, and therefore all but promised to cut rates, and as a result stocks have zoomed to new all-time highs. The S&P 500 just passed 3,000 for the first time; the Dow just passed 27,000 for the first time. Back in 2007, we were scratching our heads and wondering why stocks were focusing only on the rate cuts and ignoring the reasons for the rate cuts; we are scratching our heads today.

We are worried. To be fair, we are also probably wrong, because things are usually fine and the stock market usually goes up, but we are worried. It is not just us. There are several important entities that agree with us.

The most important entity that agrees with us is the bond market. Usually bonds and stocks move in opposite directions. When things are good, stocks are up and bonds are down, and when things are troubling, stocks are down and bonds are up. Recently, they’ve both been moving up. So stocks say things are fine, whereas bonds say things are not fine. When equities and credit disagree, generally it is thought better to listen to bonds as the “smarter” market, especially when it comes to the macro economy2. Stocks can get buoyed by manic sentiment and thoughts of unlimited upside. Bonds have extremely limited upside and mainly worry about the downside.

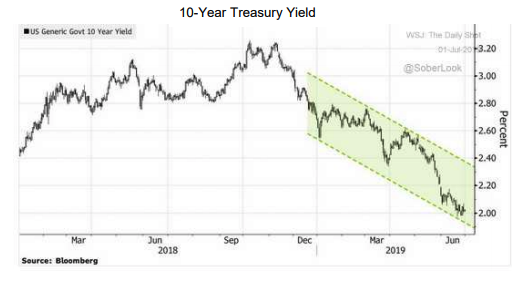

Bonds are not only broadcasting their economic worries through lower yields, but also by the inversion of the yield curve, about which we have written extensively in the last two letters.

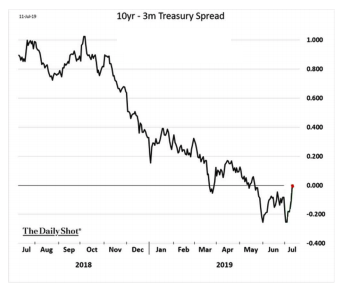

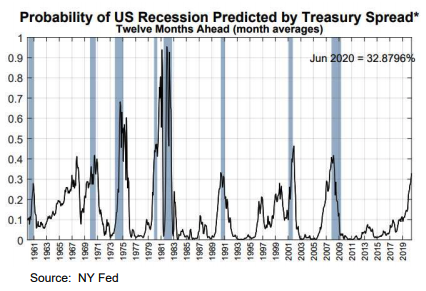

Here we present a series of updates. In April we wrote that the spread between the 10-year and 3-month Treasury yields (10yr-3m) had inverted and uninverted. Since then it has spent a lot more time in firmly inverted territory (spread below zero on the below chart).

Last quarter we included the chart on the next page, which predicts the odds of a recession in the next year based on the abovementioned 10yr-3m spread. We include this chart again and note that the odds of a recession by June 2020 have increased over the last quarter from 27% to 33%.

Finally, a note on timing. Last quarter we wrote that given the average time lag between an inversion of the 10yr-3m yield curve, a stock market peak, and a recession, one might expect the stock market top in September 2019, with a recession following four months after in January 20203. Given this outlook, perhaps things are right on schedule and we should not in the least bit be surprised at the market’s recent new highs.

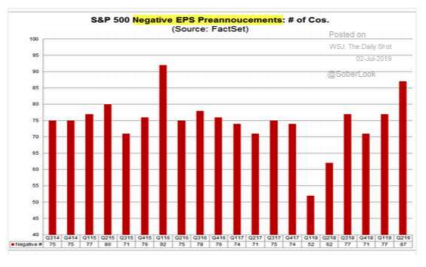

Consumers are not worried – consumer confidence is at or near all-time highs. Businesses, however, worried more and more, are beginning to preannounce negative EPS results. Analysts are taking note and lowering their 2019 earnings estimates.

Consumers are not the most forward looking among this group. We recall a Wall Street Journal news story in early 2008 declaring that despite all the talk of panic on Wall Street, that Main Street seemed to be doing just fine. The economy would later be declared to have officially been in recession at that point, but no one knew it at the time.

The last group we will call out that is worried alongside us is small cap stocks. The underperformance of small cap stocks versus the headline indexes is a classic “late cycle” sign. This gap has been widening since January as can be seen in the chart to the right. Note also that while the chart shows the S&P 500 ETF making new all-time highs, the small cap iShares Russell 2000 ETF is still some 10% below its own previous high reached in September 2018.

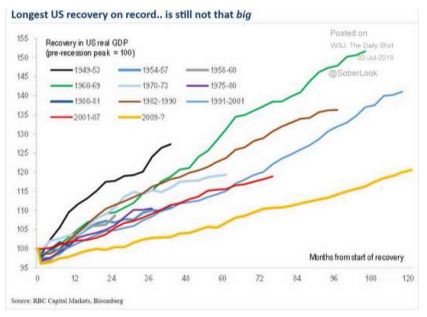

In sum, we think it likely that we are currently undergoing a topping of what has been a decade-long investment and economic cycle. Indeed, the current U.S. economic expansion recently became the longest on record. While unprecedented occurrences happen all the time, one might expect a downturn could come at any time based on this alone.

Unfortunately, there are a number of other ominous signs as well... and they are coming from leading indicators. Concurrent indicators, like employment and consumer sentiment, are in good shape... for now. In general, the rest of the world is in much worse shape than the U.S. But the U.S. situation appears to be catching up to the rest of the world and getting “less good” each day.

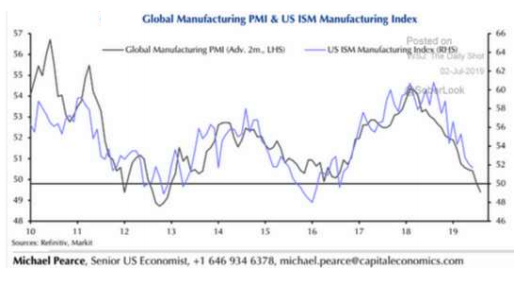

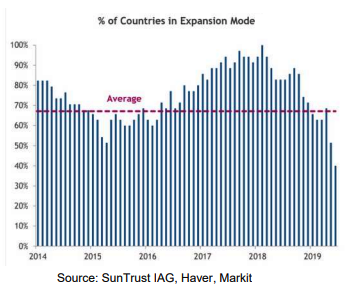

We have written before about the predictive power of Purchasing Manager Indexes (PMIs). As a reminder, a reading below 50 indicates contraction. The chart below shows how the Global Manufacturing PMI recently breached that threshold, after falling for fourteen months straight, the most protracted decline on record. Though still above 50, in expansion mode, the U.S. manufacturing PMIs have been similarly declining. Before anything can fall, it must first slow its rate of ascent...

The following chart shows the same global PMI data in a different manner. It shows the majority of the world’s economies now have manufacturing PMIs below 50 (in contraction). The deterioration is striking.

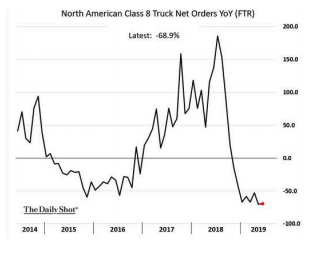

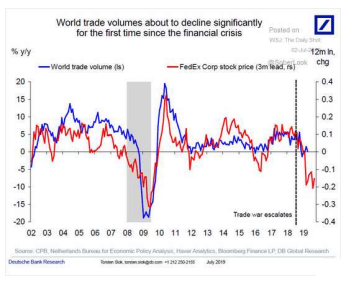

Shipping activity is also generally considered one of the most forwardlooking economic indicators, and the decline in semi-truck orders and FedEx’s stock price add to this worrying backdrop.

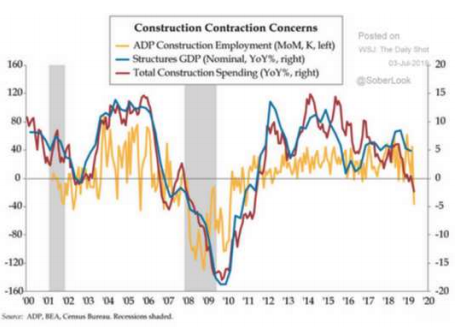

Construction spending and employment have declined year over year. Will the promised rate cuts be enough to turn this trend around? It wasn’t last time.

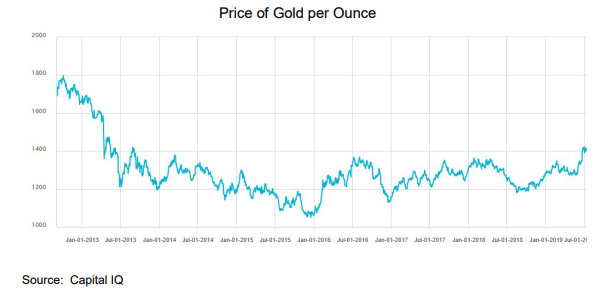

Finally, the price of gold is in a multi-year breakout, reaching heights not seen since the last time the global economy was really in turmoil in the aftermath of serious fears about a possible breakup of the Euro. Gold is an asset that investors usually seek in time of turmoil, so perhaps it is sniffing out future uncertainty... or the massive monetary easing that would likely accompany such conditions.

Any downturn in the economy might prove doubly risky for the stock market in the long term. That is because a weak economy increases the chances that Democrats will be swept into power in the 2020 elections. We do not think Democrats in general are inherently worse for the economy or the stock market4. However, front-runner Joe Biden is on record saying “the first thing he would do” upon getting into office would be to reverse the Trump tax cuts5. Ignoring any thoughts or opinions on whether or not this would be good for the country, it would absolutely undoubtedly be very bad for the stock market. We wrote in our Q4 2017 letter (http://www.knightsb.com/4Q17_quarterly_letter.pdf) just how good these tax cuts were for the market, and they would surely work in reverse on their removal. A return to a 35% corporate tax rate from the current 21% would represent an immediate 18% hit to profits. We believe the possible reversal (even if just partial) of the reduction in the corporate tax cut is one of the most underappreciated longterm risks to the stock market6.

We’ve written a bearish letter. This is how we see it. But it is completely possible that the patterns of history we’ve identified will be broken (as they sometimes are) and despite the inverted yield curve and negative leading indicators abroad, that our economy will continue charging along and shatter all records. Nevertheless, as stewards of your capital we feel compelled to play what we believe are the odds, doing our best to harden the portfolio against potential difficulties by selling many of our cyclical positions, and holding a portfolio average 13% of cash, a position which not only infuses defensiveness, but also affords the dry powder to invest at a more promising future time7. Perhaps due to the weakness in small capitalization stocks we referenced earlier, we are already seeing a bit more bargains in the market than we had previously, but we’re doing our best to hold off and only pick up the choicest candidates due to our macro concerns. If the economic and stock market juggernauts continue, we may not benefit as much as others, but if it is not so, we hope this prudence will be rewarded when the storm breaks.

For a while now it seems we have been warning, all is not well, be cautious. And yet, even according to us, it’s rather likely we’ll be writing this same letter further into the future before these warnings prove warranted. Rest assured, however, that one day we’ll be writing that all is not lost, and it is time to get aggressive.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 To be fair, the problems didn’t look that serious in October 2007 either. But in seriousness, any trouble we are expecting at this point would be a “run of the mill” recession, not a once-in-three-generations financial crisis.

2 Fun fact: the U.S. bond market, at $40 trillion in total value, is larger than the $30 trillion domestic stock market.

3 It should be reinforced that these are the dates you come up with by applying the average time lag between these events. The actual events themselves often happened much faster or slower. We would indeed be very surprised if the dates we lay out above correctly predict events going forward with any precision. It’s also worth noting that a recession beginning in January might not be officially reported as such until June or later.

4 Most people are surprised to learn that historically the economy has actually grown faster under Democratic compared to Republican administrations. https://pubs.aeaweb.org/doi/pdfplus/10.1257/aer.20140913

5 It is entirely possible that Biden may not actually follow through on this. Once upon a time it was also an Obama Democratic party goal to reduce the corporate tax rate to a level closer to that of our international competitors.

6 Our current large government deficits, which would be worsened in any recession, increase the likelihood of this reversal. 7 As it did in December 2018 when we were able to fully deploy our cash position to get fully invested when the market was down 20%.

© Knightsbridge Asset Management, LLC

More ETF Topics >