About Quarterly Macro Themes

Quarterly Macro Themes, a quarterly publication from our Macroeconomic and Investment Research Group, spotlights critical and timely areas of research and updates our baseline views on the economy. Themes are selected from the broad range of issues we are currently analyzing, and demonstrate the type of market and economic topics we address in developing our outlook on the U.S. and global business

cycle, market forecasts, and policy views. Our Macroeconomic and Investment Research Group’s research is a key input in Guggenheim’s investment process, which typically results in asset allocations that differ from broadly followed benchmarks.

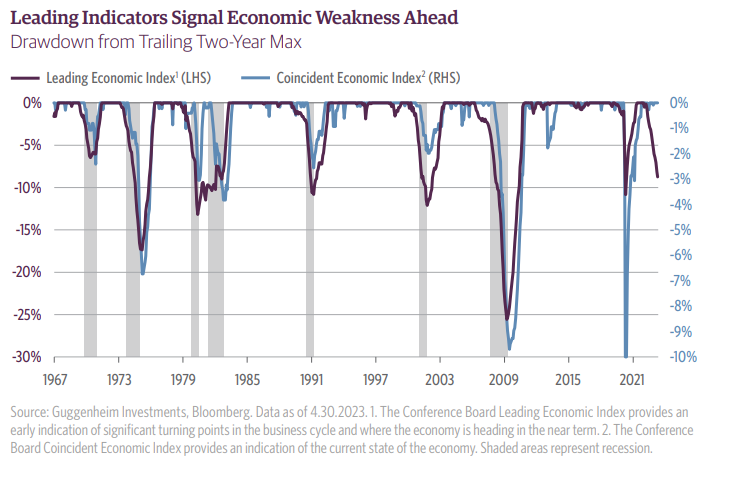

A Fed-Induced Recession Is Still in the Pipeline

2023 has witnessed a dizzying array of consensus macroeconomic views, from no landing to soft landing to financial crisis and back again. The fundamental backdrop we see for the economy is that inflation, while making some progress, continues to run well above target and the labor market remains overheated. As a result, the Federal Reserve (Fed) is deliberately and forcefully trying to weaken the economy, a strategy it believes is required to beat inflation. Making the Fed’s efforts more challenging, tight Fed policy is increasingly compounded

by several other headwinds, including banking system stress and exhaustion of households’ excess savings stockpiles. An underappreciated headwind is also looming as the Treasury builds up its cash balance after the debt ceiling resolution, a process that could drain in excess of $600 billion in liquidity over the next several months, straining the banking system and financial markets.

We continue to believe the Fed will be successful in its quest for a weaker economy, ultimately leading to a recession starting by year end. While recession understandably provokes fear among investors, in this environment it is arguably not the worst outcome from a medium-term perspective. We see signs the recession could be fairly moderate in its severity, and by cooling spending and the labor market we expect inflation will be brought under control. Indeed, while trailing inflation remains stuck around a 5 percent pace, forward-looking metrics for rental inflation and used car prices suggest sub-3 percent inflation by early 2024 is achievable. From an investment standpoint, this outlook means staying cautious on riskier assets now to take advantage of attractive entry points when prices and fundamentals become disconnected as the recession takes hold. Fortunately, shifting toward higher quality assets particularly makes sense at a time of elevated yields and wider spreads than historical norms. And while interest rates could remain rangebound in the near term, we expect more downside toward the end of the year as more progress is made on inflation and we get closer to rate cuts from the Fed.

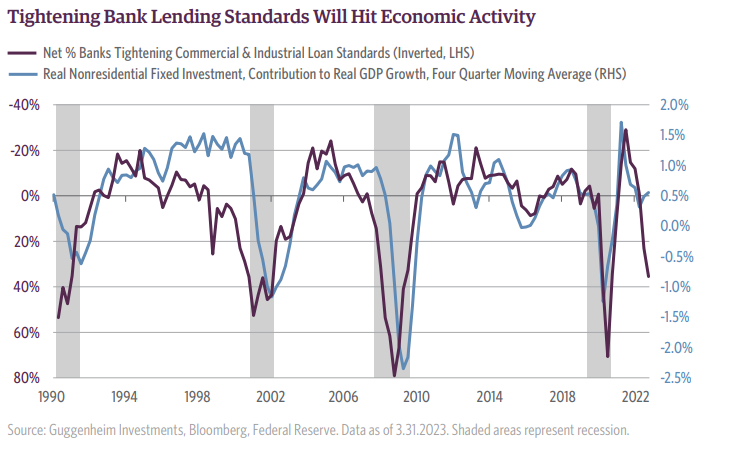

Tightening Bank Lending Standards Point to Potential Funding Gaps

With banking stress continuing to garner market attention, we remain focused on the broader spillovers to the economy. One of the clearest takeaways is that this environment of high uncertainty and risk of deposit flight will cause banks to be more cautious in their lending decisions. The Fed’s Senior Loan Officer Opinion Survey is a useful gauge of these lending conditions. The latest survey, taken

between March 27 and April 7, showed a further tightening in lending standards across all loan types, including commercial and industrial, commercial real estate, residential mortgages, and consumer loans. Notably, the latest data point after the banking turmoil erupted in March looks more like a continuation of a trend in place since 2022 when the Fed began its rate hike campaign, rather than any new

inflection point. Whatever the underlying reason, the consequence will be the same: more restrictive lending conditions mean a pullback in spending by businesses and households. This relationship can be seen clearly by comparing commercial and industrial lending standards and nonresidential investment in the GDP data, which tends to contract when lending standards tighten to the degree they have.

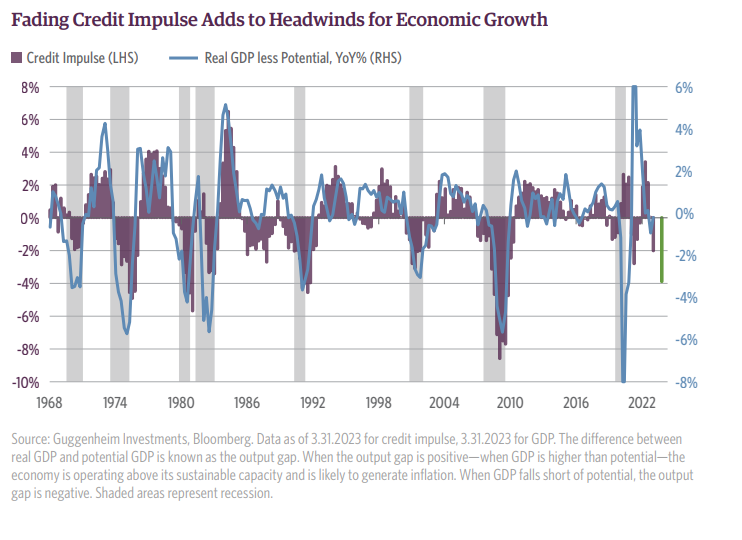

Another issue to consider is a broader view of total credit to households and businesses, including lending from both banks and nonbanks and debt securities. Our work shows that what matters for real economic growth is the change in the growth rate of total credit outstanding (the second derivative, also called the credit impulse). Data are less timely here, but as of the first quarter, we can see that the

total credit impulse had already fallen below zero, meaning that credit growth was decelerating. The underlying data show that the only thing keeping the impulse from going more negative has been bank lending, so based on the tightening in lending standards, we expect bank loan growth will slow and the credit impulse will contract further. Our expectation for where the impulse ends the year is shown in the nearby chart by the green bar, which assumes a relatively modest pullback in lending but still implies a meaningful contraction in real GDP.

A lot of uncertainty remains in terms of how the banking turmoil will evolve. But with households and businesses increasingly reliant on credit after burning through cash buffers accumulated during the pandemic, it seems clear that a credit crunch is on the way, hitting an economy already flashing signs of impending recession. These funding gaps could provide numerable investment opportunities.

Industry Trends and Labor Market Rebalancing Suggest More Moderate Recession Severity

While much attention is paid to whether there will be a recession, its severity is of equal significance. A variety of factors leads us to conclude the next recession will be fairly moderate by historical standards, more in line with 1990 or 2001 than 2008 or 2020.

As we pointed out in 10 Macroeconomic Themes for 2023, published in January, households and corporations are heading into this downturn with relatively solid balance sheets which should limit the extent of the downturn. Another point favoring moderate severity is sectoral trends. A unique feature of this cycle is that two of the most cyclical sectors that are usually the worst hit in recessions—housing

and autos—are out of sync with the broader economic cycle.

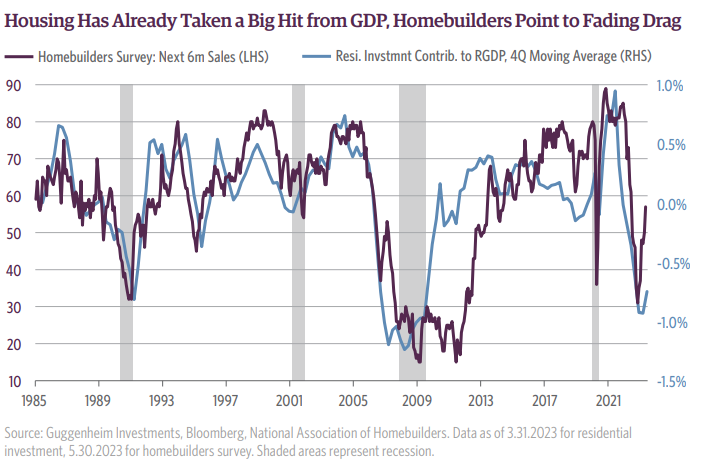

The housing sector, which has already experienced negative growth for the past eight quarters, may not have much farther to fall. This means its drag on the economy may be limited compared to prior downturns. And as the purple line in the nearby chart shows, we are actually seeing some signs of housing activity picking up as homebuyers adjust to a higher rate environment and react to mortgage rates

falling from recent peaks. Given that the construction sector typically cuts among the highest number of jobs in a recession, this revival of demand could limit the extent of layoffs even as the broader economy goes into a downturn.

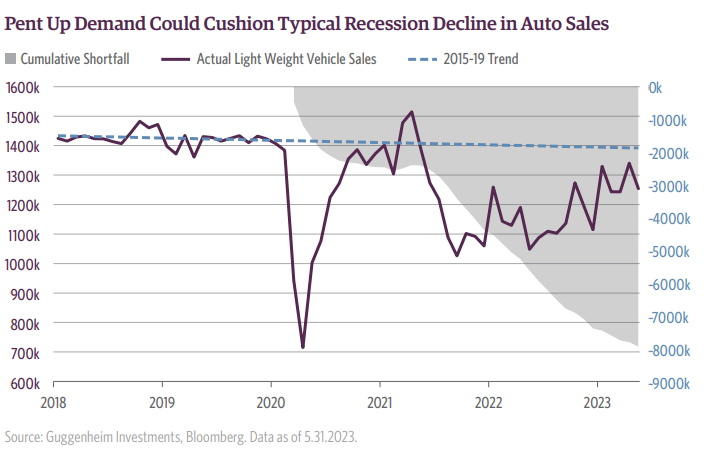

Autos is another sector that usually is a big drag in recessions, but because of supply chain issues and semiconductor shortages, we have already experienced an extended period of weak auto sales. With supply side issues improving, some of the pent-up demand for both auto production and auto sales could also blunt some of the usual recessionary dynamics.

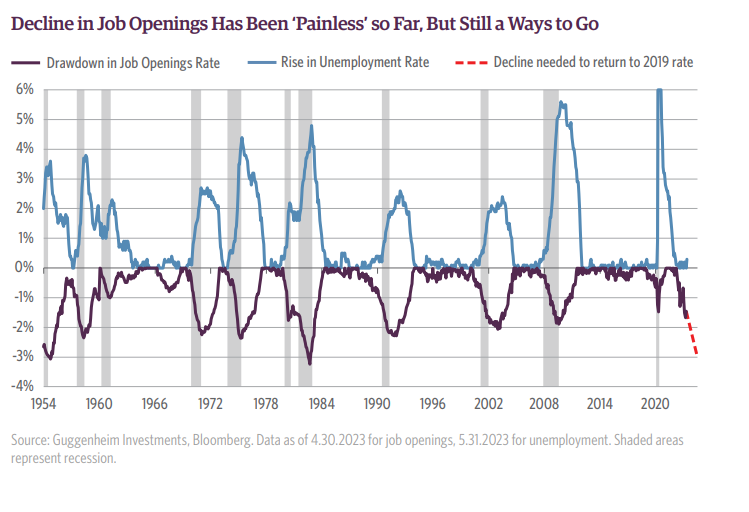

A final factor in our thinking around recession severity is applying what we have observed in the labor market data over the last year. With the labor market overheated, many predicted it would require a sharp recession to restore balance and get inflation under control. While we still believe a recession will be necessary to get inflation fully back to the Fed’s target, the ultimate size of the economic downturn needed to get there should prove to be smaller than many feared a year or so ago. We can see this in the “painless” rebalancing that has taken place so far, with job openings (a signal of labor demand), falling by nearly 2 million since early 2022 without a significant rise in unemployment, which the prior chart shows is without precedent. There are a number of potential explanations, including enhanced labor supply from rising participation and immigration, as well as a reduced need to backfill positions as employment levels have caught up with output and job churn has cooled off. As the green line shows, there is still more work to do be done in getting labor demand to a more sustainable pace, but the track record so far is encouraging.

For investors, these mitigating factors are a reminder that not all recessions are created equal. A moderate recession, together with credit spreads that are already wide of historical averages, means that we are already seeing attractive opportunities in highly rated credit even before the recession has begun.

Equity Analysts, Still Expecting a ‘No Landing’ Outcome, Are in for a Surprise

Despite the Fed’s efforts to soften consumer demand, first quarter corporate earnings results demonstrated resilience in the sectors that continue to put upward pressure on inflation. We see little evidence that analysts expect monetary policy or a more challenging lending environment to negatively impact the sectors where the central bank is aiming to soften demand. It is important to note that

earnings are backwards-looking, and the impact of tightening monetary policy takes time to manifest.

In the first quarter, S&P 500 earnings per share (EPS) declined only 1.7 percent compared to the same period in 2022, outperforming the expected 5 percent decline before reporting began. The majority of companies across all sectors exceeded EPS expectations, with 77 percent of S&P 500 companies surpassing estimates, an improvement from 61 percent in the fourth quarter of 2022. These results indicate that analyst expectations were overly pessimistic and challenge the perception of weakening demand.

While most companies exceeded sales expectations as well, the overall picture is not as robust as earnings. Only 68 percent of companies surpassed sales expectations in the first quarter. For the 9 percent of companies that beat earnings expectations but not sales, the positive surprise on bottom-line results was driven by better-than expected margins, with the largest concentrations of these in energy and materials. This does not necessarily conflict with recession concerns ahead.

On the other hand, the consumer discretionary sector stands out with 82 percent of companies beating both sales and earnings expectations. It indicates stronger-than-anticipated demand and pricing power. Recent remarks from operators in travel, leisure, and accommodation industries support this view, highlighting the resilience despite concerns about inflation, recession, and banking system issues.

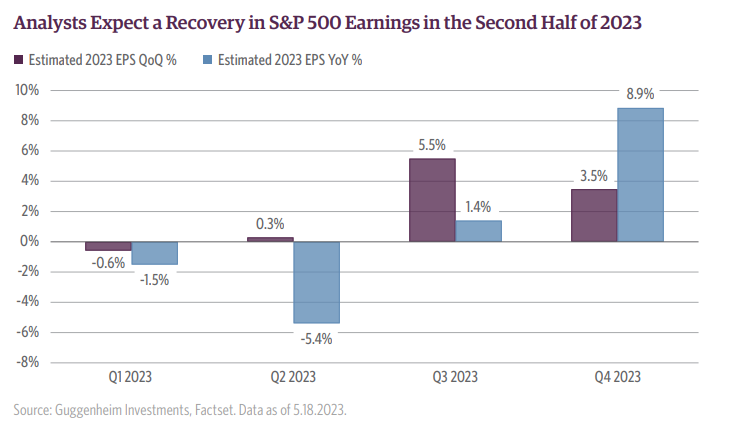

Recent earnings results have led analysts to expect an earnings reacceleration in the second half of 2023, driven by continued strength in consumer discretionary and margin expansion in other sectors. Such a scenario would be atypical during a recession if one were to materialize.

Although annual S&P 500 earnings per share is expected to increase just 1.4 percent this year, the sector weighing most on the outlook is commodities. That is because commodity prices have fallen 26 percent from the 2022 peak, implying that softer earnings expectations ahead largely reflect data behind us. Consumer discretionary, a sector which houses the areas that continue to push inflation above

the Fed’s comfort zone (namely automakers, hotels, restaurants, leisure activity providers, and homebuilders), is expected to show double-digit earnings growth this year. The net result is that the modest slowdown analysts foresee in S&P 500 earnings growth indicates a “no landing” outcome, which we believe is unlikely.

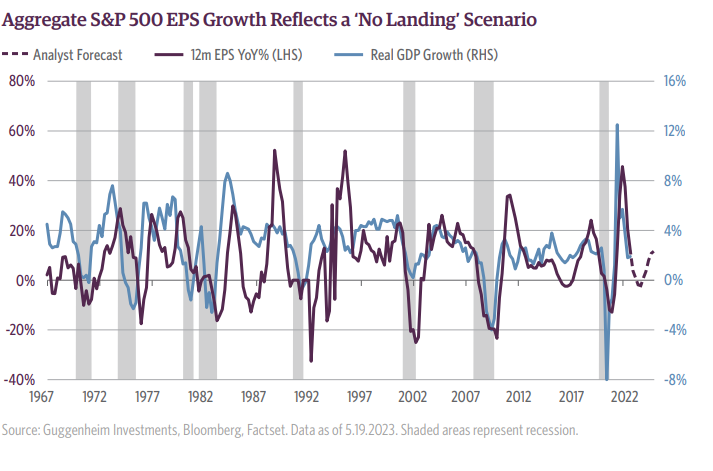

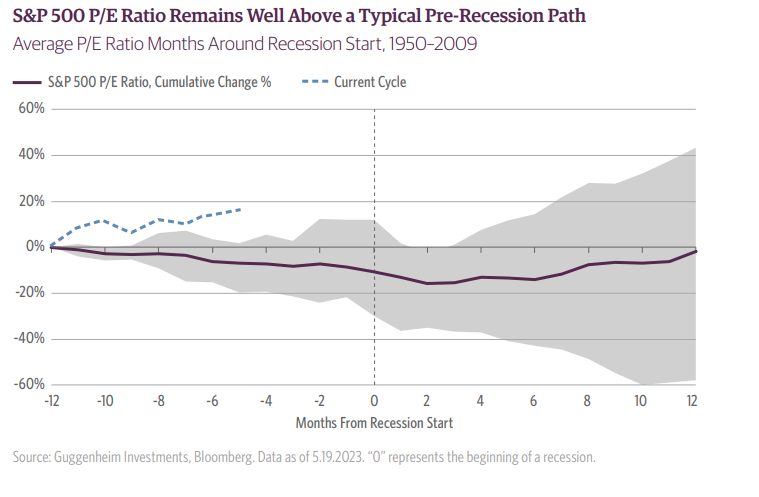

Optimism around the possibility of avoiding a recession is keeping price-to-earnings multiples well above levels that would be historically consistent with a recession within the next year. While we see signs a recession could be moderate, we are skeptical one can be avoided altogether given the Fed’s determination to bring services inflation down. Consequently, an adjustment in both earnings expectations and valuations may lie ahead for the equity market, although the extent and timing of such adjustments remain uncertain. It is worth noting

that our proprietary Bull Bear Market Indicator, an internal model based on economic and market indicators, signals that we are in a regime where bonds have historically outperformed equities. Combining this signal with our perspectives on earnings optimism, valuations, and heightened recession risks, we conclude that investment-grade fixed income is poised to outperform equities as economic data and corporate earnings start to underwhelm expectations.

The Dollar’s Status as the Preeminent Reserve Currency Remains Secure

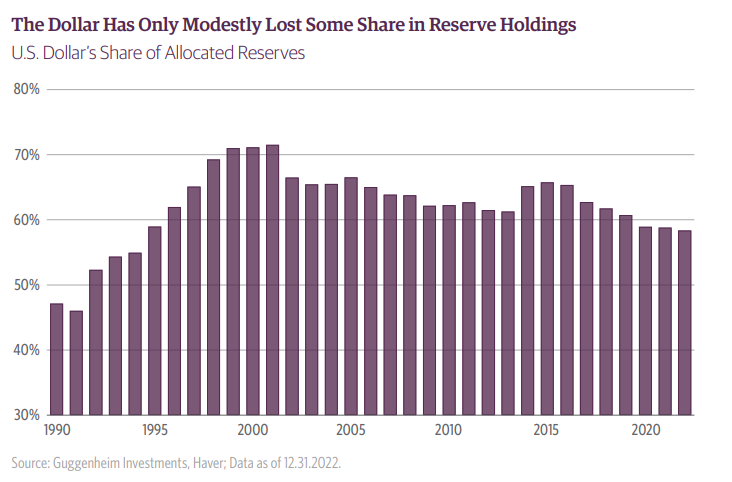

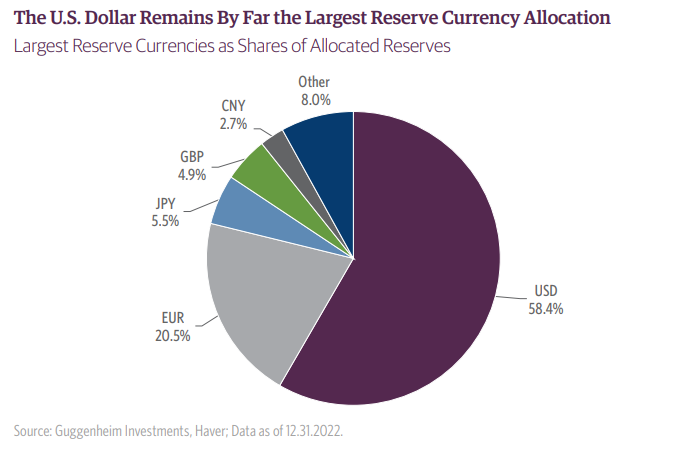

Despite recent discussion of “de-dollarization,” the U.S. dollar remains by far the most favored reserve currency: at 58 percent, more than half of total allocated reserves held by central banks and sovereigns around the world are held in dollars.

While its share is down modestly from its most recent peak of 64 percent in 2014, with the euro, Japanese yen, and Chinese renminbi all gaining 1–3 percent since then, the U.S. dollar remains the dominant reserve currency.

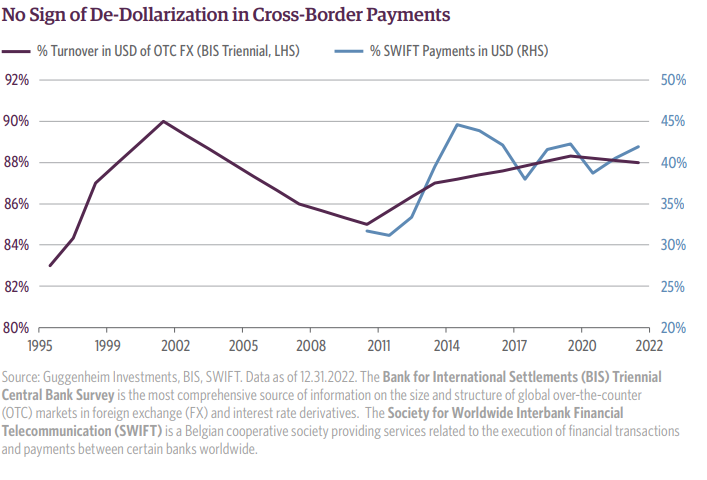

The dollar also remains the most commonly used currency in cross-border payments and transactions. According to the BIS Triennial survey, as of 2022 the dollar was involved in 88 percent of total over-the-counter currency transactions. (The totals add up to 200 percent, since there are always two currencies involved in trades/ transactions.) And as of 2020, the dollar was used in almost 42 percent of SWIFT

payments, about where it has been for the past decade.

The dollar’s status as preeminent reserve currency is supported by the size, diversity, and resilience of the U.S. economy, its deep and liquid capital markets, overall macroeconomic policy credibility, sovereign creditworthiness, and the United States’ political and military might. Of course, it is possible for the dollar to eventually lose its status as the preeminent reserve currency to the euro or Chinese renminbi, given the size of their economies and share of world trade. But those currencies are held back by longstanding structural issues: the eurozone lacks strong centralized fiscal and political authority, and China’s capital accounts are largely closed, with capital controls

in place to prevent destabilizing outflows driven by pent-up demand for overseas assets.

Those impediments, however, are gradually lifting. The E.U. and eurozone have been asserting more control over economic and fiscal affairs. And China has been slowly opening its capital account. Conversely, policy actions by the U.S. government, including sanctions, tariffs, and protracted debt ceiling debates, seem to be hastening a diversification away from dollar reserves and the use of dollars

in cross-border transactions. Even dollar strength can contribute to a move away from the dollar, as foreign authorities sell dollar reserves to support local currencies, and as pressure builds for commodity producers, such as Saudi Arabia, to accept currencies that are not bid up by their safe-haven status. We saw some of these factors weigh on dollar reserves last year. But they recovered somewhat early this

year with dollar weakness.

We expect the renminbi’s share of total allocated reserves to gradually increase over the coming years, and there is likely scope for the euro to gain as well, although to a lesser degree since it already comprises 20.5 percent of total allocated reserves. However, for another currency to surpass the dollar as the preeminent reserve currency, not only would the underlying economy have to be very large, but that

country’s macroeconomic policies would need to be deemed prudent and credible, and its capital markets would need to be large, diverse, and liquid. For those reasons, we do not expect another currency to surpass the dollar.

Important Notices and Disclosures

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author or speaker, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.