The first half of the year has so far been challenging for investors in municipal bonds.

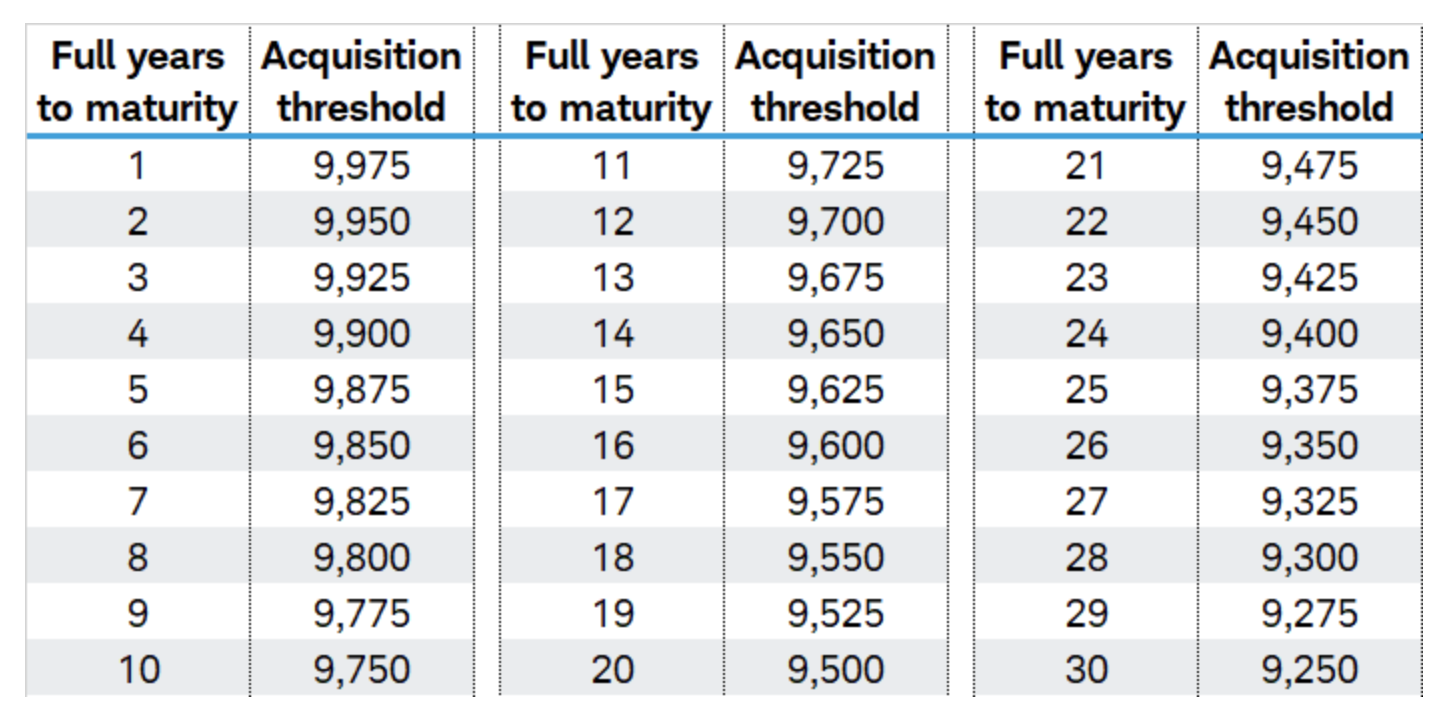

Municipal bonds acquired at too deep a discount could be subject to an additional tax, known as the de minimis tax, which would take a bite out of the after-tax return.

Markets flailed in May, seeking certainty amid conflicting signals.

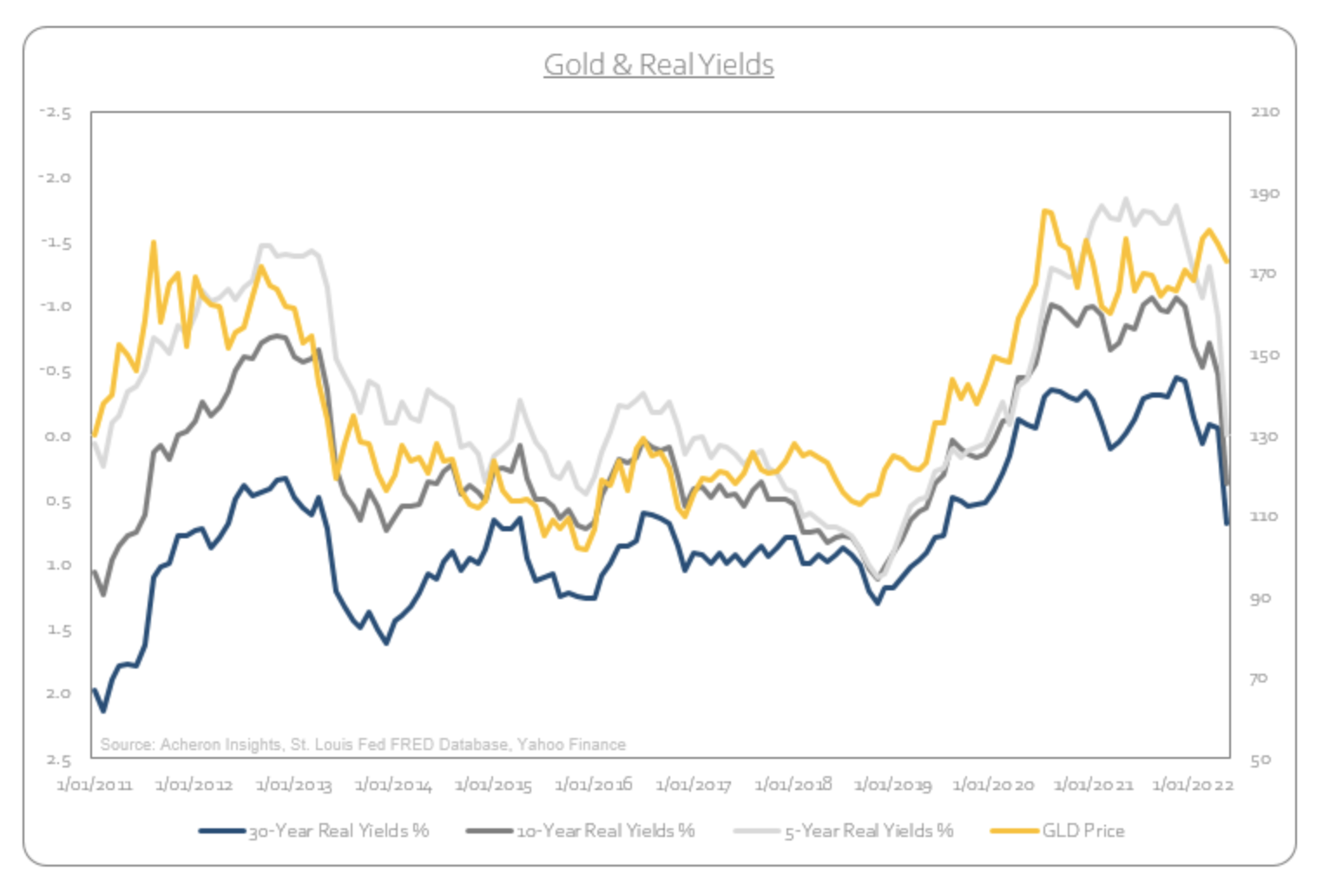

Through rising real yields, a slowing economy and poor seasonality, short-term headwinds remain for gold and precious metals.

Has the global investment environment which we have grown accustomed to over the past few decades fundamentally changed?

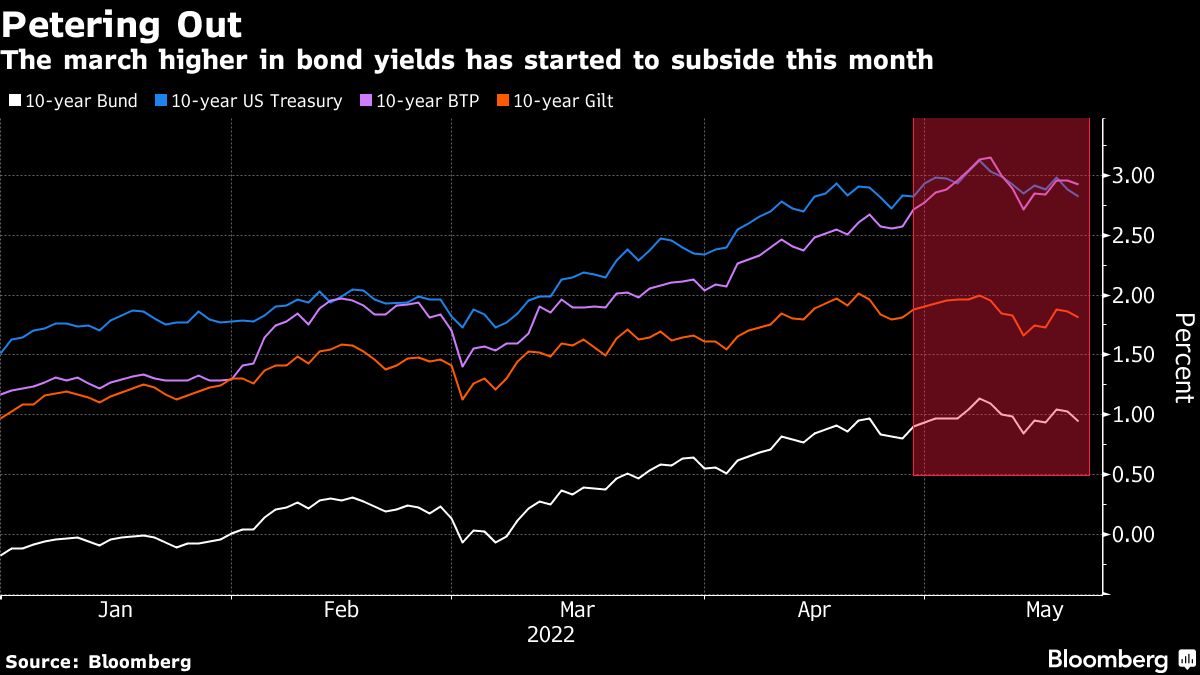

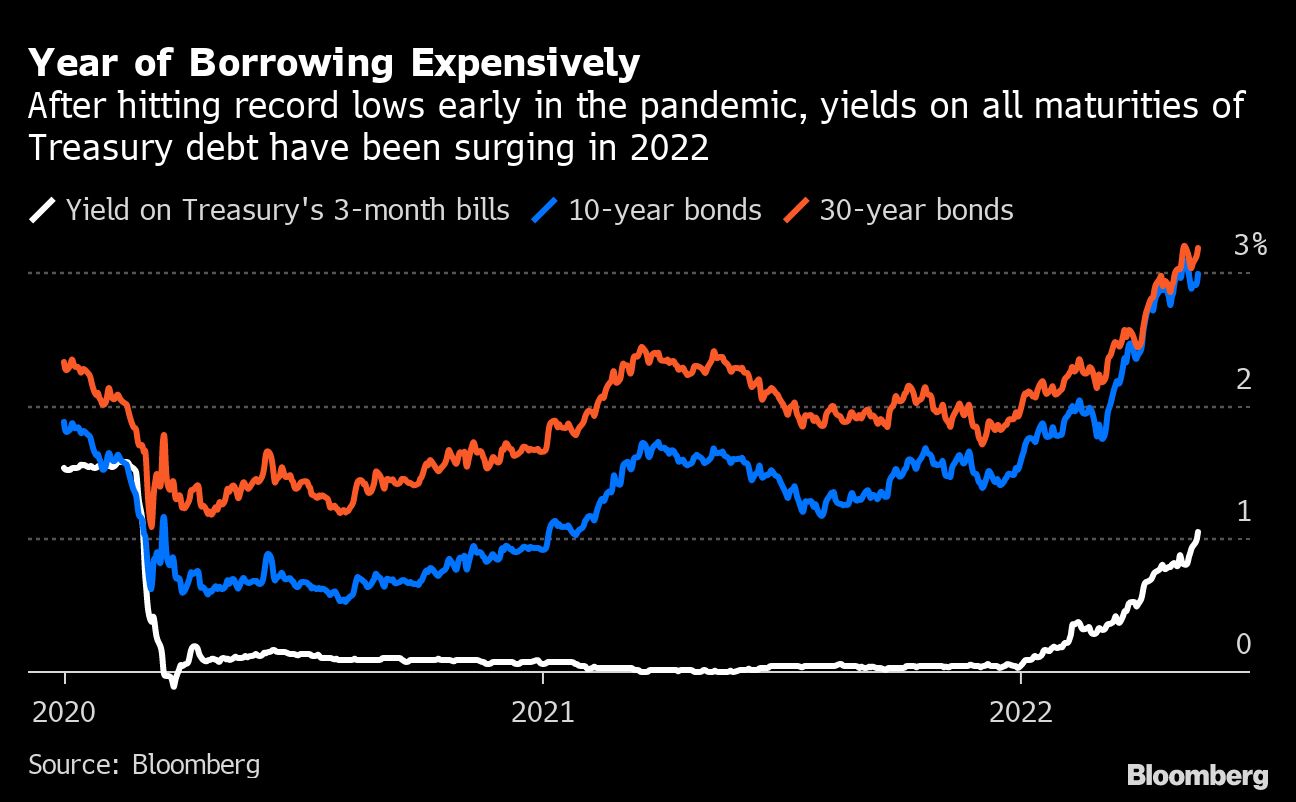

Treasuries extended their slump in New York, driving the yield on the benchmark 10-year note up by the most in more than three weeks, as renewed inflation concerns and economic data supported expectations for multiple Federal Reserve rate hikes in coming months.

The bear has ended a long hibernation.

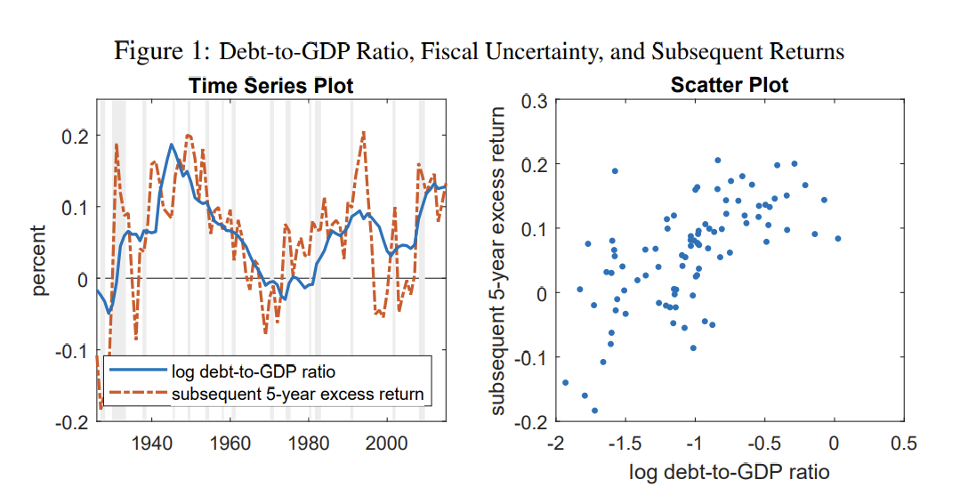

Our fiscal deficit, as measured by the debt-to-GDP ratio, has grown to levels that could impede growth, as predicted by financial theory and confirmed by empirical evidence. Moreover, new research shows that our burgeoning deficit could increase risk premiums for both stocks and bonds.

Summer is right around the corner, and traditionally that’s when families pack their bags and get away for a well-deserved vacation. Since this is the first summer travel season in three years that feels like the before times, airlines and airports are bracing for what is expected to be a particularly busy three months.

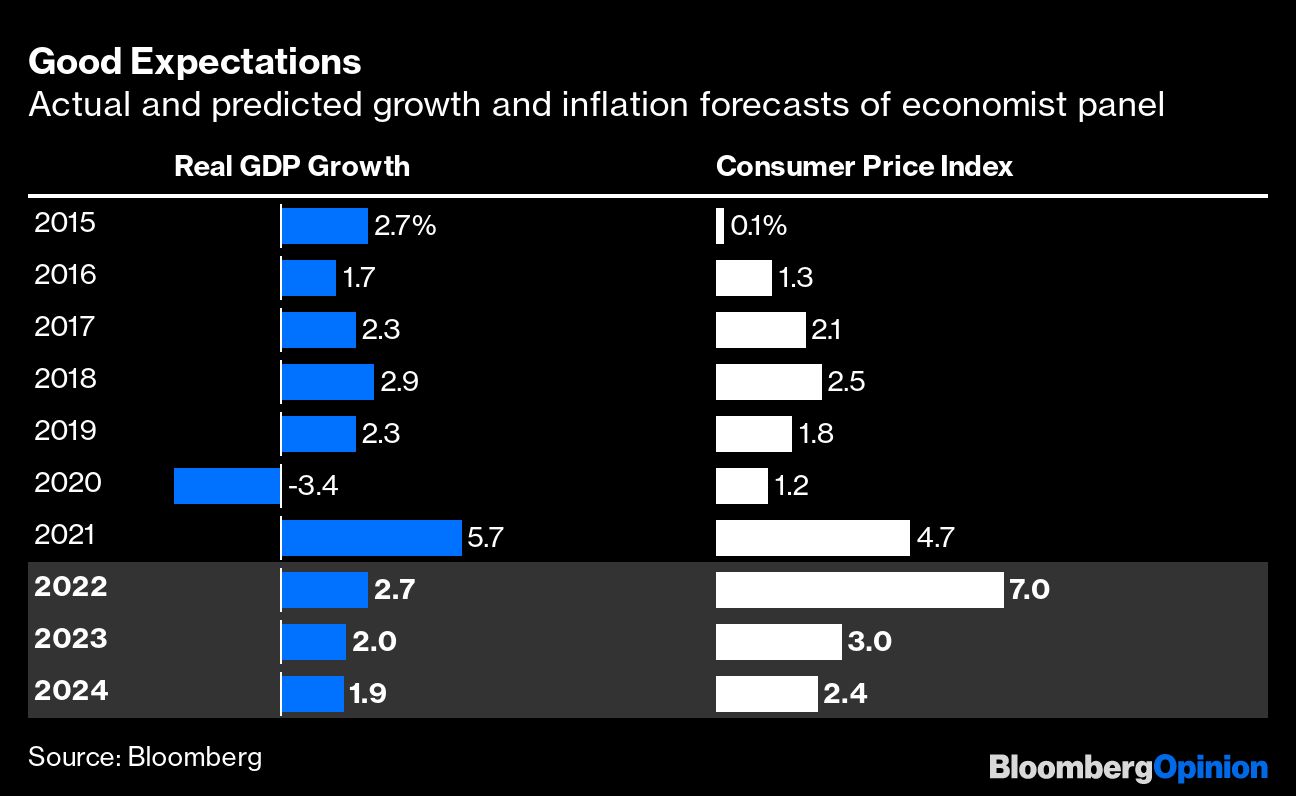

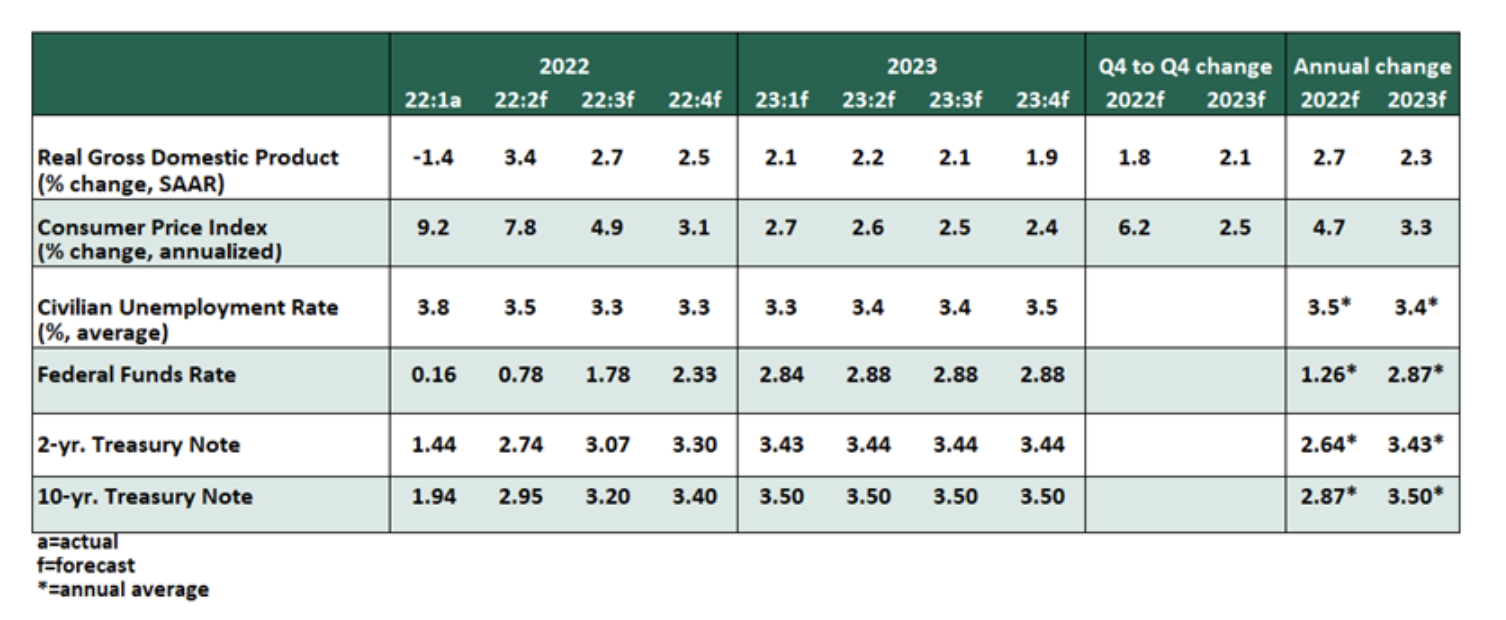

High inflation and the consequences of attempts to curb it are a top concern for today’s investors.

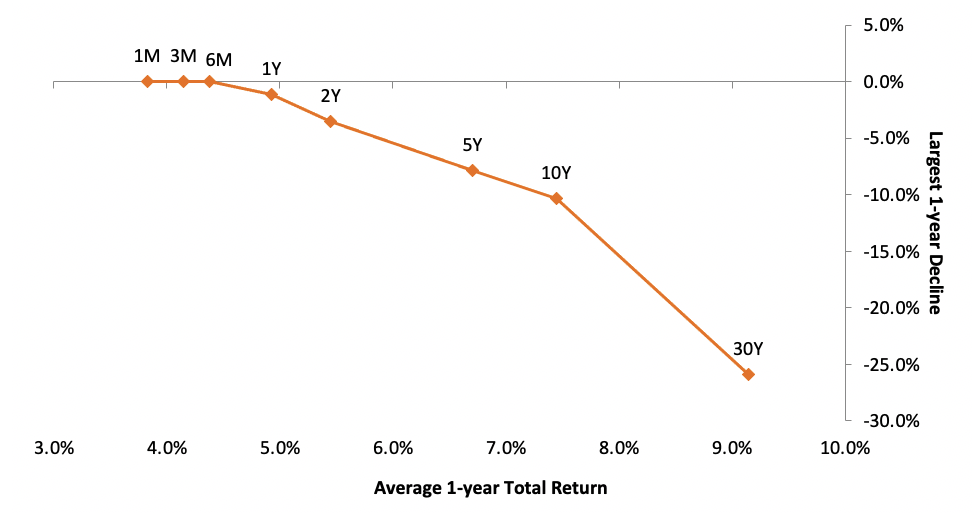

For investors wondering where to store cash, comparing the maturity profiles on Treasuries with their “risk of loss” history can help reveal where value might lie within shorter maturities.

Central bankers can’t drill for oil, grow more crops or repair global supply chains. That means the only quick fix available to Federal Reserve Chair Jerome Powell and his colleagues for cooling the fastest inflation in four decades may be raising interest rates so much that they crash the economy into recession.

Federal Reserve officials agreed at their gathering this month that they need to raise interest rates in half-point steps at their next two meetings, continuing an aggressive set of moves that would leave them with flexibility to shift gears later if needed.

Investors’ expectations that interest rates will not rise much may be very misguided.

The price of foods, fuels and other essential items are spiraling ever upward as Russia’s war on Ukraine compounds supply-chain woes stemming from the pandemic. Central banks may be in the driving seat when it comes to tackling inflation, but it’s governments that face the fallout and so are compelled to act.

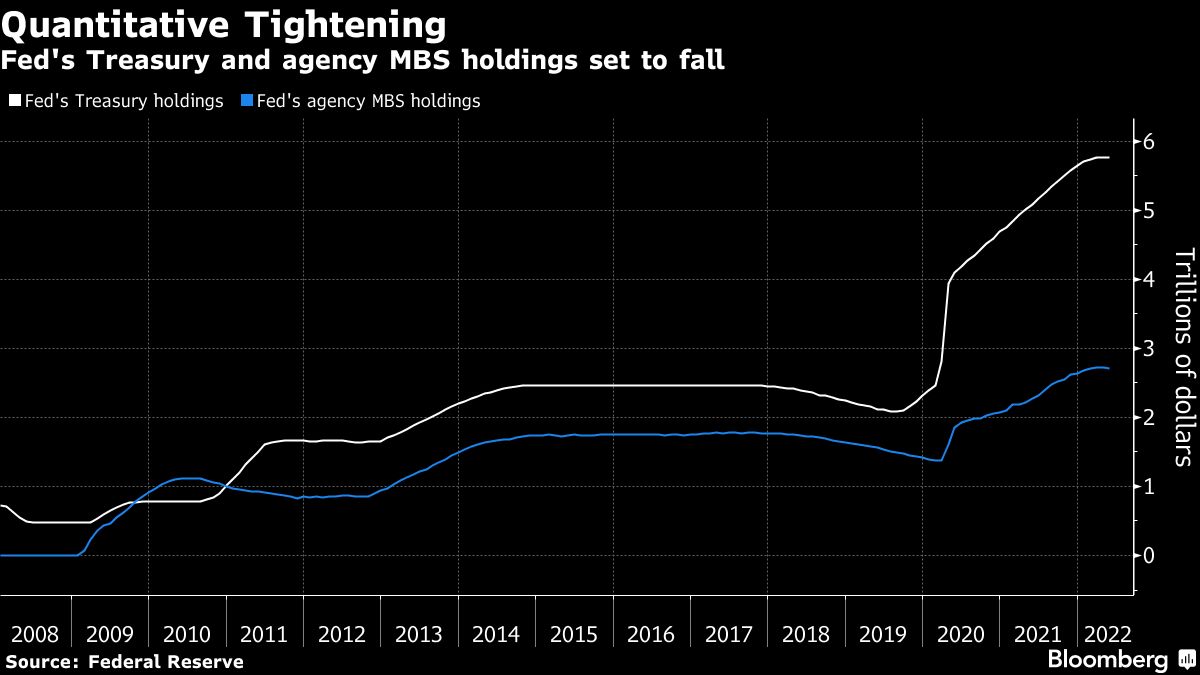

With the Federal Reserve releasing minutes from its latest meeting on Wednesday, traders are looking for further details on the plans to let billions of dollars worth of bonds to mature each month without replacing them.

Recent warnings from corporate executives and rapidly declining regional manufacturing surveys make me wonder if a recession has already started.

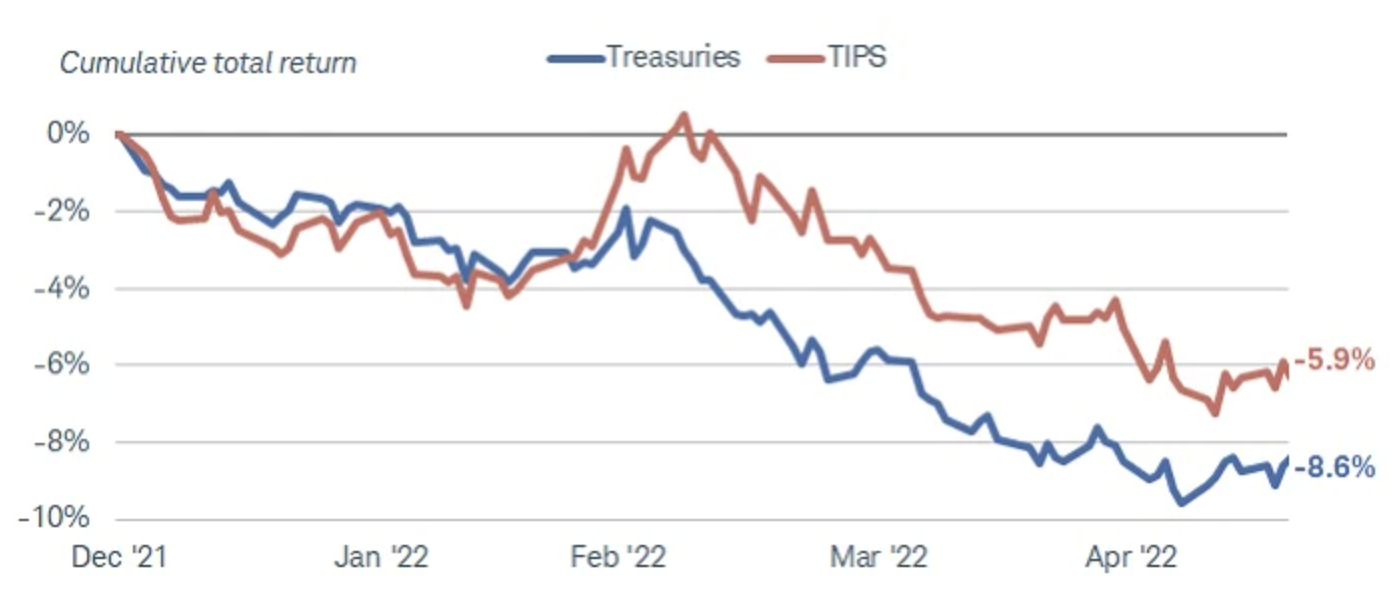

Treasury Inflation-Protected Securities, or TIPS, can help protect against inflation over the long run, but in the short term their performance may be dictated more by price declines in the secondary market.

U.S. equities are trading lower in afternoon action with the markets unable to extend yesterday's solid gains.

The future is always unknown.

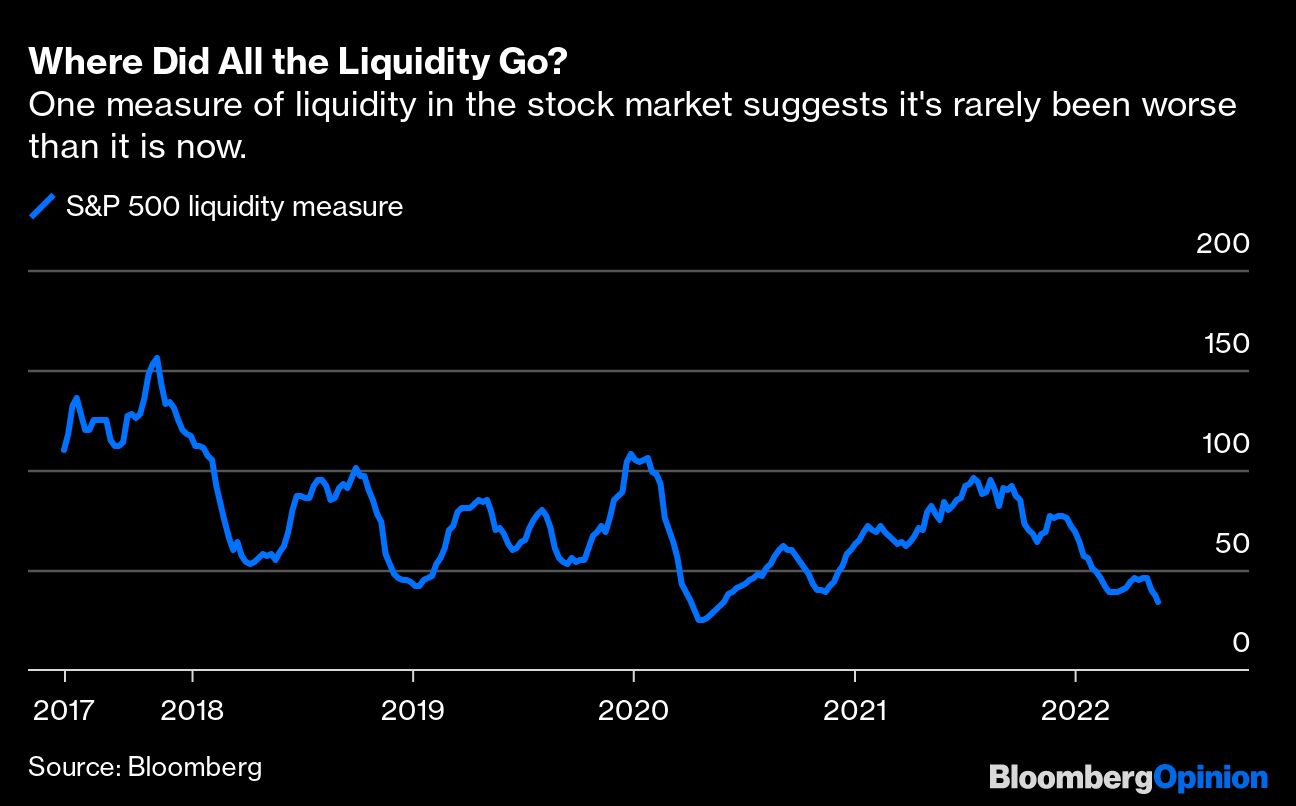

Liquidity is the lifeblood of the capital markets. It is the ease at which an asset can be turned into cash without disrupting the price of that asset. This was never really a concern in the US, whose markets are prized for being the deepest, most liquid in the world. It’s one reason why the dollar is the world’s dominant reserve currency.

All year inflation has been the narrative driving markets.

Stocks start the week higher following recent bearishness.

Wherever you get your news, there's no escaping the perception that rising prices are breaking the US economy. Recession is almost a foregone conclusion on the Bloomberg terminal, which aggregates 150,000 news sources with every bulletin categorized and counted. Headlines with the word “inflation,” increased 345% to 186,000 times a month since the beginning of 2020, while “strong economy” declined 48% to 1,766 times monthly.

As with bodily atherosclerosis, curing our economic condition may require lifestyle modifications. But in one sense, it will be even worse: We’re all going to get the cure whether we want it or not. We’ll get its side effects, too… and you can bet there will be many.

This week has seen a series of rapid contractions across the digital asset ecosystem. In a space that is well-known for volatility, even this week has stood out to observers.

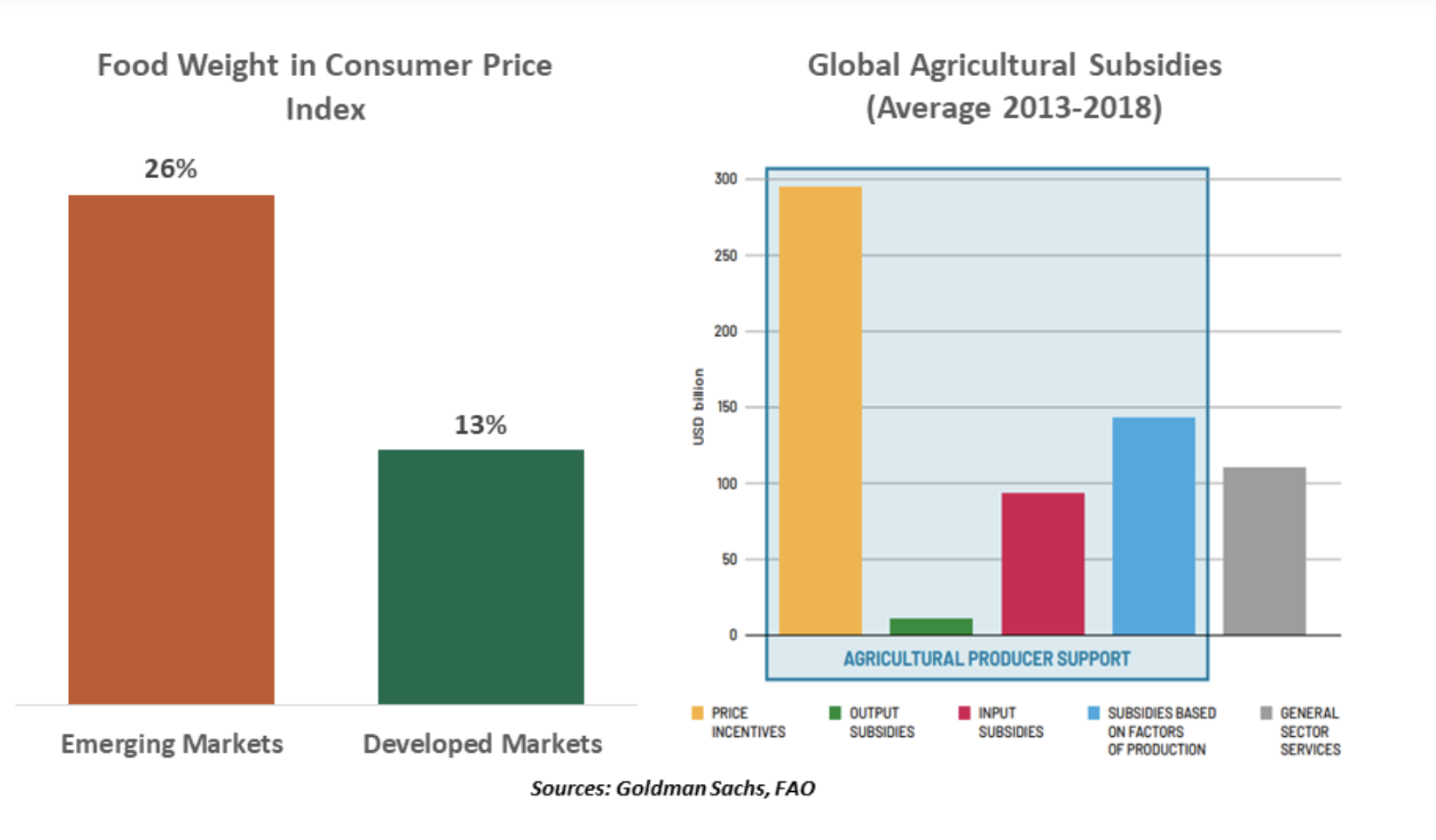

Soaring commodity prices have helped drive inflation to 8.5%, by far the highest level in the last few decades.

Since the global financial crisis, assets in private credit have grown exponentially as investors search for yield while protecting against inflation and rising interest rates.

Treasuries gained for a second day as investors sought out the safest debt, driving the 10-year yield down 11 basis points to 2.77%, it’s lowest level since late April. Weaker than forecast US jobless claims and a sharp decline in a regional Philadelphia Fed survey spurred a burst of buying in Treasuries, with equities futures indicating that stock prices will open lower.

“What does a yellow light mean? Slow down!

U.S. equities plunged, finishing near the lows of the day, following disappointing quarterly results from Target Corporation and Lowe's Companies, with both retailers warning of rising cost pressures.

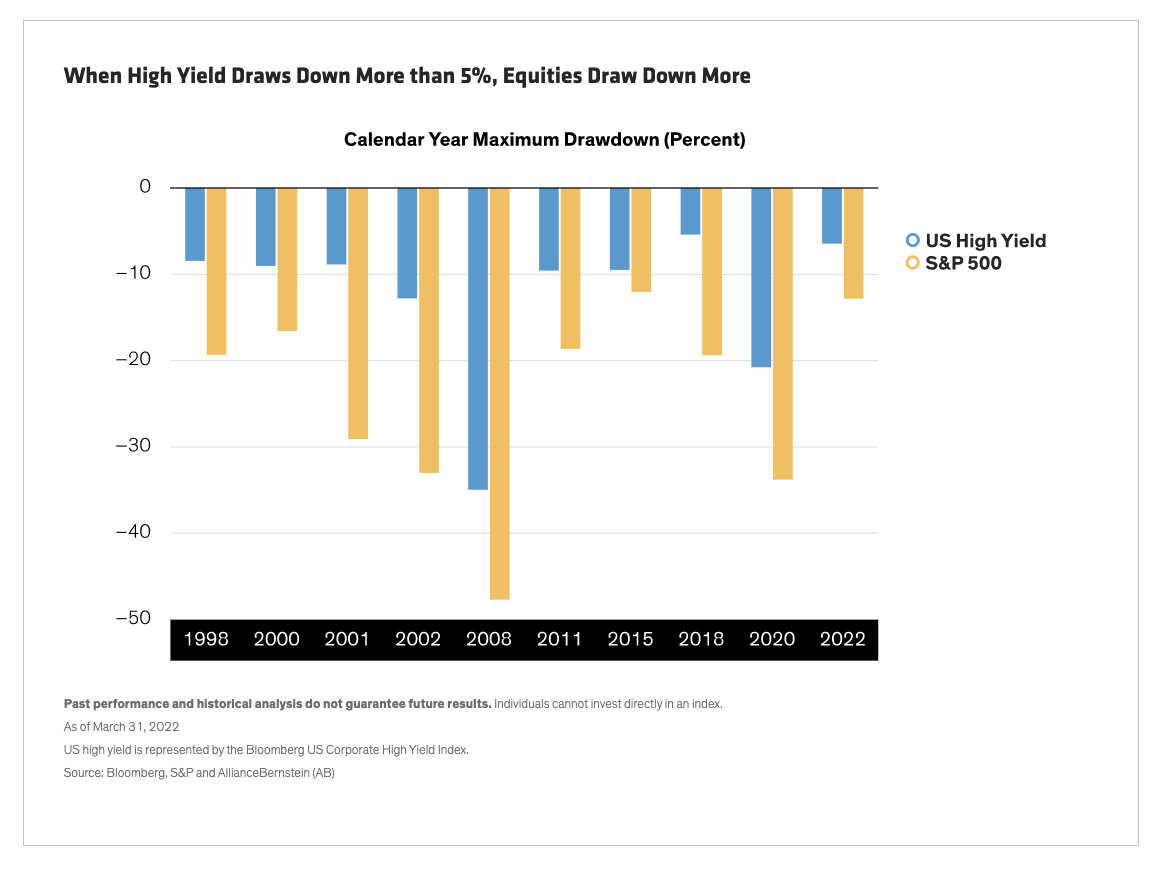

Looking for a tactical way to de-risk your portfolio? You might consider rotating a portion of your equity allocation into high-yield bonds.

Credit market volatility this year has been extreme.

If we follow the threads underlying inflation over the past year to their earliest beginnings, they run straight through the fog of pandemic, quickly pass by the financial crisis in 2008, and wind their way past the Great Inflation of the 1970s...

Like a supertanker, US debt-service costs only change course very slowly. But it’s happening now -- and from Washington’s point of view, the new direction is the wrong one: they’re heading up.

Federal Reserve Chair Jerome Powell, in his most hawkish remarks to date, said the US central bank will keep raising interest rates until there is “clear and convincing” evidence that inflation is in retreat.

Wylie Tollette, Head of Client Investment Solutions with Franklin Templeton Investment Solutions, joins the head of the Franklin Templeton Institute, Stephen Dover, for a conversation on the recent equity market selloff.

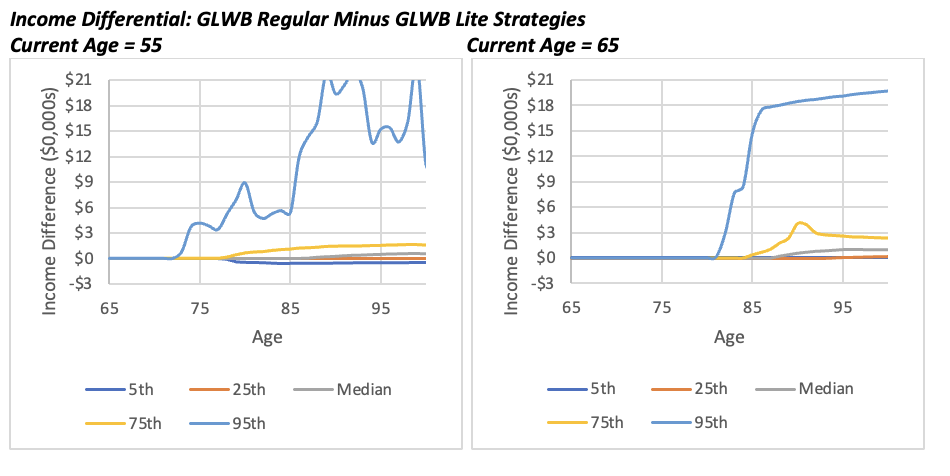

This article explores the benefits of annuities with lower explicit fees, a category I dubbed as “annuities Lite” in a previous article that focused on GLWBs.

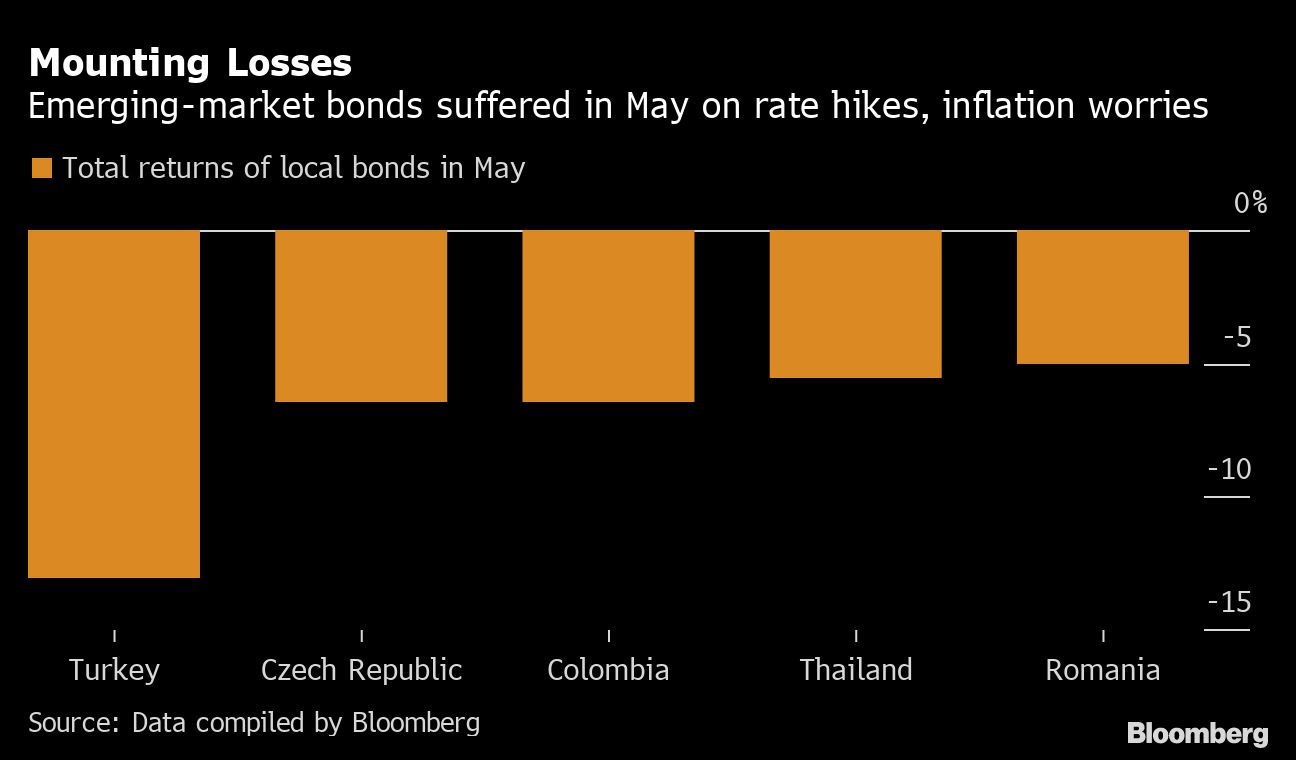

Local-currency debt from developing nations -- which is far more sensitive to a country’s domestic inflationary pressures than dollar denominated equivalents -- has slumped almost 9% this year, the most since at least 2008, according to a Bloomberg index.

U.S. stocks are trading lower as another week begins on the heels of six-straight weekly losses for the S&P 500.

When life gives you lemons: sell them!

Historical data shows that stock markets have reacted poorly when the Fed has contracted its balance sheet and reduced liquidity – and the effect is more pronounced when Fed actions deviate from what the market expects.

Some big-name investors forecast that Bitcoin will eventually hit $100,000, $1 million or more. It could very well do that, but for now, its price is closer to $0. That’s both a risk and an opportunity.

Rising yields, wider spreads, and heightened market volatility are providing an attractive environment, but caution in credit selection is warranted.

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates.

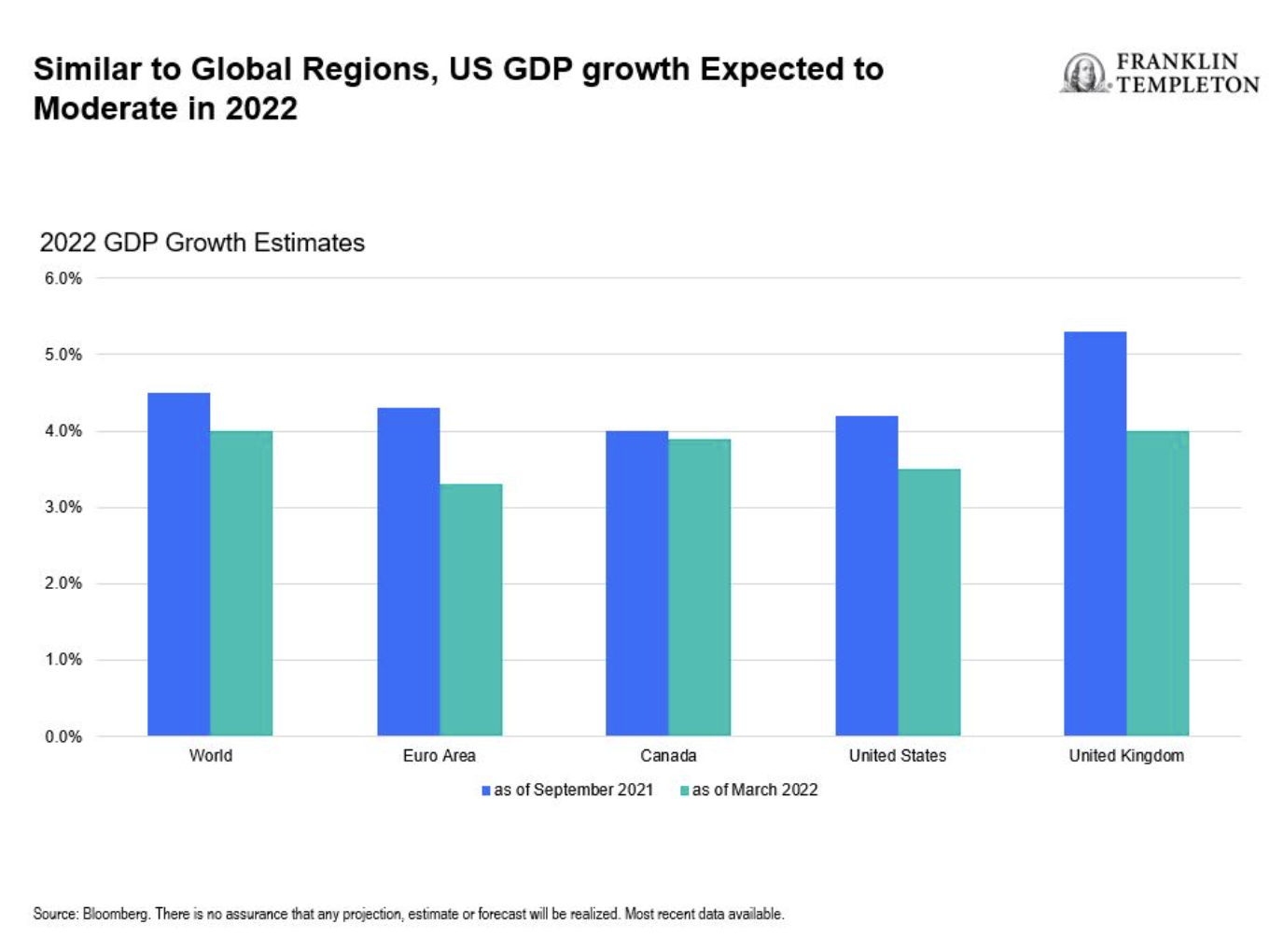

Coming out of the depths of the pandemic, US equity and fixed income markets are facing new challenges this year amid a rising interest rate environment and deceleration in growth.

In 1995, Treasury Secretary Robert Rubin asserted that a strong dollar is in the US national interest, a mantra repeated by each of his successors. They’re partially correct since the effects of the robust buck, which has soared this year, help some while harming others.

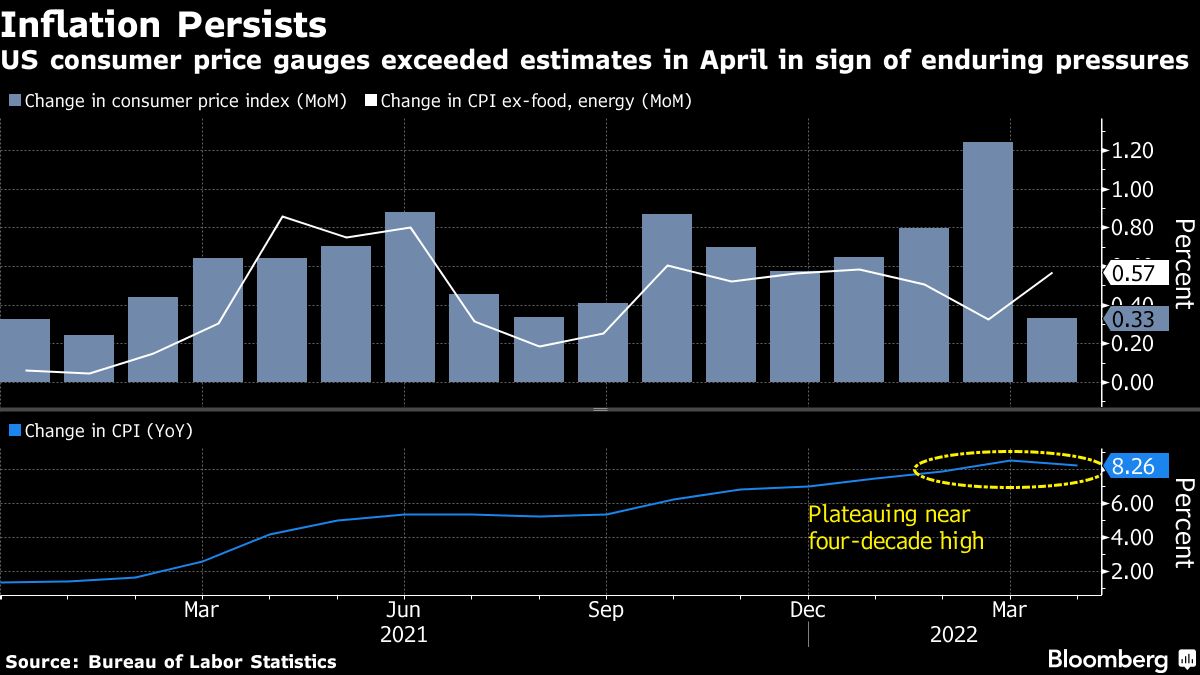

The latest US inflation report should be a reality check for Wall Street, but many investors are still wearing rose-colored glasses. Bond yields ticked slightly higher Wednesday after the Labor Department reported that consumer prices rose more than forecast last month, but they are still nowhere near reflecting the monetary policy path it may take to rein in inflation.

An unfriendly macro and market landscape is making life harder for investors today, with traditional core bonds coming up short on income. In our view, focusing on generating efficient income is an effective approach to tackling the challenge of mixing the key building blocks of rates, credit and growth.

The geopolitical crisis in Ukraine creates a stagflationary shock for global economies. The plan to fight inflation just got far more complicated for global central banks.