Emerging-market investors seem to have a lot going for them right now -- and the renewed weakness in the U.S. dollar is adding to the bullish mood.

Cast a gaze across global bond markets and it’s a sea of calm. Yields are close to record lows, volatility is nowhere to be seen and central banks are still ploughing trillions of dollars into the economy to help foster a recovery.

Short-term interest rates are approaching zero percent and will likely be negative shortly. The culprit is an unusual circumstance at the U.S. Treasury.

It isn't over and financial markets don't accept that yet. I realize suggesting anything negative about the virus is misanthropic, but the truth matters and the optics are misleading.

Happy Year of the Ox! Today China and a number of other Asian countries celebrate the Lunar New Year, also known as the Spring Festival.

Rob Arnott: “There hasn’t been a better time to be a value investor at any other time in my career. I look back at the tech bubble and I never thought I would see valuations stretched the way they were then. We're back to that, and then some." We invite you to revisit “Reports of Value’s Death Have Been Greatly Exaggerated” now published in the Financial Analysts Journal.

Hope is high that economic growth will accelerate as more people are vaccinated against COVID-19, but so far economic data has been lackluster. Meanwhile, bond investors are expecting inflation despite signs that the economic recovery’s momentum may be stalling. Why does everything seem so disconnected?

Recent volatility and high valuations underscore the need to be selective, but risk premiums still justify a moderately pro-risk stance, in our view.

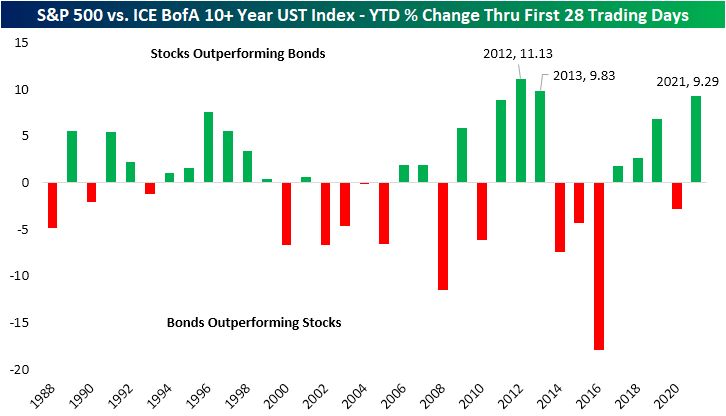

Investors awash in optimism have bid up equities to their best start of the year relative to bonds in almost a decade.

Yields on two-year Treasury yields briefly printed a record low under 0.1% on Thursday as cash trading got underway in London after a holiday in Asia.

Stephen Dover, our Chief Market Strategist and Head of Franklin Templeton Investment Institute, shares four investment themes he’s thinking about as the world recovers from the COVID-19 pandemic.

Federal Reserve Chair Jerome Powell said the U.S. job market remains a long way from a full recovery and called on both lawmakers and the private sector to support workers.

Having strongly underperformed the wider stock market in 2020, high-dividend stocks have shown early signs of a rebound in recent weeks.

I don’t say this often, but Fed Chairman Jerome Powell is wrong. Regular readers of our investor letters and other publications will recall that we regularly cite Chairman Powell as doing the best he can with the levers he has while arguing correctly for others to do their part.

Rick Rieder and team think that today’s potent policy cocktail holds important implications for the path of economic growth, markets and the value of a dollar.

Fortunately, human behavior has a history of repeating itself at extremes. The worst buying decisions are made at the top. Just like bonds, the convexity is true when yields rise going forward. It’s a slippery slope and could be vexing.

In making the case for a mammoth $1.9 trillion economic relief package, President Joe Biden and his acolytes had maintained that economists across the board agreed that now is the time to go big in the fight against the pandemic.

For the first time in a long time, there’s a conversation on Wall Street about when equities might start to feel the heat from reflation signals in the bond market.

It was a dinner conversation with former Federal Reserve Chairman Ben Bernanke in early 2020 that convinced Cesar Perez Ruiz that the golden age of bond investing was over.

At some point, interest rates will move higher. Advisors must understand the inherent risks, and proactively evaluate alternatives for their fixed income portfolios to manage through successfully.

Any surge in inflation will likely not last for long, but Italy's economic troubles and the shift in rental markets may endure.

With fixed income yields stubbornly low, should clients prepay their mortgage instead of investing in bonds? I argue this question is based on a false equivalence.

The pandemic has accelerated an evolution in bond trading, and it is already making a difference for investors—if bond managers have embraced tech-enabled trading.

It’s hoped that an extra $1,400 in the pockets of everyday Americans may help support lagging U.S. consumption. We believe the stimulus, along with improved vaccine roll out, may also help support commercial air travel.

Today I want to discuss an arcane-sounding but incredibly important term you need to know: Yield Curve Control. Several central banks are already using it and I see a strong possibility the Fed will join them. But first we must again consider the Gripping Hand.

Effective vaccines, historic fiscal stimulus, Democratic Party control of the legislature, even more stimulus, reopening economies, 6% U.S. real GDP (gross domestic product) growth, 25% U.S. EPS (earnings per share) growth, and maybe even an infrastructure plan sprinkled on top.

CIO Robert Horrocks, reviews a topsy-turvy 2020 and shares the reasons for his relative optimism for Asia and the emerging markets in 2021.

Treasury yields continued to march higher in January, with the move again concentrated in longer maturities. Mortgage spreads tightened slightly, while corporate bond spreads were mostly mixed. The market remains stuck between the push/pull of the prospect for greater fiscal stimulus and ongoing vaccine rollout versus continued lockdowns and the greatest one-month mortality rate since the pandemic began nearly a year ago.

The U.S. Treasury held steady its planned issuance of longer-dated securities at a quarterly debt auction next week as the department awaits the result of the Biden administration’s push for a fresh coronavirus relief package.

Discerning investors could eke more gains out of developing-nation bonds, but the bulk of the rally in the riskiest corners of the market may have passed.

Cyclically oriented value stocks could make a comeback in 2021, yet there’s still a place for durable growers in a balanced equity portfolio.

Jerome Powell doesn’t want to talk about scaling back massive Federal Reserve asset purchases -- at least not yet -- but it’s only a question of time before the discussion resumes and that might not be a bad thing.

Collateralized loan obligations are the largest source of demand in the loan market. Cheryl Stober breaks down some key drivers of CLO manager behavior.

In this piece, BlackRock Global Allocation Fund portfolio manager Russ Koesterich discusses the implications of a rise in stock-bonds correlations.

February begins with a stack of important economic scorecards. Among them are the last of the fourth-quarter corporate earnings reports, last week’s assessment of the 2020 gross domestic product (GDP), unemployment figures, consumer spending, as well as all the other regular reports that give us a snapshot of our recent economic history.

Emerging markets seek a sustainable solution to debts, and the Fed takes a step toward sustainability.

I’m often asked if I foresee inflation or deflation. Both are possible in their own ways, and frankly I feel a little funny telling people I think we will see both. I would just like to have a growing economy and dependable money that holds its value.

Bank loans offer some of the highest yields in the current interest rate environment. We believe their unique characteristics may prevent many investors from considering them, but it may be a mistake to overlook them.

Over the last dozen years, investors holding the classic US 60/40 portfolio were substantially better off than their diversified peers, yet now is not the time to abandon diversification and diversifying asset classes. We believe it is imprudent to trust that escalation in valuations will continue unabated into the next decade...

As China begins the year of the Ox, many investors are wondering whether another bull run is possible in 2021. Given that last year’s rally was extremely narrow, we believe many parts of the market still offer pent-up recovery potential.

Federal Reserve Chair Jerome Powell heads into what could be his last year atop the central bank determined not to repeat the mistake he made when he was a neophyte monetary policy maker seven years ago.

The 10-year Treasury note’s almost three-week run above the once-elusive 1% yield is suddenly looking precarious.

Calls for fiscal stimulus measures to target infrastructure are growing. But new research shows that infrastructure investments have offered few benefits to investors.

The budget deficit for fiscal year 2020, which ended 9/30/2020, was $3.1 trillion, the highest ever on record in dollar terms, and the highest relative to GDP since World War II. This year the deficit will be even larger.

There is no easy answer for income investors whose expectations and behaviors need to be adjusted accordingly.

In the years since the end of the gold standard, there’s been a significant lack of discipline in government spending. Today, the federal debt is closing in on an astronomical $28 trillion, which is more than 130% of the size of the U.S. economy.

The 2020s are going to be about rifle shots, not the shotgun approach of index funds.

What goes up must come down... but does what goes down have to come up? According to the laws of gravity, no. As for commodity markets, however, history tells us it is true.

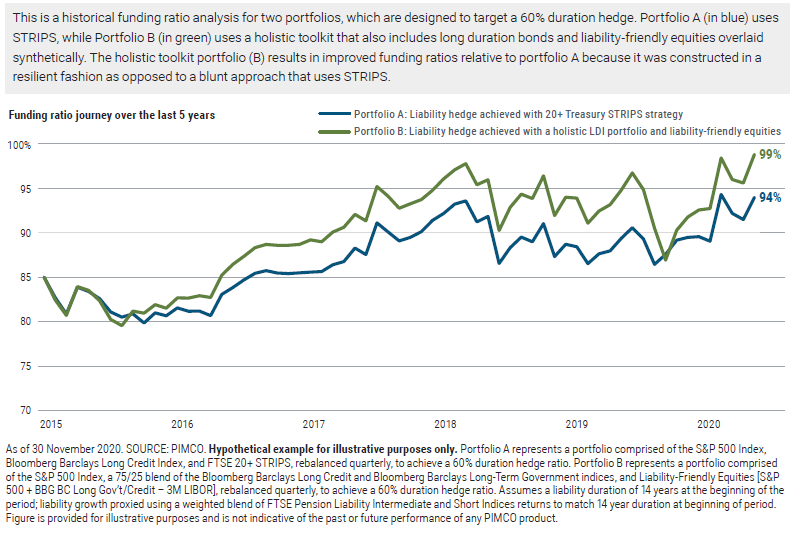

A holistic LDI portfolio may provide a superior liability hedge.

For European banks’ stockholders, 2020 was a year to forget. But bank bondholders enjoyed positive returns and may overcome COVID-19 challenges again in 2021, backed by solid balance sheets and supportive regulatory conditions.