The U.S. stock market has rallied to new highs, but some of the recent “winners” were companies that aren’t profitable and/or had been widely bet-against (“shorted”) by hedge funds. Hope is high that economic growth will accelerate as more people are vaccinated against COVID-19, but so far economic data has been lackluster. Meanwhile, bond investors are expecting inflation despite signs that the economic recovery’s momentum may be stalling. Why does everything seem so disconnected?

U.S. stocks and economy: Frothy sentiment, but solid participation

The pace of COVID-19 vaccinations has been improving around the world as manufacturing and logistical issues are worked out. The road to herd immunity is long, although the total number of administered doses is now outpacing total infections and the trajectory of new cases, hospitalizations, and deaths is improving.

However, this success hasn’t yet been reflected in broader economic data. Fourth-quarter gross domestic product (GDP) growth was weaker than expected, and the U.S. economy added a tepid 49,000 jobs in January—much less than the consensus estimate of 105,000—while December’s payroll shrinkage was revised lower, to -227,000 from -140,000. The unemployment rate ticked down to 6.3%, but for the “wrong” reason: Labor force participation fell, as fewer Americans tried to find jobs.

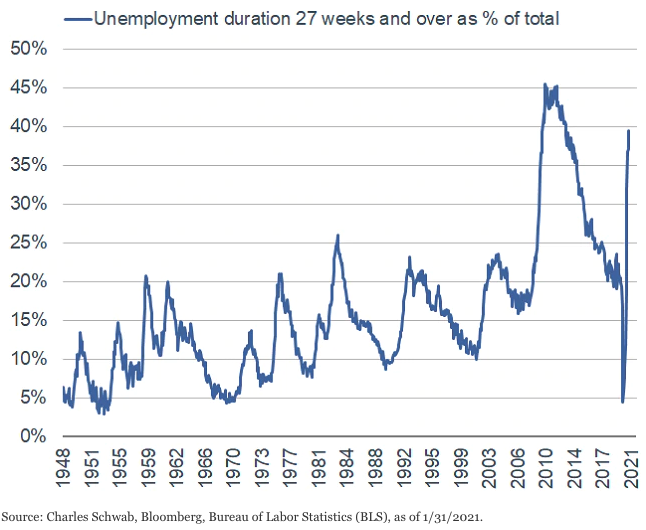

Long-term unemployment has shown no improvement. As seen in the chart below, nearly 40% of unemployed individuals have been without a job for at least 27 weeks. Aside from the three years after the 2007-2009 Great Recession, this is the highest percentage on record. Permanent job losses also ticked up in January, underscoring that scarring effects on the unemployed are becoming widespread.

Chronic long-term unemployment remains an issue

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics (BLS), as of 1/31/2021.

Nevertheless, the U.S. stock market has continued to rally. In one of the more bizarre trading events in recent memory, a tidal wave of retail traders bid up prices in a small subset of the market: unprofitable technology companies, stocks most-shorted by hedge funds, and those most-favored by retail traders. The most prominent of these was GameStop, a brick-and-mortar video-game retailer, but the frenzy also targeted movie-theater chain AMC Entertainment, mobile-device maker BlackBerry, and home goods superstore Bed Bath & Beyond. The hedge-fund community had heavily shorted many of these stocks—that is, borrowing and selling shares at the current price, hoping to buy them back at a lower price to return to the lender. When retail traders began piling into the stocks, rising prices caught the hedge funds in a “short squeeze,” leading to even more buying.

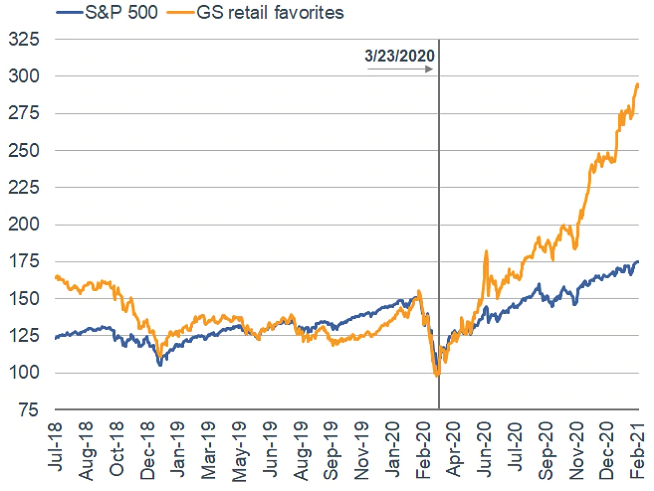

The “most-favored by retail traders” group had underperformed the broader market heading into the 2020 bear market plunge. However, as you can see in the chart below, retail-favored equities have outpaced the S&P 500 markedly, with a substantial portion of outperformance coming in just the past few months.

Retail-favored stocks have outpaced the broader market

Source: Charles Schwab, Bloomberg, as of 2/11/2021. Data indexed to 100 (base value = 3/23/2020). The Goldman Sachs (GS) retail favorites basket consists of U.S. listed equities that are popularly traded on retail brokerage platforms. Past performance is no guarantee of future results.

Frenzied speculation has subsided over the past couple weeks—at least in heavily shorted stocks—but that hasn’t cooled exuberant investor sentiment. This is a risk bred by the market’s recent success. Nearly all behavioral measures of sentiment—most notably associated with the options market—continue to show heightened speculation, highlighting the risk that a lot of good news is already priced into the stock market.

For now, though, strong market breadth has been a tailwind, helping support the broad-based ascent to all-time highs. You can see in the chart below that a high percentage of stocks have been trading above their 200-day moving averages for the better part of two months.

Large- and small-cap breadth still looks strong

Source: Charles Schwab, Bloomberg, as of 2/11/2021.

For now, strong market breadth and strong participation across sectors and factors is a positive offset to frothy sentiment conditions. However, if breadth conditions should weaken without an accompanying decrease in exuberant sentiment, the risk of a pullback would build. As for the broader economic picture, as spring approaches and as the pace of COVID-19 vaccinations improves, the hope is that a lift in social-distancing restrictions (some of which already have started to ease) will spark more activity, along with a resumption in job growth.

Global stocks and economy: Better than expected

International equities have performed well so far in 2021, despite the virus-driven economic slowdown. This may be because economic data continues to surprise on the upside and earnings estimates for the MSCI World Index have continued to climb—positive surprises that may last, as COVID-19 vaccinations are now exceeding cases.

There has been talk of a potential double-dip recession in Europe. Last week’s eurozone GDP figures slipped back below zero in the fourth quarter, to -0.7%, after growing at 12.4% in the third quarter. However, the lockdown-induced slowdown has been less economically damaging than expected during the ramp-up of the vaccine rollout, with most economic data exceeding economists’ expectations.

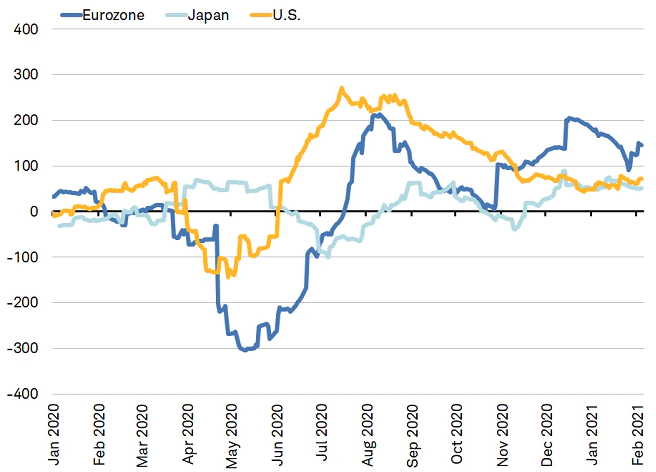

The Citigroup Economic Surprise indexes for the eurozone, Japan and the United States are all currently above zero, indicating that economic data for all three areas is coming in better than economists’ expectations. Despite the finger-pointing in Europe over the slow start to the rollout of vaccinations, the better-than-expected string of economic reports reveals that eurozone economic data is exceeding estimates by a wider margin than in both the United States and Japan, as you can see in the chart below.

Economic data continues to surprise to the upside

Citigroup Economic Surprise Indexes. Source: Charles Schwab, Bloomberg data as of 2/8/2021.

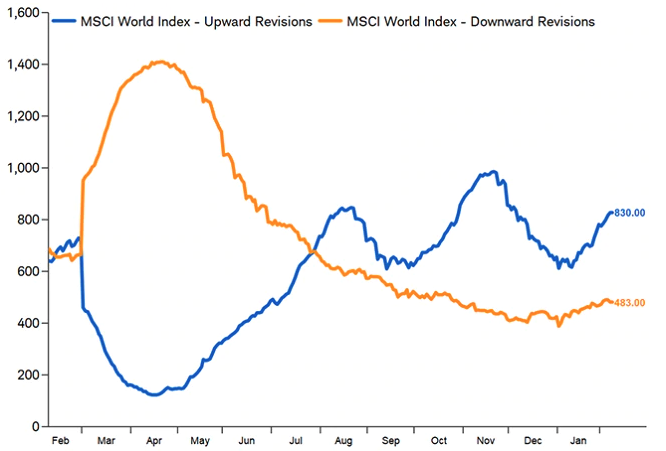

Positive economic surprises are supportive of the outlook for global earnings, and earnings expectations are a key driver of stock markets. More global companies are seeing their earnings per share estimates raised than lowered by analysts, as you can see in the chart below. Over the past 30 days, a total of 830 companies in the MSCI World Index saw estimates revised up, while 483 saw estimates lowered.

Upward revisions to earnings estimates exceeding downward revisions

Number of companies with upward or downward analyst revisions tracked by Factset over the past 30 days.Source: Charles Schwab, Factset data as of 2/8/2021.

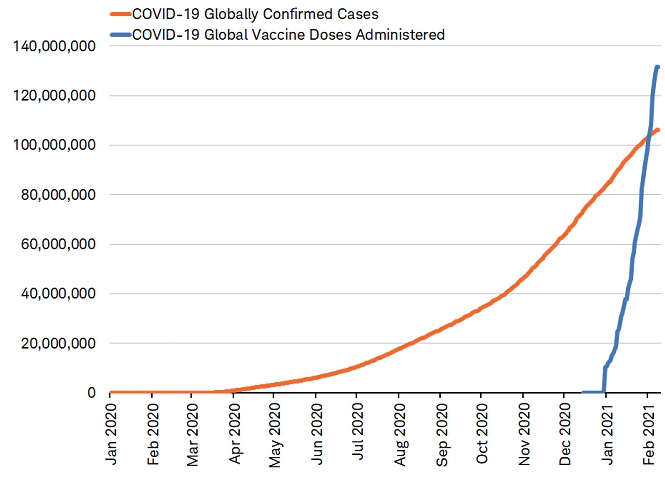

The better-than-expected data and favorable earnings outlook may continue as individuals with at least one vaccination shot began to exceed COVID-19 cases in February, as you can see in the chart below. This may keep lockdowns from tightening and weighing on economic growth.

February crossover as global vaccinations exceeded cases

Source: Charles Schwab, Bloomberg data as of 2/7/2021.

Fixed income: Message from the bond market

The bond market is signaling concern about inflation. After nearly a year of bouncing along in a 0.5%-1% range, 10-year Treasury yields have moved up swiftly in recent weeks.

Ten-year Treasury yields are at the highest level in nearly a year

Source: Bloomberg. Daily data as of 2/6/2021.

The jump in yields is at odds with signs that the economic recovery’s momentum is stalling. In the last few months, the growth rate in job creation has slowed, new orders for manufactured goods have leveled off, and consumer spending has cooled. Moreover, inflation readings are tame, with nearly every major indicator followed by the Federal Reserve still below its 2% target.

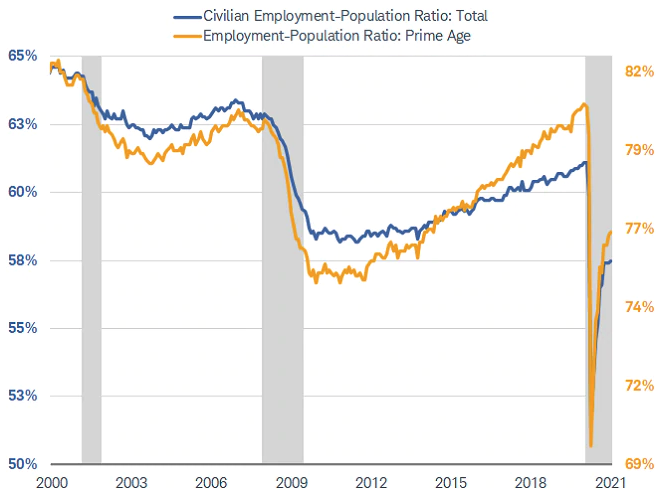

However, if one indicator of slack in the economy stands out, it’s the drop in the ratio of employment to population. After plunging at the onset of the pandemic, it has only managed to rebound to the lows seen during the 2007-2008 global financial crisis. That suggests there is still a lot of excess capacity in the labor market.

The ratio of employment to population remains low

Source: Bureau of Labor and Statistics. Civilian Employment-Population Ratio (USERTOT Index), Employment-Population Ratio - 25-54 Yrs. ("Prime Age" USER54A Index), U.S. Recession Index (USRINDEX Index). Percent, Monthly, Seasonally Adjusted. Data as of 1/31/2021.

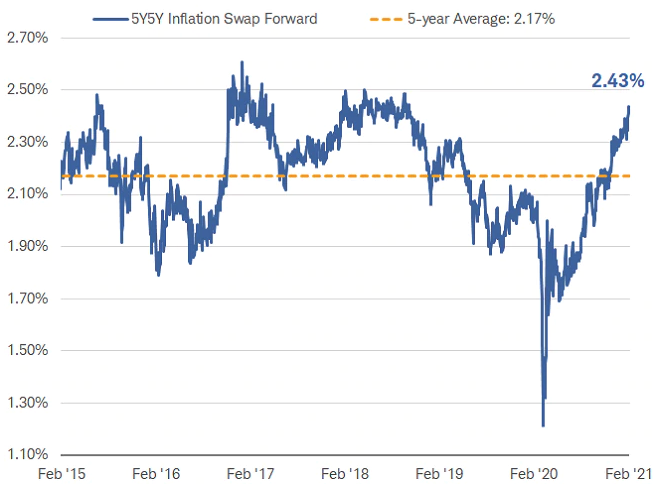

Nonetheless, the bond market is focusing on the prospects for stronger growth owing to the advancing vaccine rollout, along with the potential for at least a $1 trillion fiscal relief package and renewed inflation. The premium investors pay for inflation protection over the next five years has risen to 2.43%, well above the prevailing inflation rate of about 1.5%, and the highest since 2018. The steepening of the yield curve—that is, the difference between short-term and longer-term yields—also suggests elevated inflation expectations, as investors demand more yield to hold long-term bonds.

Investors pay up for inflation protection

Note: This is the 5-year, 5-year USD inflation swap rate. This rate is a common measure, which is used by central banks and dealers, to look at the market's future inflation expectations. The rate is calculated using the following formula: USD: 2*USSWIT10 Curncy - USSWIT5 CurncySource: Bloomberg. USD Inflation Swap Forward 5Y5Y (FWISUS55 Index). Daily data as of 2/5/2020

While we don’t anticipate a significant rise in inflation in the next year or two, the case for higher inflation beyond that is growing stronger. Fiscal relief targeted to lower-income households, combined with declining pressure on wages from globalization and demographic trends, should fuel stronger demand, while a falling dollar will lift import prices. Moreover, the Federal Reserve’s “wait and see” approach to inflation suggests investors are seeing a higher risk of upward pressure on prices longer-term.

We continue to expect bond yields to rise this year as the economic outlook improves. We look for 10-year Treasury yields to move up to 1.6% in 2021 and suggest investors should keep average portfolio duration low.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

All corporate names are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Short selling is an advanced trading strategy involving potentially unlimited risks, and must be done in a margin account. Margin trading increases your level of market risk.

Small cap stocks are subject to greater volatility than those in other asset categories.

Currencies are speculative, very volatile and are not suitable for all investors.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0221-190W)

© Charles Schwab

More Portfolio Building Topics >