Federal Reserve Chairman Jerome Powell and his colleagues appear to be winning over investors with the argument that the current surge in consumer prices won’t last.

With investors anxious to hear the Federal Reserve’s latest take on inflation after last week’s hot reading, certain corners of the market are already simmering down.

Commodities prices have been moving higher this spring amid rising demand and rising inflation expectations globally as economies emerge from the pandemic.

In our last issue we suggested that the "Inflation Genie" was out of the bottle.

To drive home his commitment to easy monetary policy and low interest rates in mid-2020, Federal Reserve Chairman Jerome Powell declared the Fed was not even "thinking about thinking about raising rates."

I spoke with Staley Cates, the vice chairman of Southeastern Asset Management, on the value opportunities he sees in the U.S. and abroad, and why his firm’s process has generated superior returns for its partners/investors.

To get the facts, sometimes you need to look beneath the surface.

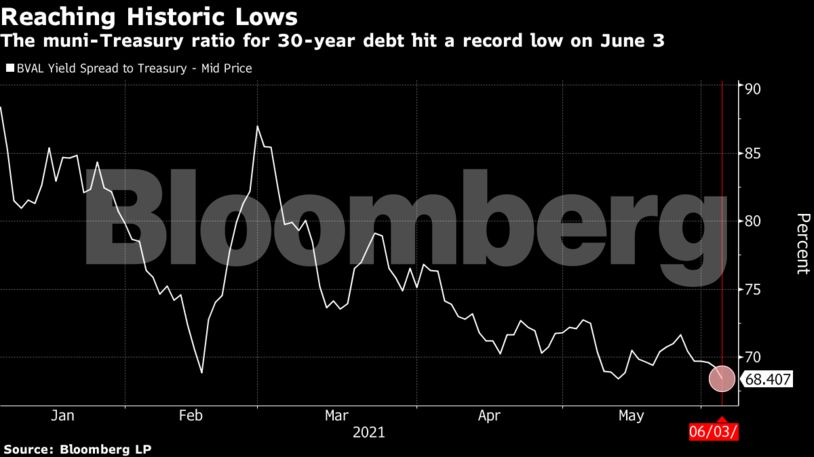

A brief monthly update on what's happening in the municipal bond market.

I’ve been writing about the possibility of higher inflation for months, and now it looks to have finally made landfall. The headline consumer price index (CPI) came in at 5% year-over-year, the highest in over a decade.

With the post-pandemic US economy on the mend, a new threat has emerged: inflation.

In the long term a true inflationary risk comes from growing government borrowing and budget deficits, which will bring higher interest rates and a weaker dollar with them, which will only make inflation worse and will deflate away assets.

The strength of the municipal-bond market shows no sign of fading in the next few months, sustaining the securities’ historic valuations with investors plowing money into funds that buy tax-exempt debt.

This week’s subscriber request series Tuesday covers 10 popular equity REITs.

With only a few brief downturns in an otherwise upward trend in the U.S. equity market since the Global Financial Crisis, declining interest rates have pulled forward the net present value of distant earnings and propelled growth stocks (and the market as a whole) higher.

The economist who helped change the way the Federal Reserve assesses long-run inflation expectations says their current level means the central bank needs to start laying the groundwork for shrinking its massive bond-buying program.

Treasury yields fell again in May and credit spreads approached recent tights as the virus continued to recede, allowing the reopening of the economy to progress. Economic data was noisy this month, largely due to base effects, but confirms the ongoing trend of renewed growth and signs of inflation.

The Fed stated in late April that it expects inflation to be “transitory,” but Jeffrey Gundlach gives that only a 60% chance of being true. If inflation is non-transitory, markets will be “severely stressed,” he said.

Bonds have never been more expensive. Investors face historically low yields, high duration risk, tight spreads and signs of inflation across many sectors of the economy. The most conservative asset class contains much more risk than investors may realize. Financial professionals are asking themselves …

In this webinar, Steve Brown (Assistant CIO and Portfolio Manager – Guggenheim) and Jack Chee (Portfolio Manager and Head of Fixed-Income Strategies – Litman Gregory) will take attendees on a tour through the fixed-income universe, discussing the relative risk/reward across subcategories while exploring alternative areas to help clients de-risk their bond allocations.

Over the past year, a surge of investors drove high-yield bond prices back to pre-pandemic levels.

Although interest rates have risen since the pandemic started, they continue at levels that would be considered historically low.

MicroStrategy Inc. is borrowing $400 million to buy more Bitcoin while also writing down the value of its existing holdings. It’s the first-ever junk bond sale used for financing purchases of the volatile cryptocurrency.

It’s kind of weird to say this, but after more than a decade of Bitcoin’s existence, there’s finally some consensus about what it is.

Most retirement planning software uses data or assumptions that will lead to unrealistically optimistic outcomes, considering our low-interest-rate environment.

In 1974, U.S. President Gerald Ford took office “amidst one of the worst economic crises in U.S. history,” which was characterized by double digit inflation.

According to data provided by The Block, mining revenue on the Ethereum blockchain topped $2.35 billion in May—a new all-time high—compared to $1.45 billion for Bitcoin. Transaction fees alone contributed over $1 billion.

Who isn’t baffled by the continuing run-up in stock prices? Behavioral scientists. They explain that we have a host of biases that make us irrational. Here are the reasons that we have a stock market bubble, presented in two tables.

Transitory is defined as being of brief duration, tending to pass away and not persistent

It’s no secret that investors today are wrestling with their fixed income portfolios. On one hand yields remain historically low. On the other hand, fiscal and monetary forces seem poised to boost inflation and send rates higher. We’ve already witnessed this as we emerge from the pandemic, but how fast and how high will rates go? And more importantly, what will this do to traditional fixed income portfolios?

Victory Capital offers an innovative alternative income strategy that aims to capture attractive equity income while neutralizing the equity risk. Learn more about this approach, how it differs from some of the other alternative income funds, and why it might be appropriate as a long-term strategic allocation.

As more people are getting vaccinated and economic conditions return to normal, Franklin Equity Group’s Jonathan Curtis says the digital transformation themes that accelerated during the COVID-19 crisis are still just getting started.

As special purpose acquisition companies come under growing scrutiny, one basic calculation that was off the mark for some of them is calling into question all other projections: the interest income the companies said they expected to earn on their cash.

In 2021, municipal (“muni”) bonds have been a tough asset class to manage due to overwhelming demand and limited supply in the market.

Inflation is likely to remain high in 2021. The primary source of price pressures is the rebound in commodity prices after their sharp collapse last year.

The eventual tapering of QE will foster a change in investor behaviors. This article focuses on bond yields and a few interest-rate-sensitive equity sectors to provide forward guidance on how fixed income and interest-rate-sensitive assets may perform in a tapering environment.

Since the global financial crisis, a new asset class has emerged that offers attractive yields – single-family rentals (SFRs).

The International Energy Agency (IEA) was founded in 1974 in response to oil embargos the previous year that caused the global price of oil to surge 300% from $3 per barrel to $12 per barrel. From the start, the IEA’s mission has been to help member nations deal with major oil supply disruptions.

With the US economy accelerating and price pressures rising, investors have started wondering when the Federal Reserve will start to wind down, or taper, its current QE asset purchases—a pillar of accommodative monetary policy since the global financial crisis.

Wondering where the dollar’s headed as the U.S. deficit keeps growing? Wall Street’s also trying to figure it out.

A quant pioneer with $112 billion in fixed income assets is defying doom-mongers like Ray Dalio as it places a bullish wager on interest-rate risk.

Central bankers around the world are mulling the future of their massive bond-buying programs in a post-pandemic world, knowing that with big balance sheets come big expectations.

In good news for high-yield bonds, recovery rates on defaults are also improving from the concerningly low levels of recent months, as energy-sector defaults have worked through the system. However, recovery rates are still well below their historical level, which indicates weak bond covenants.

While it’s very early to say the rise in inflation has passed, there are signs that the fastest part of the rebound in inflation might soon be over.

We believe the municipal bond market is on the brink of major changes. The Biden administration has proposed legislation that, if passed, could meaningfully increase both taxable and tax-exempt supply in the municipal bond market. While this potential shift could cause some short-term disruption, we believe it could result in more balanced supply and demand over the medium term.

While some major economies are recovering fast from the pandemic-induced recession, others are languishing, and still others remain in a state of acute crisis.

The week’s selloff was dramatic. By Wednesday, Bitcoin was down more than 40% from its all-time high of $64,000, set in mid-April. The token’s market dominance fell to a three-year low of 40%.

Speculative booms provide both entertainment and outsized profits while they are happening, but they do generally burst painfully,” Inker writes. “Speculative booms provide both entertainment and outsized profits while they are happening, but they do generally burst painfully. This is particularly true in equity markets, where the demand growth is ordinarily met with increased supply from savvy capitalists. Maintaining excess demand in the face of growing supply becomes ever more difficult and eventually proves impossible.

The pandemic forced us all to communicate via Zoom.

In a complete reversal from what was expected roughly a year ago, the outlook for muni issuers is much brighter.

“You can't always get what you wantBut if you try sometimes, well, you might findYou get what you need”“You Can’t Always Get What You Want,” The Rolling Stones (Let It Bleed, 1969)

The Federal Reserve may be fretting over the speculative euphoria in crypto, SPACs and meme stocks, but plenty on Wall Street see bubble risks growing across all the systemically important assets.

A boom in spending has stirred fears of economic overheating, which has coincided with a surge in commodity prices and a lift in traditional inflation metrics.