Disinflation is Just Getting Started

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSummary & Key Takeaways

-

We are now seeing clear signs of a broad-based decline in inflation.

-

This is primarily being driver by goods and energy, while food inflation is likely to drive the next leg lower in CPI.

-

Services and rent inflation however remain sticky, which are primarily being driven by strong wage growth.

-

Although the leading indicators of wage growth are rolling over, given the long and variable lags it is not likely wages and thus services inflation will inflect lower to a material degree until the second half of 2023.

-

This will ultimately force the Fed to keep policy conditions tight for at least the next few quarters, perhaps longer.

Inflation has peaked and is rolling over hard

At long last we are seeing definitive signs of a broad-based peak in inflation. Yes, headline CPI peaked nearly six months ago and has since decelerated from 9% pa to just over 6%, but now, it is the stickier measures of inflation where things are looking positive. Namely, core CPI, sticky prices CPI ex-food and energy, trimmed mean PCE and core PCE are all showing signs of clear deceleration to the downside over the past two to three months.

Just as quickly as inflation climbed during 2021 and early 2022, inflation momentum has cooled significantly of late. In particular, headline CPI is now growing at a sub-2% three-month and six-month annualised rate, while core CPI and core PCE are hovering around the 3% level. Perhaps more important however are the recent developments in Powell’s primary inflation measure in services CPI ex-shelter, which has decelerated markedly of late to a 0.9% three-month annualised rate of growth. The trend in inflation is now definitively downward.

Through seeing data such as this one can perhaps make greater sense of the recent price action in risk-assets, despite the prevalence of headwinds that remain. Regardless, the trend in inflation is clear and this is being priced in accordingly. The markets really want to buy the transitory goldilocks narrative.

In terms of the drivers of the recent disinflation, as we can see below, energy CPI and commodities ex-food and energy CPI can claim responsibility. It is through the latter category the recent disinflation has been particularly noticeable, so much so that durable goods CPI growth is now outright negative, with both durable goods CPI and used vehicles CPI in deflationary territory. In terms of food CPI, we are yet to see a material move lower (it’s coming), while shelter inflation and services-ex shelter continue to inflect positively. Unsurprisingly, goods are rolling over yet services remain sticky.

As we will discuss below, these trends in goods disinflation, energy disinflation and soon-to-be food disinflation appear likely to continue in the months ahead. In other words, we should see most measures of inflation move materially lower in the months ahead, while the outlook for services related inflation is less clear.

The primary driver of inflation is the business cycle

As simple as it may seem, the business cycle is at the center of everything. Just as it can lay claim to the directional moves in most asset prices, inflation almost always follows the movements in the business cycle. While inflation can overshoot or undershoot depending on secular trends such as technology, globalisation and demographics among others, it is the business cycle driving the cyclicality of inflation. Inflation is very cyclical.

If we have a view as to where growth is broadly heading over the next six to 12 months, we can have a view as to where inflation is also heading, broadly speaking. Given the trajectory of the business cycle and that its leading indicators continue to point to a prolonged cyclical downturn (detailed here), we can expect inflation to continue to decelerate lower over the next six to nine months.

Goods disinflation will follow economic growth lower

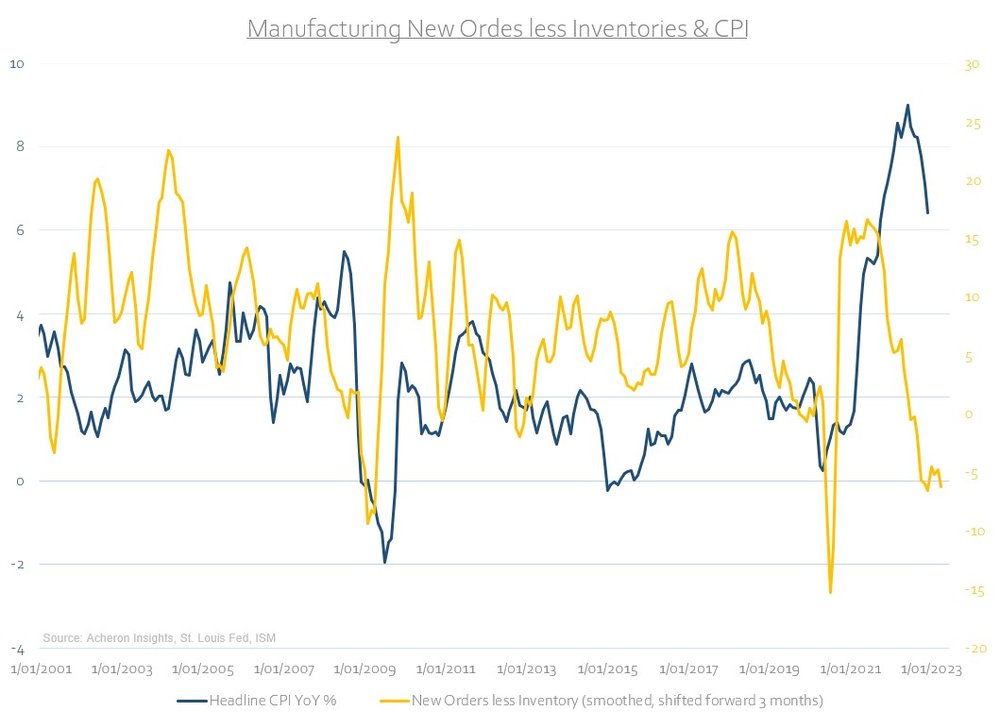

The component of CPI most heavily linked to the business cycle is of course goods inflation, which makes up roughly 22% of the overall CPI basket. We can delve further into this relationship below by examining the trends within the manufacturing sector through the lens of the ISM New Orders less Inventories spread and Prices Paid index. Higher prices tend to lead to lower demand, which in turn leads to higher inventories while sales stagnate, thus forcing companies to lower prices. This is why we see such measures provide solid leads for the direction of CPI. Both indicators lead inflation by around three months and continue to suggest a material decline is imminent.

Echoing this sentiment is the growth rate in retail sales, which itself leads inflation by around nine months and is suggesting a sub-4% CPI reading is on the cards sooner rather than later.

Similarly, industrial commodities are one of the largest input costs for many manufacturing and industrial production related companies worldwide. Industrial commodities are highly sensitive to demand and thus are a very reliable indicator of overall inflation pressures. As we can see below, they are suggesting headline CPI could be as low as 5% within the next few months.

Meanwhile, the effects of the strong dollar over the couple of years are still yet to flow through to inflation measures while import prices too continue to roll over. Lower import prices and a higher dollar should continue to allow the US to export inflation. How long these trends remain disinflationary will likely depend on how swiftly the dollar downtrend continues. But for now, given the long lags associated with a strong dollar, they remain disinflationary.

Supply chain constraints no longer

Using the New York Fed’s Supply Chain Pressure Index as a gauge for overall supply chain constraints, we can see this measure continues to roll over as supply chain pressures continue their descension. Given this index leads headline CPI by around six months, the continued easing of supply chains will remain a tailwind for lower inflation, indicating a 4% headline CPI reading is imminent.

Used vehicles are now outright deflationary

In my most recent deep dive on inflation back in November, I suggested it would be likely we see outright deflation in several areas of the goods related CPI basket, and, this has of course come to fruition most notably in the used cars component of CPI. Indeed, December’s CPI report for used vehicles came in a -8.3% on a year-over-year growth rate basis. This is likely set to continue over the next month or two as the Manheim Used Vehicle Index, which leads used vehicles CPI by around four months has yet to materially inflect higher.

However, the overall impact this will have of the headline CPI reading are likely have largely already played out. After all, used vehicles only constitute 3.6% of the total number. The trend in new vehicle CPI (rough 4% of the overall CPI basket) will likely be of greater importance in the months ahead however. New vehicle CPI tends to closely follow used vehicle inflation in a less volatile manner, and if this correlation continues to hold, then new vehicle CPI should move materially lower in the coming months in line with used car CPI.

Food inflation, the next shoe to drop

What is almost assured however is the imminent disinflation of food CPI. Food CPI (roughly 14% of the overall headline basket) has yet to inflect lower to any meaningful degree, but, based on the leading indicators of food inflation we are almost certainly set to see a material bout of food disinflation over the coming months. Food CPI should become the primary driver of overall CPI disinflation during this period.

Indeed, both the FAO Food Price Index and fertilizer prices have historically provided a solid lead for food CPI by around eight and six months respectively, and both suggest food CPI will reach 2-4% by mid-year.

Energy inflation on the other hand has already fallen significantly in recent months as energy prices have corrected. Though I am certain we are going to see higher oil prices over the coming years, from a cyclical perspective, both gasoline and crude oil are suggesting energy CPI is set to continue to move lower in the coming months as it is yet to fully reflect the movements lower in oil and gasoline. For now, energy prices remain disinflationary.

Shelter inflation remains sticky

While the trend in goods, energy and food related inflation are clearly downward, we are yet to see such inflections lower within the services side of the equation.

The biggest component of services inflation is shelter CPI, which is made up of rent inflation and owners’ equivalent rent (OER). These subcategories contribute roughly 7.4% and 24% to the headline CPI number respectively. The direction of shelter inflation is the most important variable in determining the overall trend in CPI. Shelter inflation is both sticky and slow moving. Fortunately, it can be forecasted to a certain extent by a number of leading indicators.

In terms of owners’ equivalent rent, the largest single component of the CPI basket, house prices are the most important variable. As we know, house prices are rolling over hard and are likely to continue to do so for much of 2023. This will eventually translate into lower OER. However, we must remember the lags from house prices and their impact on OER are long and variable, meaning we may not even see OER inflect lower until the second half of 2023 at the earliest. Once it does, it should be a significant driver of disinflation and may provide the impetus to see overall inflation measures get back toward the Fed’s desired 2% level, though this is a long way off.

In terms of rent inflation, the Zillow Observed Rent Index (ZORI) and the Census Bureau’s Median Asking Rent data series each provide a solid signal into where rent CPI may be heading. And, as we can see below, both have declined materially over the past few months. However, the median asking rent variable displays a significant level of volatility, so whether the direction lead proves true remains to be seen. The ZORI index on the other hand has rolled over hard.

What is perhaps a more reliable leading indicator of rent inflation is wages. Landlords will adjust rents in line with what tenants can afford, and what tenants can afford is primarily a function of wage growth. Fortunately, we are slowly seeing signs of peaking wage growth, however, until wage growth actually cools to a material degree, rent inflation is likely to remain hot.

Regarding the outlook for wage growth itself, despite the unprecedented strength of the US labour market we are seeing at present, the leading indicators of wages continue to suggest a material decline should come to fruition at some point in 2023. I discussed this dynamic recently in detail here, and, as we can see below, two of the more reliable leading indicators of wage growth in the quit rate and ratio of job openings versus unemployed persons are both very much confirming this thesis.

The overall floor in inflation for this cycle will ultimately be determined by the stickiness of wages. While the warning signs of material disinflation and outright deflation are flashing from the goods, food and energy sector, we must remember services inflation makes up nearly 60% of the overall CPI basket. If we want to see inflation reach the 2% area once more, it is wage growth that is going to be the key determinant.

While we ultimately won’t know how low inflation will get until much of 2023 has played out, we can expect a continued decline in headline CPI for the coming months. While the imminent disinflation will likely appease the Fed to the extent they will stop hiking rates, until wage growth subsides, it is not likely we will see an actual easing cycle by Powell and Co. We are getting closer, but we are not there yet.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All