Political risks have always been present in emerging debt markets and we’ve long taken them into consideration within our overall country risk process.

In this article and video, we are going to cover Fidelity National Information Services.

I was watching NBC Nightly News the other night, and they ran a story about how there is no housing inventory because people are trapped in their mortgages.

Sticky inflation looks to compel developed markets (DM) central banks to crank policy rates higher – and keep policy tight for longer. The Federal Reserve paused last week but pointed to more hikes on the way.

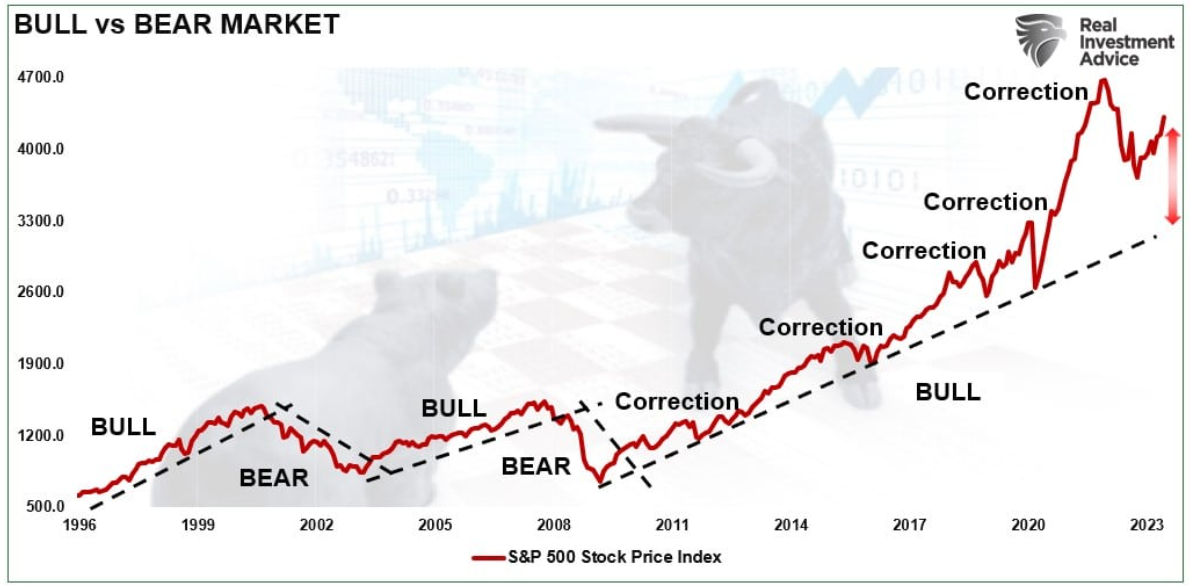

“It’s a ‘New Bull Market’!” Over the past few days, the call of a new bull market has plastered headlines and media commentary.

Sunsetting a core benchmark rate is no small feat.

The period of large upside surprises to global data prints, which dominated the first quarter, seems to be over for now, but it is a major leap to suggest recession is now imminent.

With unanimity, the Federal Open Market Committee held the federal funds rate in its current range, but updated projections suggest this rate-hike cycle is not yet over.

While the Euro Area reported inflation of 6.1% in May, the US was able to post 6% year-over-year as of February. In this framework, a hike, and potentially two more to follow, was to be expected before a pause could occur.

In this article, we examine three important indicators from the past week: the consumer price index, the producer price index, and retail sales. By examining these data points, we gain valuable information about inflation in the U.S. and consumer spending patterns and their response to the ongoing inflation battle.

Although once considered a niche strategy, secondaries have matured and now represent a vital cog in the private equity ecosystem, according to Franklin Templeton Institute’s Tony Davidow.

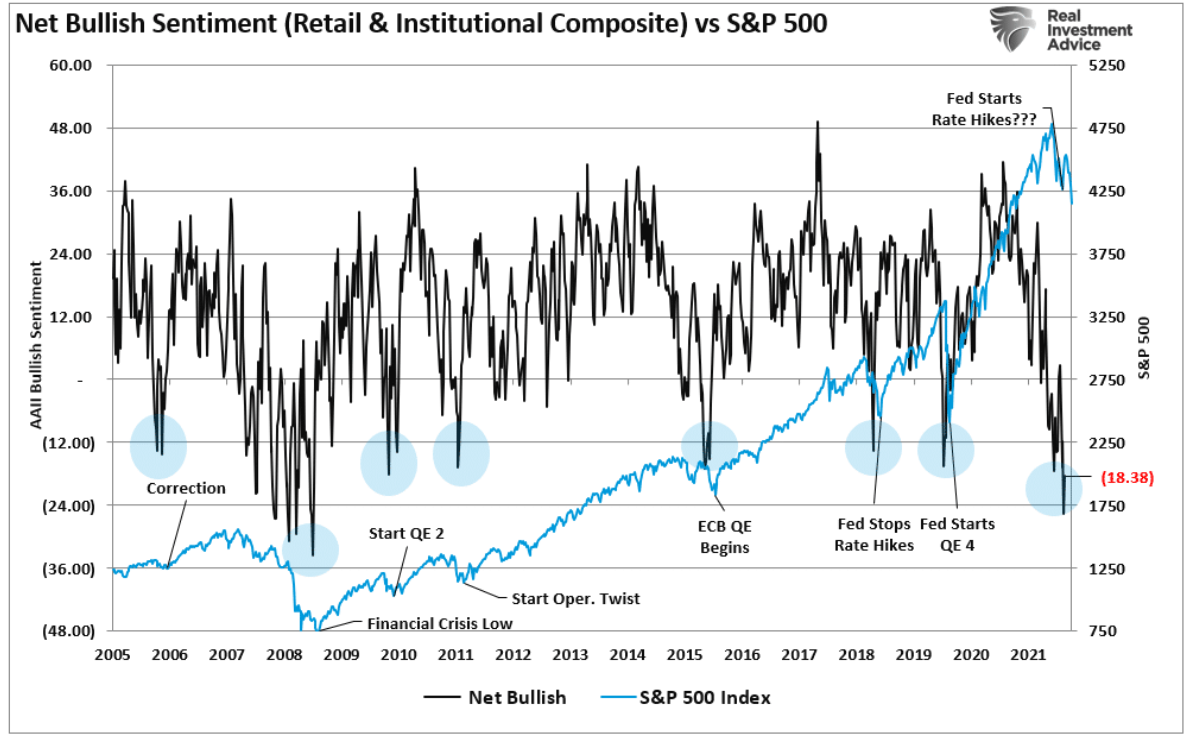

Lately, it’s been easy to see the optimism. As of the Friday close, the S&P 500 is up 15% so far this year (not including dividends) and up 23% (again, without dividends) versus the lowest bear-market close back in October.

Artificial Intelligence (AI) has garnered widespread attention with the public launch of ChatGPT. Learn how these same technologies can be used in investing.

Our long-term outlook for commercial real estate investing argues for a flexible, long-term approach to seize opportunities in debt and equity investments across the real estate landscape.

Bull markets and bear markets can’t be identified in real-time – only in hindsight. More importantly, the return/risk profile of a “bull market” or a “bear market” can change dramatically depending on whether valuations are consistent with the beginning of a market cycle or the end of one.

Quarterly Macro Themes, a quarterly publication from our Macroeconomic and Investment Research Group, spotlights critical and timely areas of research and updates our baseline views on the economy.

At its June meeting, the Fed opted to forgo an increase in its key lending rate for the first time since March 2022 but projected that more rate hikes may be possible by year-end. Our investment strategy analyst shares his thoughts on when the central bank’s rate-hiking journey could finally end.

In this article, we will explore why advisors may not need to worry about illiquidity regarding ESG and other specialty ETFs. We will also offer some tips on how to mitigate any potential issues.

Most of the things we expected to happen during the first half of the year in fact did: Inflation eased, U.S. economic growth slowed, the Federal Reserve appears to be near the end of its rate-hike cycle, and the U.S. government debt ceiling standoff was resolved before a potential default.

The Federal Reserve paused in June but raised its estimates for the policy rate later this year. We expect a July increase but remain skeptical about subsequent hikes.

With the passage of SECURE 2.0, new in-plan emergency savings solutions are on the horizon. What have the past five years of research taught us about the connection between short-term and long-term financial security? And how can 401(k) plans benefit from lessons learned?

For this edition of Bull vs. Bear, James Comtois, and Elle Caruso debate the pros and cons of investing in high-yield fixed-income ETFs.

The surprising resilience of the economy despite the aggressive tightening remains the Fed’s biggest challenge at this point in the cycle. Below we discuss how the Fed’s thinking will likely evolve for the remainder of the year and what it means for the markets.

Bullish sentiment has surged as the “Fear Of Missing Out,” or FOMO, kicked in in recent weeks. It is somewhat interesting to write this blog, given that we discussed the exact opposite roughly one year ago.

The intensity of the chatter around AI has led to some concerns that the space might be in a bubble or that interest in it could wane. However, a look at flows into ETFs that focus specifically on AI suggests that investor engagement remains strong.

The potential for a Fed pause presents an opportunity for investors to consider adding duration back into their portfolios.

Sometimes it feels like the economy and markets are on different tracks.

Chief Economist Eugenio J. Alemán discusses current economic conditions.

There is a whole world going on beyond the 8 largest stocks, which some people can’t see without a microscope or frankly have no inclination to bother stepping into the lab.

The European Central Bank (ECB) hikes rates and signals more tightening ahead.

Naturally, the recent banking crises in the US and Europe raise concerns about EM exposure to financial sector risks too. We’ve found that the EM financial sector overall looks strong and resilient—but that several individual EM countries’ banks could be vulnerable.

A year ago, the US Consumer Price Index was rising at an almost 9% annual rate. The Federal Reserve was trying to change that trend with tighter policy. But it wasn’t just the Fed. All of us—businesses, consumers, everyone—responded to the pain.

Measuring changes in consumer prices is a messy, imprecise undertaking, one that can result in conflicting data, and yet these data are used by both the public and private sectors to guide important policy decisions.

Our director of Customized Portfolio Solutions and overlay portfolio management, Brian Causey, shares his key takeaways from 20 years of working on overlay solutions.

Doug Drabik discusses fixed-income market conditions and offers insight for bond investors.

The sudden influx of capital into the fund could suggest that equal-weight strategies may be back in favor with advisors.

It can feel like inclusivity is a risky policy for a firm in the current climate, but this is not the case at all. Research has shown that companies that are more inclusive tend to perform better than less inclusive firms.

India is making bold moves in ‘new energy’ and decarbonization and our recent trip reinforced our reasons to remain bullish.

Recruiting talent is a basic ingredient for business success. Companies that are more inclusive in their recruiting will discover better-qualified employees, which can bolster competitive advantages and help deliver better outcomes for investors.

Going into the Fed meeting today it seemed like the consensus was toward a skip, pause, or possibly a full-on stop in raising interest rates going forward. Indeed, there are reasons to be optimistic about inflation coming down despite currently sticky “core numbers.”

The meaning of "wealth" goes far beyond having a lot of money. It's more about what money can do for you.

For the first time since beginning the current tightening cycle in March 2022, the Fed opted against raising the federal funds rate at the June 14, 2023, FOMC meeting. The decision officially ends a run of 10 consecutive interest rate hikes by the central bank.

State and local tax revenues sank in April, yet we believe most governments have strong fiscal positions, with ample reserves and budget flexibility to manage the decline.

Using our AI engine, we prompted a description of the Atlanta Fed’s Flexible CPI. What we got was a pretty decent explanation.

Macroeconomic uncertainty has sparked questions over the durability of the traditional 60/40 portfolio—highlighting why investors may want to add alternative investments to the mix.

It’s been a challenging year for many managed futures strategies but they continue to offer long-term potential for portfolios. The benefits of trend-following strategies are numerous and worth consideration for inclusion in any alternative sleeve.

The Federal Reserve will meet this week and announce its decisions on Wednesday.

Interest-rate volatility on shorter-duration assets is running near historical highs, even as rate changes begin to level off.