Central Banks Compelled To Hold Tight

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits- Sticky inflation is leading major central banks to keep policy tight. We prefer emerging market debt as policy loosens and like short-dated bonds for income.

- Developed market short-term bond yields jumped after central banks signaled more rate hikes to come. We see rates staying higher for longer.

- This week’s PMIs will help gauge how much rate hikes have cooled activity. We already see signs of a mild recession in the U.S. and euro area.

Sticky inflation looks to compel developed markets (DM) central banks to crank policy rates higher – and keep policy tight for longer. The Federal Reserve paused last week but pointed to more hikes on the way. The European Central Bank (ECB) raised rates and made clear it wasn’t done. Others hiked after earlier pauses. We prefer emerging market (EM) debt due to looser policy potential, like recent rate cuts in China. We also like income opportunities such as short-dated bonds.

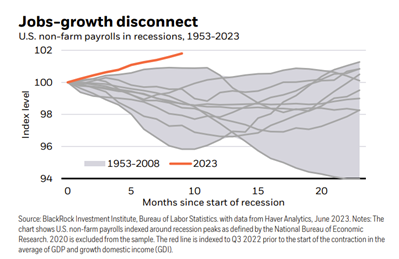

Labor shortages are fueling wage growth, keeping core inflation elevated. That has led the Fed to double down on a “whatever it takes” approach to fighting inflation: Last week it signaled more hikes in the same meeting where it paused. This is happening as central banks in Australia and Canada resumed hikes after attempted pauses – and as the ECB hiked again. We think the Fed and ECB appear to be underappreciating the existing damage from hikes. The Fed revised its growth forecast based on historically low unemployment. The Fed may be relying on a job and growth relationship that has broken, in our view. Labor shortages have made firms reluctant to let workers go, even as demand slows, and growth stagnates. That has made job growth look resilient (orange line in the chart) in recent months compared with weaker jobs data in past recessions (gray lines), even as some data suggest recession may have already arrived.

A broad measure of activity that in the past has been a good indicator suggests as much. The average U.S. gross domestic income and GDP has contracted for two consecutive quarters. We think the Fed’s improved growth forecast ignores the sharp trade-off it faces: crush growth or live with inflation. We think it also exposes an important inconsistency: even higher rates to combat still-high inflation – but with a better growth outlook than previously expected. We don’t think the Fed can expect to bring inflation back down so quickly and maintain such an optimistic view of growth. CPI data last week confirmed core inflation is not cooling enough yet for inflation to return to 2%. We prefer short-term government bonds for income as interest rates stay higher for longer.

This new regime of heightened macro and market volatility requires us to constantly assess what is being priced by markets. That helps uncover regional nuance in how markets are interpreting the macro story across DM. The ECB’s determination to keep hiking has pushed up euro area government bond yields. The market pricing of hikes by the ECB and the Bank of England has become more extreme than our view: Pricing shows rates for both staying higher for much longer than the Fed while inflation stays elevated. Recent wage data in the UK confirmed the worker shortage and supply constraints plaguing other DMs, but we don’t see the inflation problems there or in the euro area as fundamentally much worse than in the U.S. The market pricing in more rate hikes than we think likely is what led us to close our previous underweight on UK gilts in May. We find gilt yields more attractive after having risen near levels reached during 2022’s budget turmoil and prefer short-term maturities. We also like global inflation-linked bonds due to persistently higher inflation.

The EM policy picture stands in sharp contrast with DM. EM central banks started hiking sooner and we think their hiking cycles are closer to an end. That’s why we like EM local currency debt, especially in Brazil and Mexico. Falling inflation makes room for central banks in the emerging world to loosen monetary policy, we think. Case in point: China cut some policy rates just last week as its economic restart from pandemic lockdowns loses steam. Brazil’s central bank governor also hinted last week that the central bank could start cutting rates soon. The market has priced in cuts starting in August through year-end.

Bottom line: We think the tight policy is likely here to stay as sticky inflation compels major central banks to keep policy tight – and likely tighten even further. We see more scope for policy easing in EM – that’s why we prefer EM local currency debt. We also like short-dated bonds for income against this backdrop. Read more in our 2023 midyear outlook on June 28.

Market backdrop

Short-term bond yields jumped in the euro area and the UK on market expectations for further rate hikes after the ECB’s signal and UK data showed surprisingly strong wages. Two-year Treasury yields also rose as the Fed signaled more rate hikes even after a pause. These events confirm the ongoing tightening bias of central banks facing sticky inflation. DM stocks hit new 14-month highs, with gains broadening beyond the mega-cap tech shares that have been the big winners this year.

Macro Take

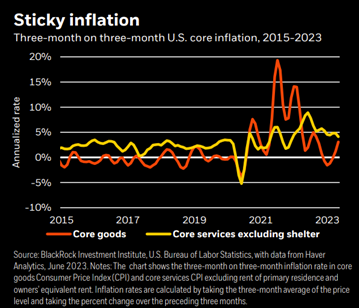

Last week, data showed U.S. core inflation running hot at 5.3% year-on-year in May, as most expected. The surprise? A deeper look shows core goods prices – excluding food and energy prices – have accelerated. See the chart.

We expected goods inflation to keep falling this year, as the surge in U.S. consumer spending towards goods during the pandemic unwound. But it hasn’t been smooth. Core goods prices fell sharply at the end of last year but have rebounded – driven by things like used car prices.

Core services inflation excluding shelter costs is stubbornly high. It reflects wage pressures, especially in contact-intensive service sectors, as firms deal with labor shortages.

Sticky inflation reinforces why the Fed will keep rates higher for longer. We expect inflation to stay high into next year – leaving central banks with no room to cut rates. That’s even if activity weakens as the impact of this year’s rate hikes kicks in.

Investment themes

1 Pricing in the damage

- Recession is foretold as central banks try to bring inflation back down to policy targets. It’s the opposite of past recessions: Rate cuts are not on the way to help support risk assets, in our view.

- That’s why the old playbook of simply “buying the dip” doesn’t apply in this regime of sharper trade-offs and greater macro volatility. The new playbook calls for a continuous reassessment of how much of the economic damage being generated by central banks is in the price.

- In the U.S., it’s now evident in the financial cracks emerging from higher interest rates on top of rate-sensitive sectors. Higher mortgage rates have hurt sales of new homes. We also see other warning signs, such as deteriorating CEO confidence, delayed capital spending plans, and consumers’ depleting savings.

- The ultimate economic damage depends on how far central banks go to get inflation down. The Federal Reserve paused rates in June but signaled further hikes ahead. The European Central Bank hiked again in June. We see the ECB going full steam ahead with rate hikes to get inflation to target – regardless of the damage that entails.

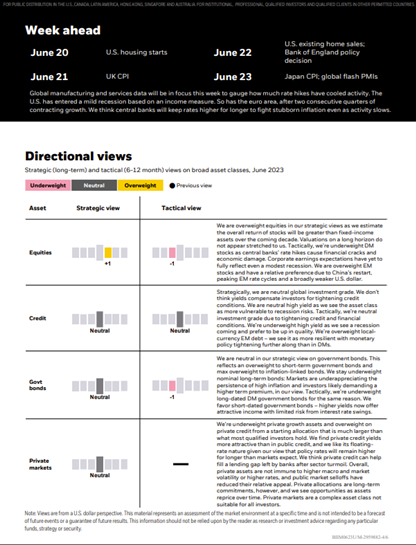

- Investment implication: We’re tactically underweight DM equities. They’re not pricing the recession we see ahead.

2 Rethinking bonds

- Fixed income finally offers “income” after yields surged globally. This has boosted the allure of bonds after investors were starving for yield for years. We take a granular investment approach to capitalize on this, rather than taking broad, aggregate exposures.

- Short-term government bonds look more attractive for income at current yields, and we like their ability to preserve capital. Tighter credit and financial conditions reduce the appeal of credit.

- In the old playbook, long-term government bonds would be part of the package as they historically have shielded portfolios from recession. Not this time, we think. The negative correlation between stock and bond returns has already flipped, meaning they can both go down at the same time. Why? Central banks are unlikely to come to the rescue with rapid rate cuts in recessions they engineered to bring down inflation to policy targets. If anything, policy rates may stay higher for longer than the market is expecting. Investors also will increasingly ask for more compensation to hold long-term government bonds – or term premiums – amid high debt levels, rising supply, and higher inflation.

- Investment implication: We prefer short-term government bonds over long-term government bonds.

3 Living with inflation

- High inflation has sparked cost-of-living crises, putting pressure on central banks to tame inflation with whatever it takes. Yet there has been little debate about the damage to growth and jobs. We think the “politics of inflation” narrative is on the cusp of changing. The Fed’s rapid rate hikes will stop without inflation being back on track to return fully to 2% targets, in our view. We think we are going to be living with inflation. We do see inflation cooling as spending patterns normalize and energy prices relent – but we see it persisting above policy targets in coming years.

- Beyond Covid-related supply disruptions, we see three long-term constraints keeping the new regime in place and inflation above pre-pandemic levels: aging populations, geopolitical fragmentation, and the transition to a lower carbon world.

- Investment implication: We’re overweight inflation-linked bonds on a tactical and strategic horizon.

BlackRock Investment Institute

The BlackRock Investment Institute (BII) leverages the firm’s expertise and generates proprietary research to provide insights on macroeconomics, sustainable investing, geopolitics, and portfolio construction to help Blackrock’s portfolio managers and clients navigate financial markets. BII offers strategic and tactical market views, publications, and digital tools that are underpinned by proprietary research.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation, or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This material may contain estimates and forward-looking statements, which may include forecasts and do not represent a guarantee of future performance. This information is not intended to be complete or exhaustive and no representations or warranties, either express or implied, are made regarding the accuracy or completeness of the information contained herein. The opinions expressed are as of June 20, 2023, and are subject to change without notice. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks.

In the U.S. and Canada, this material is intended for public distribution. In the European Economic Area (EEA): This is issued by BlackRock (Netherlands) B.V. and is authorized and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded. In the UK and Non-European Economic Area (EEA) countries: this is Issued by BlackRock Advisors (UK) Limited, which is authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL, Tel: +44 (0)20 7743 3000. Registered in England and Wales No. 00796793. For your protection, calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorized activities conducted by BlackRock. In Italy, for information on investor rights and how to raise complaints please go to https://www.blackrock.com/corporate/compliance/investor-right available in Italian. For qualified investors in Switzerland: This document is marketing material. This document shall be exclusively made available to, and directed at, qualified investors as defined in Article 10 (3) of the CISA of 23 June 2006, as amended, at the exclusion of qualified investors with an opting-out pursuant to Art. 5 (1) of the Swiss Federal Act on Financial Services ("FinSA"). For information on Art. 8 / 9 Financial Services Act (FinSA) and on your client segmentation under Art. 4 FinSA, please see the following website: www.blackrock.com/finsa. For investors in Israel: BlackRock Investment Management (UK) Limited is not licensed under Israel’s Regulation of Investment Advice, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”), nor does it carry insurance thereunder. In South Africa, please be advised that BlackRock Investment Management (UK) Limited is an authorized financial services provider with the South African Financial Services Board, FSP No. 43288. In the DIFC this material can be distributed in and from the Dubai International Financial Centre (DIFC) by BlackRock Advisors (UK) Limited — Dubai Branch which is regulated by the Dubai Financial Services Authority (DFSA). This material is only directed at 'Professional Clients’ and no other person should rely upon the information contained within it. Blackrock Advisors (UK) Limited - Dubai Branch is a DIFC Foreign Recognized Company registered with the DIFC Registrar of Companies (DIFC Registered Number 546), with its office at Unit 06/07, Level 1, Al Fattan Currency House, DIFC, PO Box 506661, Dubai, UAE, and is regulated by the DFSA to engage in the regulated activities of ‘Advising on Financial Products’ and ‘Arranging Deals in Investments’ in or from the DIFC, both of which are limited to units in a collective investment fund (DFSA Reference Number F000738)In the Kingdom of Saudi Arabia, issued in the Kingdom of Saudi Arabia (KSA) by BlackRock Saudi Arabia (BSA), authorized and regulated by the Capital Market Authority (CMA), License No. 18-192-30. Registered under the laws of KSA. Registered office: 29th floor, Olaya Towers – Tower B, 3074 Prince Mohammed bin Abdulaziz St., Olaya District, Riyadh 12213 – 8022, KSA, Tel: +966 11 838 3600. The information contained within is intended strictly for Sophisticated Investors as defined in the CMA Implementing Regulations. Neither the CMA nor any other authority or regulator located in KSA has approved this information. The information contained within does not constitute and should not be construed as an offer of, invitation, or proposal to make an offer for, the recommendation to apply for, or an opinion or guidance on a financial product, service, and/or strategy. Any distribution, by whatever means, of the information within and related material to persons other than those referred to above is strictly prohibited. In the United Arab Emirates only intended for - naturally Qualified Investors as defined by the Securities and Commodities Authority (SCA) Chairman Decision No. 3/R.M. of 2017 concerning Promoting and Introducing Regulations. Neither the DFSA nor any other authority or regulator located in the GCC or MENA region has approved this information. In the State of Kuwait, those who meet the description of a Professional Client as defined under the Kuwait Capital Markets Law and its Executive Bylaws. In the Sultanate of Oman, sophisticated institutions that have experience in investing in local and international securities, are financially solvent, and have knowledge of the risks associated with investing in securities. In Qatar, for distribution with pre-selected institutional investors or high net worth investors. In the Kingdom of Bahrain, to Central Bank of Bahrain (CBB) Category 1 or Category 2 licensed investment firms, CBB licensed banks, or those who would meet the description of an Expert Investor or Accredited Investors as defined in the CBB Rulebook. The information contained in this document does not constitute, and should not be construed as an offer of, invitation, inducement, or proposal to make an offer for, the recommendation to apply for, or an opinion or guidance on a financial product, service, and/or strategy. In Singapore, this is issued by BlackRock (Singapore) Limited (Co. registration no. 200010143N). This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. In Hong Kong, this material is issued by BlackRock Asset Management North Asia Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong. In South Korea, this material is for distribution to Qualified Professional Investors (as defined in the Financial Investment Services and Capital Market Act and its sub-regulations). In Taiwan, independently operated by BlackRock Investment Management (Taiwan) Limited. Address: 28F., No. 100, Songren Rd., Xinyi Dist., Taipei City 110, Taiwan. Tel: (02)23261600. In Japan, this is issued by BlackRock Japan. Co., Ltd. (Financial Instruments Business Operator: The Kanto Regional Financial Bureau. License No375, Association Memberships: Japan Investment Advisers Association, the Investment Trusts Association, Japan, Japan Securities Dealers Association, Type II Financial Instruments Firms Association.) For Professional Investors only (Professional Investor is defined in Financial Instruments and Exchange Act). In Australia, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). The material provides general information only and does not consider your individual objectives, financial situation, needs, or circumstances. In China, this material may not be distributed to individual residents in the People’s Republic of China (“PRC”, for such purposes, excluding Hong Kong, Macau, and Taiwan) or entities registered in the PRC unless such parties have received all the required PRC government approvals to participate in any investment or receive any investment advisory or investment management services. For Other APAC Countries, this material is issued for Institutional Investors only (or professional/sophisticated /qualified investors, as such a term may apply in local jurisdictions). In Latin America, no securities regulator within Latin America has confirmed the accuracy of any information contained herein. The provision of investment management and investment advisory services is a regulated activity in Mexico and thus is subject to strict rules. For more information on the Investment Advisory Services offered by BlackRock Mexico please refer to the Investment Services Guide available at www.blackrock.com/mx

©2023 BlackRock, Inc. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All