Investors to bond issuers: “We’ll pay you to borrow money from us.”

As interest rates around the globe have edged lower in recent weeks, the amount of negative-yielding debt has been growing.

Year to date as of June 26, 2019, 186 bonds totaling $1.4 trillion have been issued at negative yields, already surpassing 2018’s total of $309 billion.

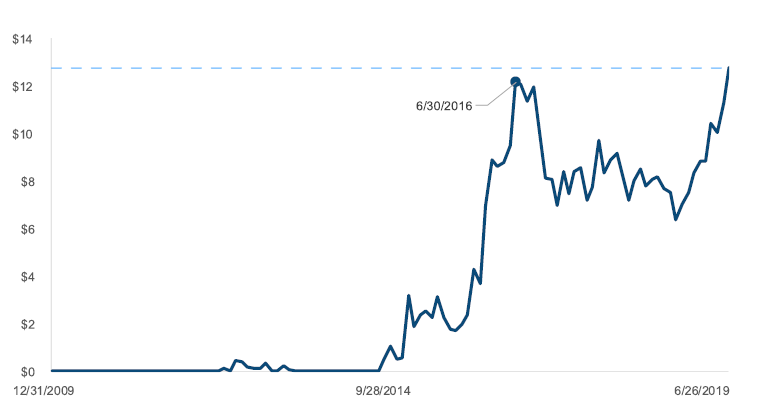

The market value of the bonds in the Bloomberg Barclays Global Aggregate Index is $54.6 trillion (as of June 26, 2019). Of that amount, $12.9 trillion (23.6%) currently has a negative yield; its weighted average yield is -0.31% with a maturity of 5.1 years.

This current amount surpasses its previous high of $12.2 trillion during the summer of 2016 when yields in many countries touched their all-time low. At that time, the percent of the index with a negative yield reached 25.7%.

On its face, the global bond market, with its inverted yield curves and $trillions in negative-yielding debt, would seem to be in defiance of the laws of not only finance, but of human nature itself.

Lenders take on the risk of lending with the expectation of earning a profit. Outside a deliberate act of charity, it goes against our nature to lend money knowing it will result in a loss. So what are investors to make of this? What circumstances or conditions would rationalize such a transaction?

A simple thought experiment may offer some insight. Suppose Mr. Smith lends Mr. Jones $1 million for three years. At the end of three years, Mr. Smith (the lender) will pay Mr. Jones (the borrower) $15,000 when Mr. Jones repays the $1 million. What could possibly motivate Mr. Smith to make such a loan?

Barring charitable intentions, the only reason Mr. Smith would lend at such terms is if he expects the purchasing power of his $1 million to have increased by more than $15,000 three years from now.

Such a phenomenon is the opposite of inflation, otherwise known as deflation.

While there is currently no deflation occurring in any of the world’s major economies, these negative yields offer some indication of the bond market’s projection for future deflation.

If the bond market is right and the world is indeed headed for a deflationary period, it would seem that the Fed can’t ease policy fast enough.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.