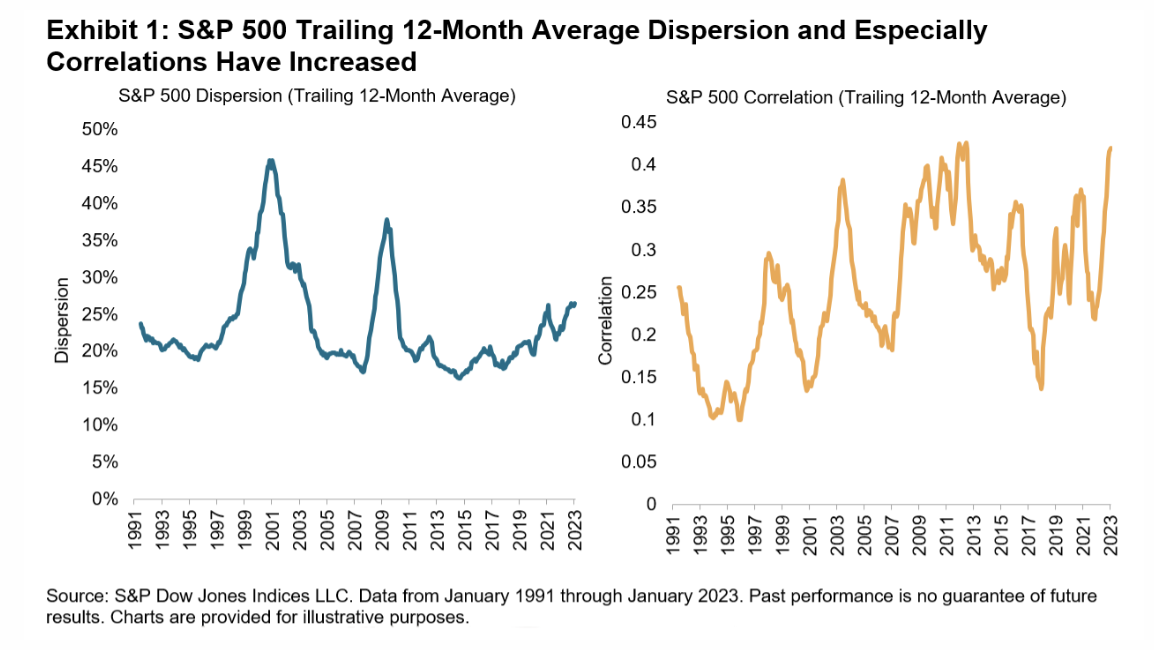

Some commentators have argued that today’s market environment—characterized by rising rates and economic growth concerns—is a ripe environment for stock pickers.

Last week, I dissected developed markets EMEA (DM EMEA) stock performance by sector and found that the consumer discretionary sector was driving upward performance.

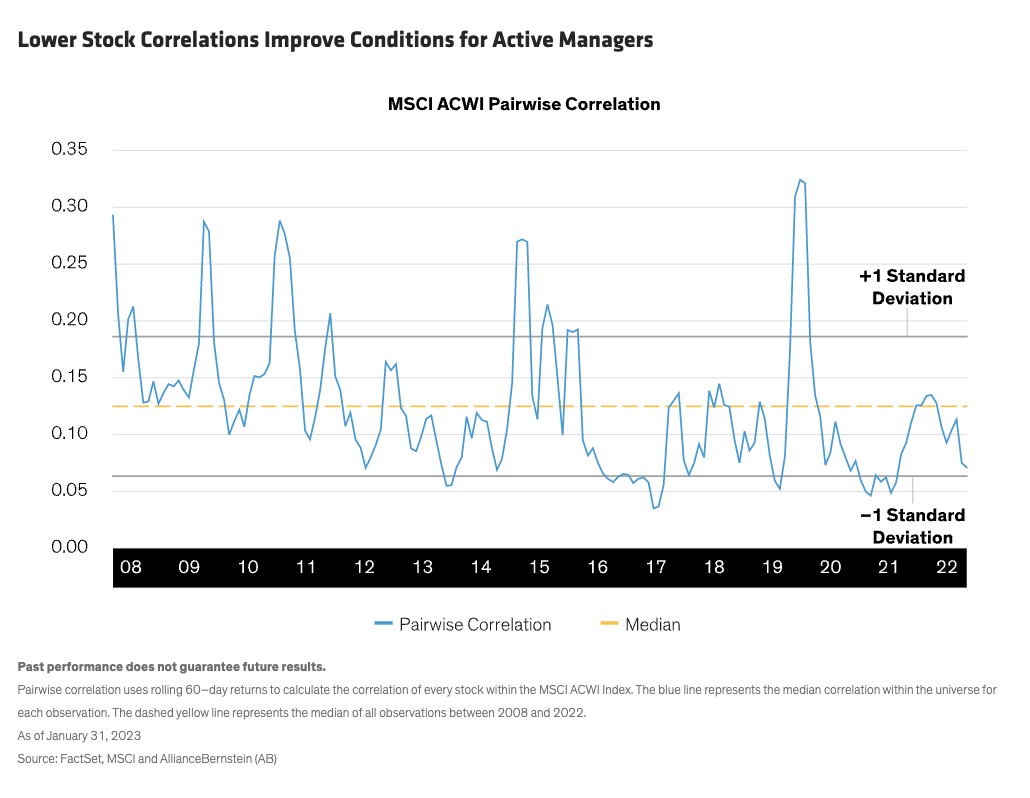

Passive equity investing has retained its dominance and outflows from active portfolios have continued amid the market and macro shocks of the past year.

U.S. inflation may not be moderating as quickly as many were expecting.

Tony Muhlenkamp provides examples to support the maxim by Ron Muhlenkamp that “Just because everybody knows something doesn’t make it true.”

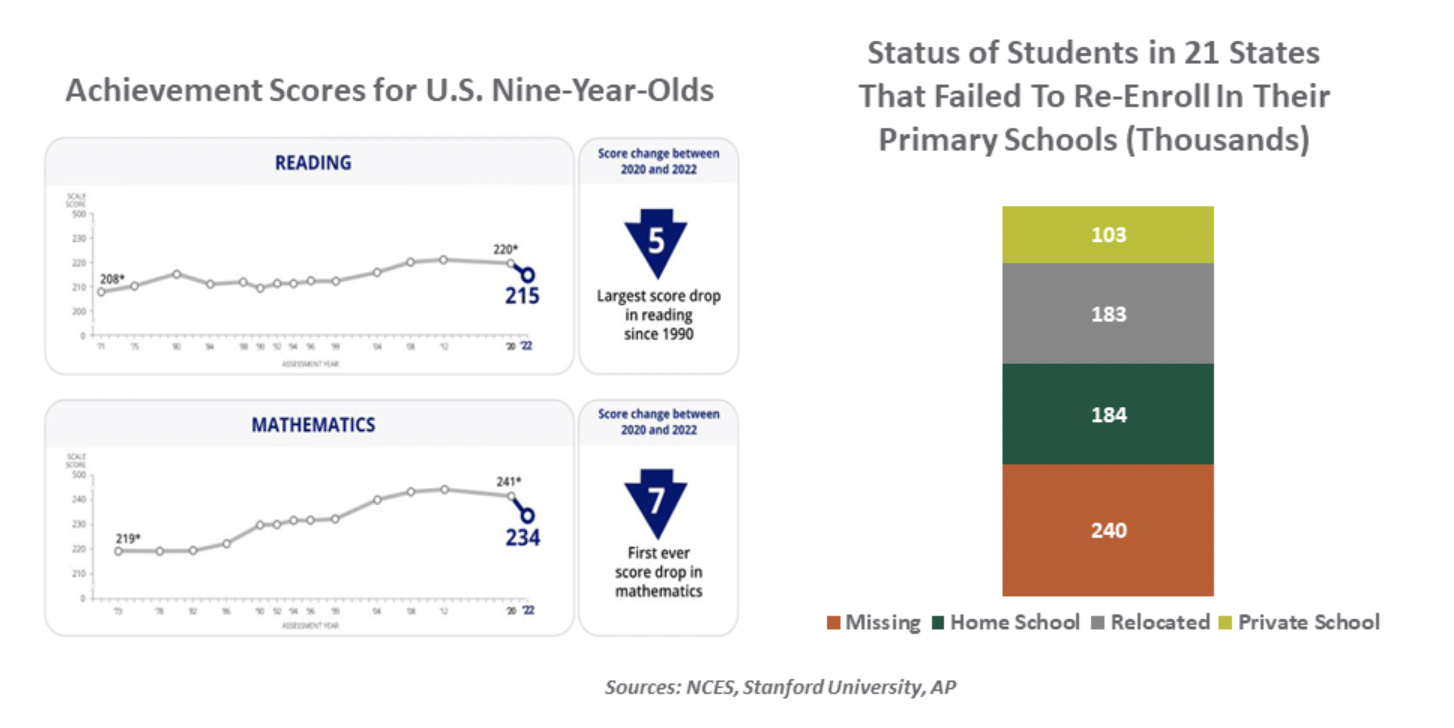

Time out of school is still weighing on student performance.

Advisors who have business owners as clients need to adapt their discovery process and service plans to help these independent and resourceful investors.

Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Contrarian investing requires extra due diligence to identify traits that give investors confidence and conviction to invest in a company when everything and everyone is against it.

Most think so.

Last week I looked at how Canadian stocks underperformed US stocks this year, decomposing North American Performance.

Corn futures traded higher to start the month with weekly USDA data showing an increase in exports week over week.

On October 17, 2022 I posted a video suggesting that: “Don’t Just Buy From Amazon – Buy Amazon.”

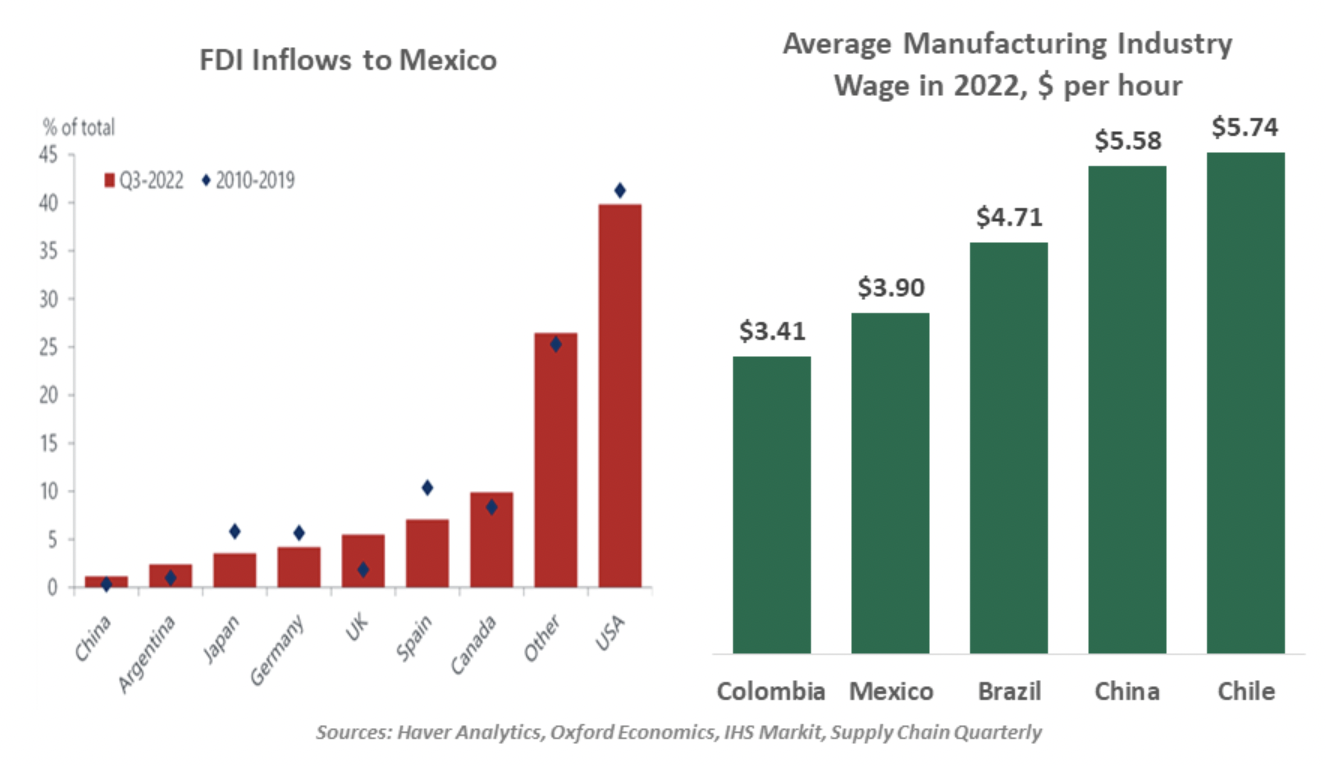

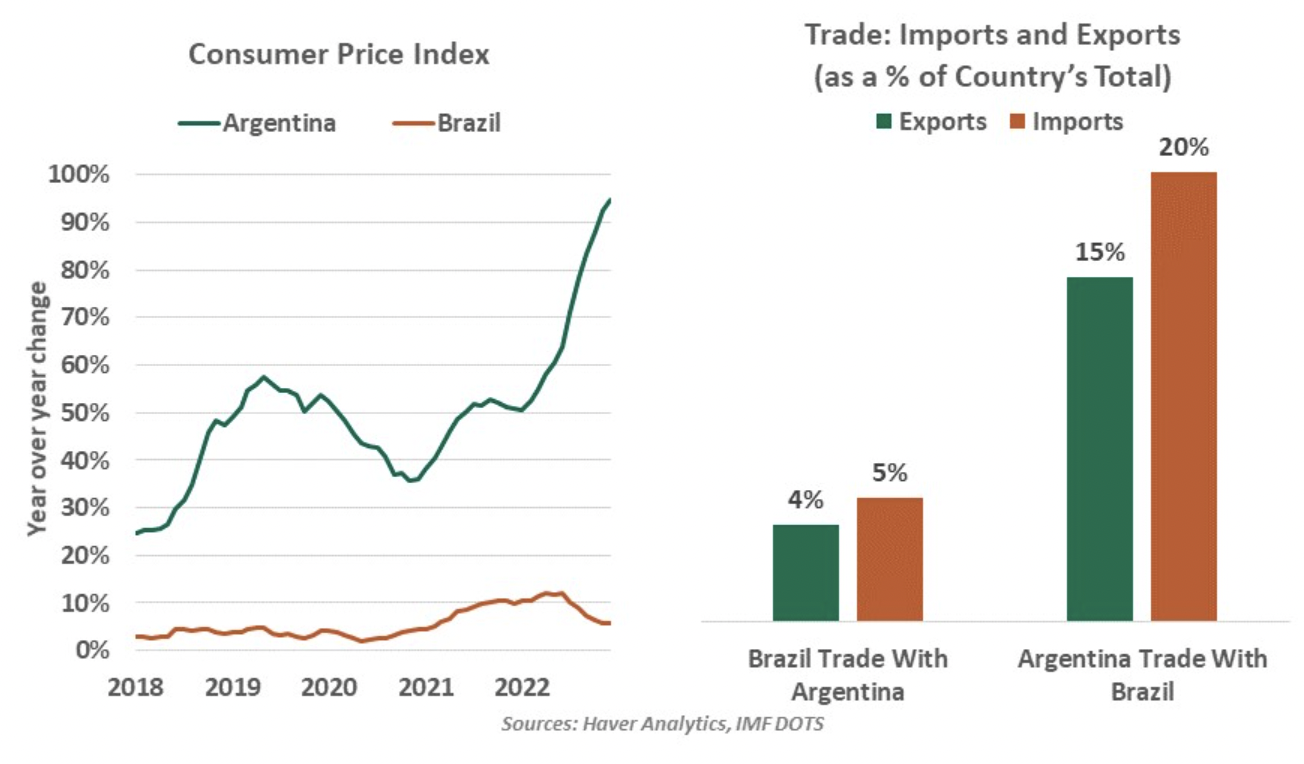

Mexico is downstream of shifting trade winds.

Following the 25 basis-point (bp) increase that the Fed announced on February 1, 2023, Franklin Income Investors Chief Investment Officer Ed Perks answered questions about his outlook on US interest rates as well as fixed income and equity securities for the rest of 2023.

Regal Assets, a somewhat prominent gold and silver dealer in southern California, is in serious trouble based on news released last week.

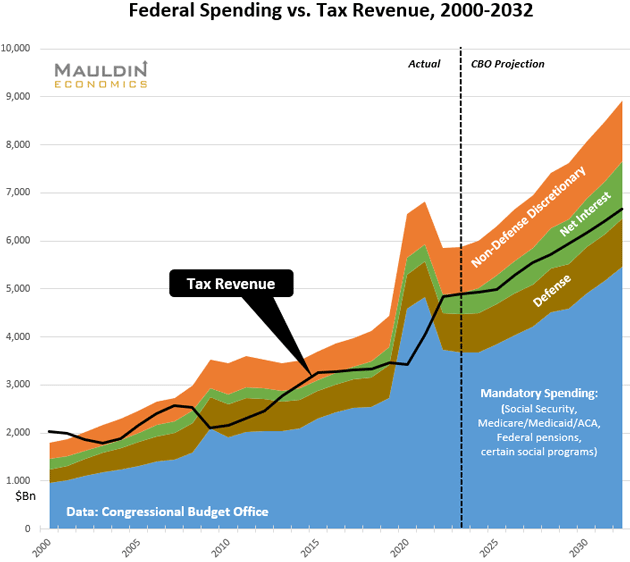

The US economy has reached a crucial juncture point, as several leading economic indicators are on the edge of signaling a recession.

Chief Economist Eugenio J. Alemán discusses current economic conditions.

Bullish investors continue to “Fight the Fed,” hoping that a change to monetary policy will reignite the 12-year-long bull market.

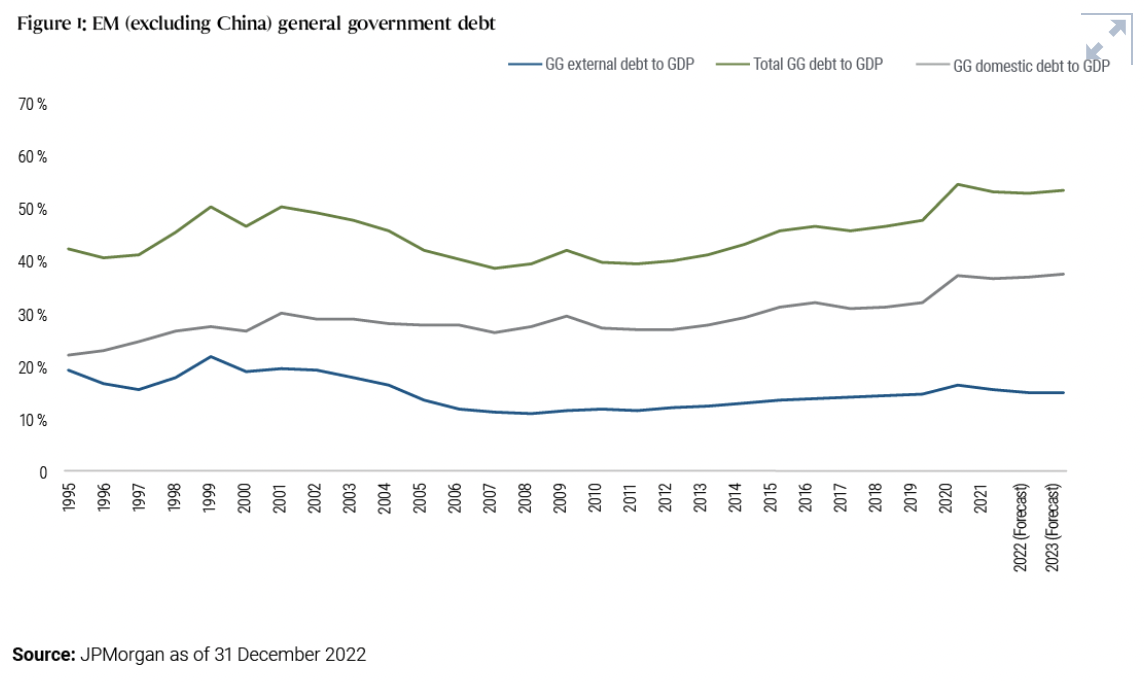

After withstanding a multitude of global challenges last year, emerging markets look poised for improvement as inflation recedes and the path of monetary policy comes into view.

Markets have been volatile, with reports convincing many that the Fed is done hiking rates.

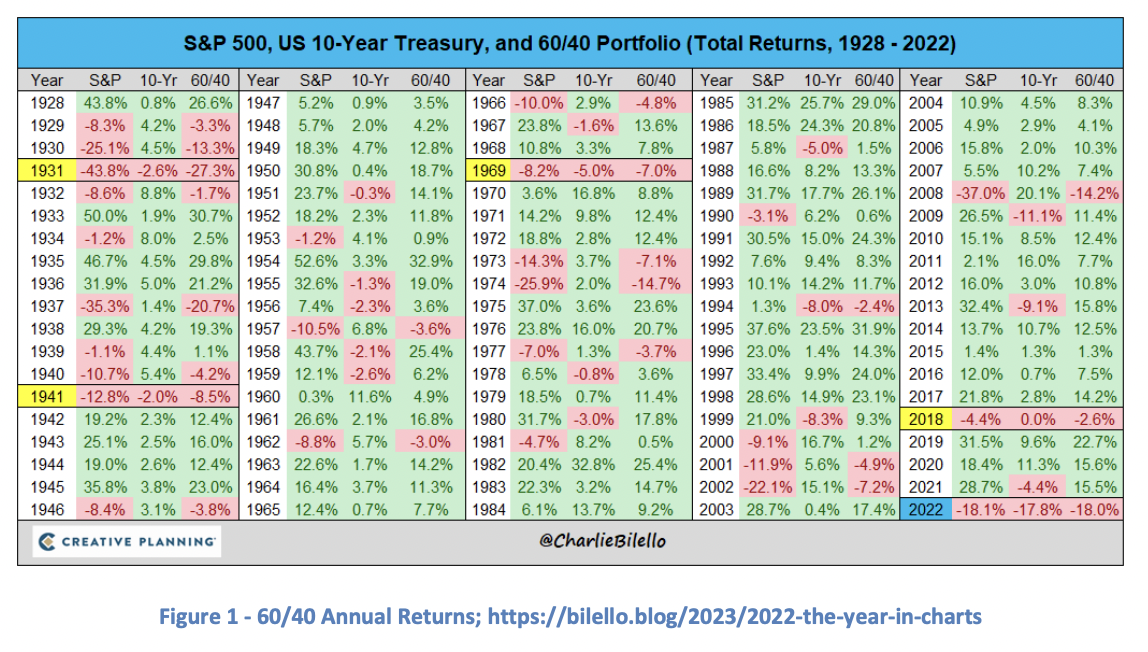

Assumptions can be wise or unwise. They can be unduly optimistic or excessively pessimistic. Slightly different assumptions can produce giant changes in predicted outcomes. Assumptions are necessary but we shouldn’t make them lightly, nor forget we are making them.

This Super Bowl will also be remembered, I believe, as a major turning point in sports betting in the U.S. More than 50 million American adults are expected to bet on the game, the most ever and a remarkable 61% increase from last year.

As inflation fears have receded somewhat—though we’ll see in next week’s US CPI report how much they really have receded—European stocks have had a good start to the year.

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

Despite mounting evidence supporting recession forecasts, the stock market remains at odds with that outlook.

The Loomis Sayles Mortgage & Structured Finance Sector Team shares insights on consumers, real estate markets and more.

As US inflation gradually eases, the claim that today’s inflationary pressures are the result of a temporary supply shock has re-emerged.

Stocks have been interesting, and one question we have had here at the FRED Report is whether the January rally is a sea change in the markets or a flash in the pan.

After a bruising 2022 for equities globally, Value stocks in the U.S. have become attractive in an absolute sense and worthy of inclusion in one’s portfolio.

The aftermarket auto parts industry has been dominated by fast-growing growth stocks O’Reilly automotive and AutoZone.

Despite the current rally in risk assets that includes US equities, we believe caution remains warranted.

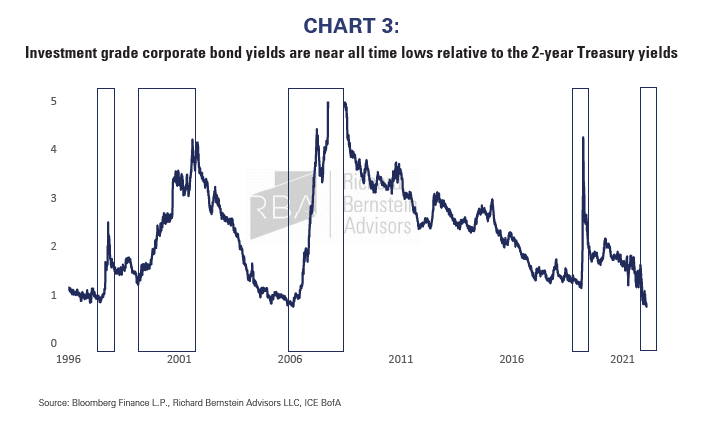

Read Michael Contopoulos' latest report highlighting opportunities outside of Investment Grade corporate bonds and why one does not need to own credit to generate income at the moment.

Stocks lower as investors digest data, Fed commentary.

With the new year in its infancy, it may be too early to think about where to spend Thanksgiving or booking your car’s fall tune-up.

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

US workers are clearly feeling the strain of economic uncertainty, according to Franklin Templeton’s third annual “Voice of the American Worker” study.

Differing economic cycles and limited trade links will make the sur unfeasible.

Brian Smedley, Chief Economist and Head of the Macroeconomic and Investment Research Group, joins Macro Markets to discuss Fed policy, recent inflation, labor, and GDP data, and key takeaways for investors from our 10 Macroeconomic Themes for 2023.

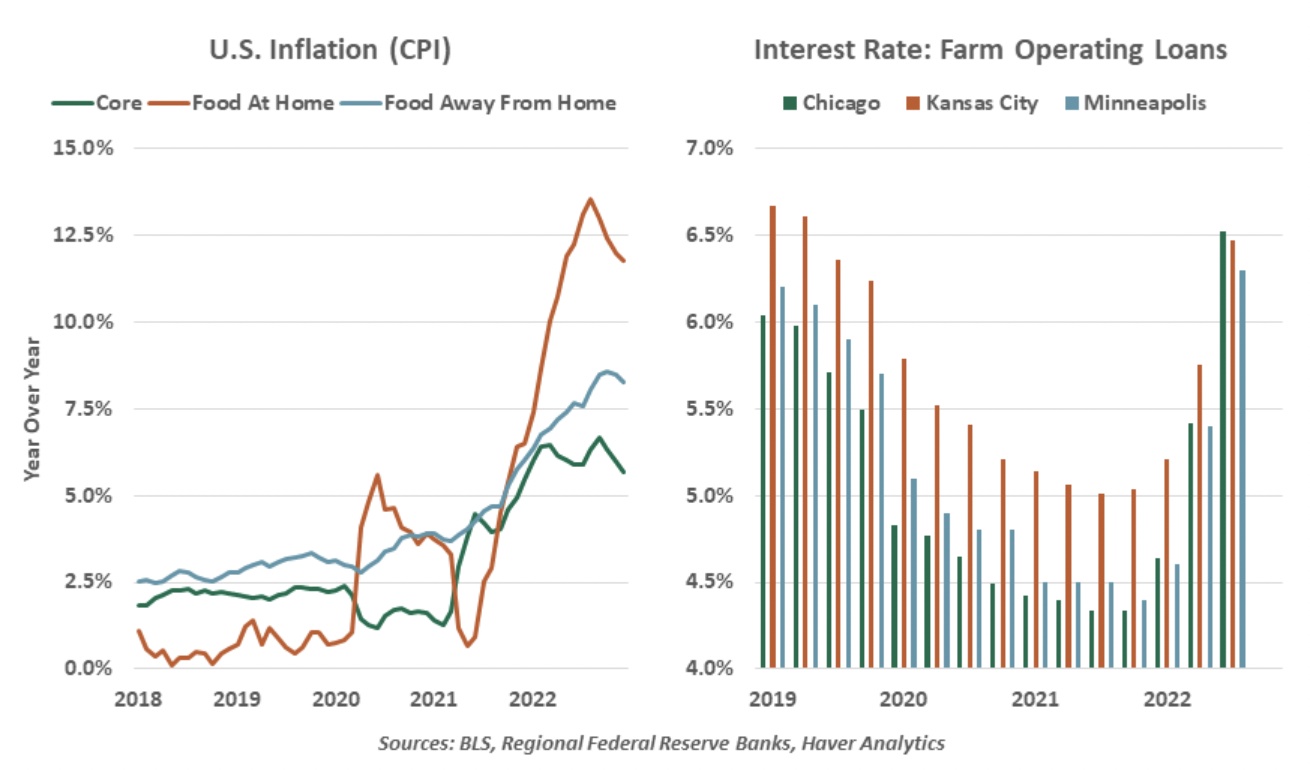

Inflation has turned a corner, but not yet for food.

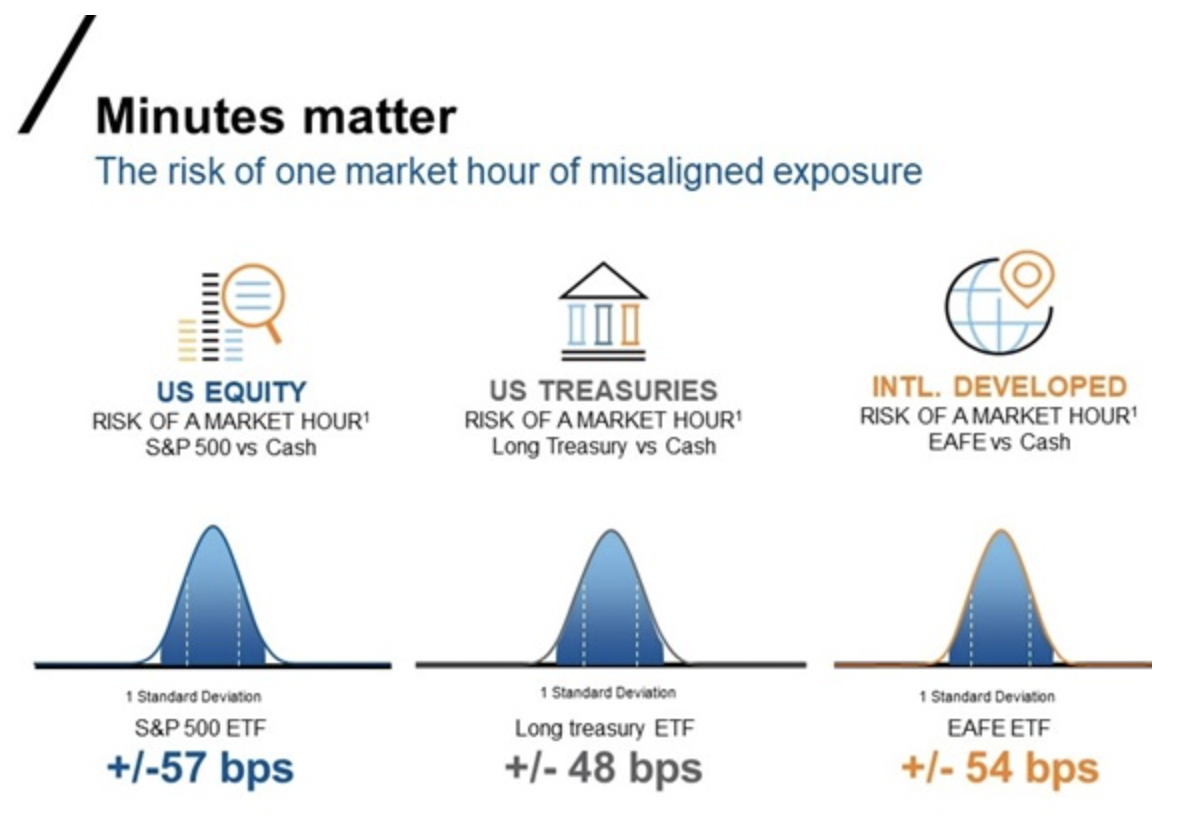

Investors should be aware of potential real-time market exposure risks when implementing large changes to their portfolios.

Monday’s trading saw oil rise as traders digested China’s return in demand against a continued supply strain and slower growth in world economies.

Changes for investors include RMD age increases, higher catch-up contribution limits and a new 529 transferal option.

Valuation metrics across all but the U.S. interest rate dimension remain unambiguously attractive.

With Caixin China PMI numbers today broadly confirming Monday’s official CCP data, the outlook for China and its neighbors remains bright.

At the beginning of the season, not many predicted that the Philadelphia Eagles would be in the Super Bowl this year.

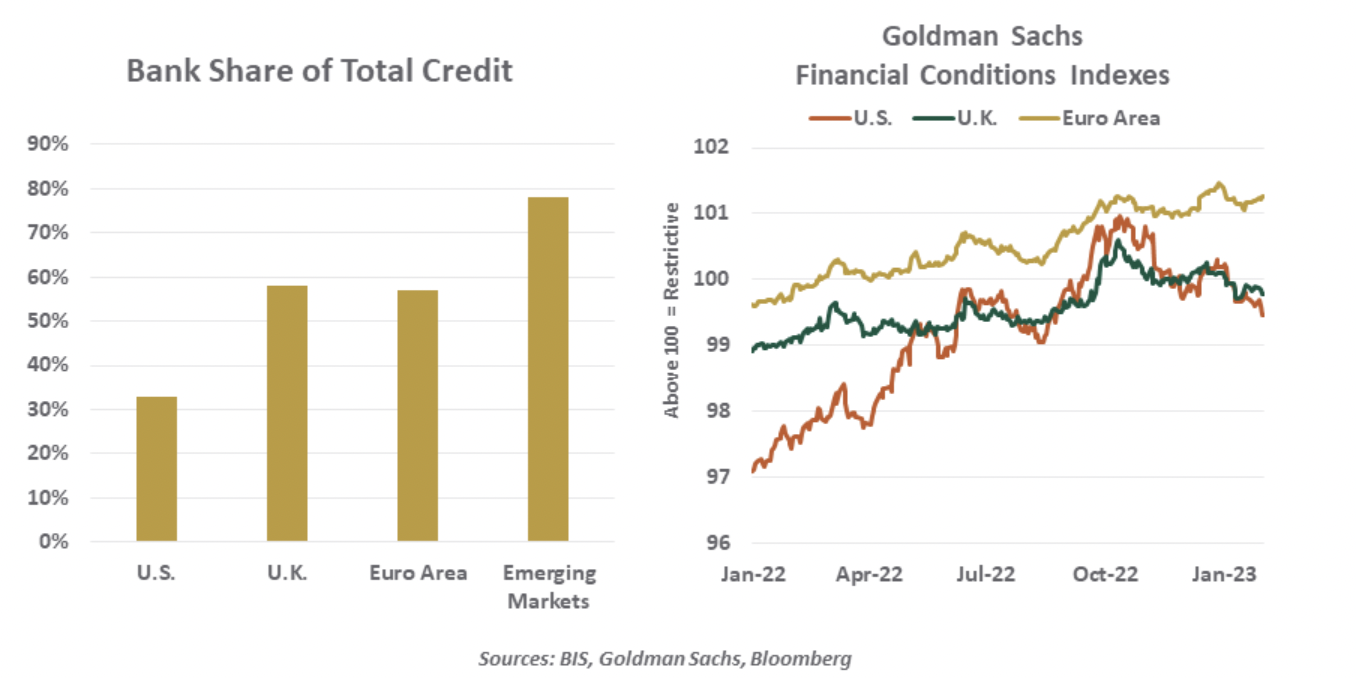

The European Central Bank raised its policy rate, and more hikes are coming.

The most recent NFIB (National Federation Of Independent Business) is sending a strong signal of an economic recession.

Markets are no longer shocked by central bank tightening.

We are now seeing clear signs of a broad-based decline in inflation.