Nearly everyone holds some cash in their portfolio, either to invest later, pay upcoming expenses, or provide a counterbalance to riskier investments. Often, we aren’t exactly sure how and when we will spend or invest our cash, and thus want easy access regardless of market conditions. The basic choice is a 1-month Treasury bill, but really any Treasury instrument will do as they can be sold quickly if we need funds immediately.

Storing cash in Treasuries helps avoid credit or liquidity risk but may involve duration risk – if rates unexpectedly rise more than expected, then you could get back less than you invested. The main goal for reserves is liquidity, but there is a secondary goal of generating income to help mitigate the inflationary drag of holding cash.

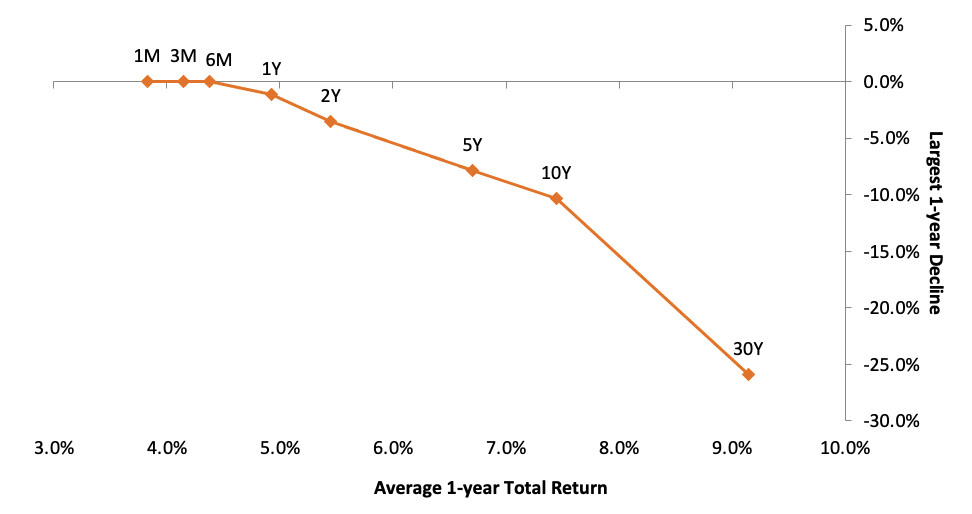

Exhibit 1 compares the historical average one-year holding period return for each major Treasury maturity (1-month, 3-month, 6-month, 1-year, 2-year, 5-year, 10-year and 30-year) versus its largest-ever one-year decline.

Exhibit 1: Average 1-Year Return vs. Largest 1-Year Decline (various Treasury maturities)

Source: FTSE Treasury Benchmark Index, Janus Henderson, January 1980 to April 2022. Note: Constant maturity total return series, rebalanced monthly, excludes transaction costs. Past performance is no guarantee of future results.

Clearly, historical returns are far above current rates. Nevertheless, the graph shows that despite various periods of rising and falling rates over the last 42 years, holding 1-year or 2-year Treasuries rather than shorter bills has generally enhanced returns while introducing minimal drawdown risk. Interest rate sensitivity for these maturities is low as existing hike expectations get priced in. For example, the 2-year note today already reflects the rising rate profile implied by markets and the median path of the Federal Reserve (Fed) dot plot, which records each Fed official’s projection for the federal funds rate.

Consequently, even if the Fed increased rates by a further 2.5% or so over the next two years, the total return from rolling 1-month bills versus buying a 2-year note today would most likely be similar.

However, there is a possible asymmetry: If the Fed slowed its hiking pace, perhaps due to falling markets, economic slowdown, or moderating inflation, then the 2-year holder would come out ahead if all of the expected hiking didn’t come to pass.

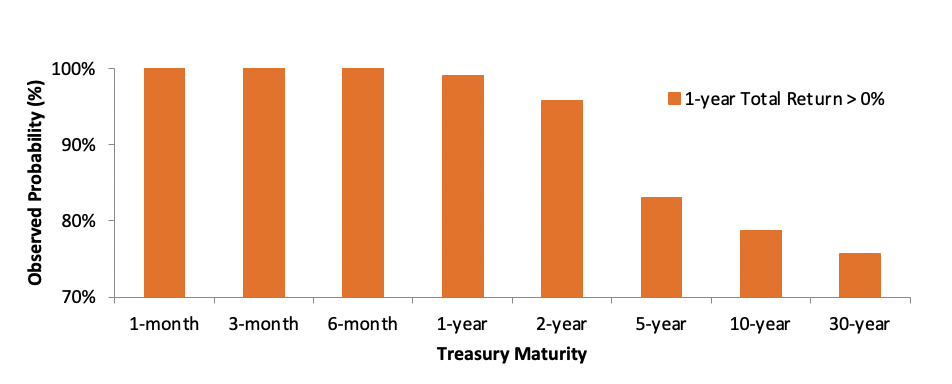

Another way to compare holding cash in various Treasury maturities is the observed probability of achieving a positive total return over a one-year holding period. This is shown in Exhibit 2.

Exhibit 2: Historical Probability of a Positive 1-Year Total Return (various Treasury maturities)

Source: FTSE Treasury Benchmark Index, Janus Henderson, January 1980 to April 2022.

Note: Constant maturity total return series, rebalanced monthly, excludes transaction costs.

Past performance is no guarantee of future results.

Through the 2-year Treasury maturity point, the likelihood of an outright capital loss is low, but the risk rises quickly as duration is extended. This makes 5-year or longer-dated Treasuries a less suitable investment choice if capital preservation is the primary goal.

There is high demand for short-term (1-month, 3-month) Treasury bills for legal, collateral and other funding reasons, which reduces their yield. Instead of owning bills, holding a portfolio of 2-year bonds (versus rolling 1-month bills) has added, on average, 1.6% extra return per year with minimal risk of a large drawdown.

At today’s rates, and with more hikes expected, the potential benefit from extending is smaller, but likely still positive. Accordingly, if you are holding cash reserves in 1-month bills out of rate hike fears, then you are probably better off buying, say, 1-year to 2-year paper because the incremental duration risk is largely offset by the higher starting yield.

By extending modestly, you can immediately increase interest earned (e.g., for Treasuries, the current 1-month rate is 0.42% but the 2-year rate is 2.67%).1 You could also benefit if rates rose more slowly than the already anticipated pace of hikes.

1 As of May 18, 2022.

High-yield or "junk" bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

U.S. Treasury securities are direct debt obligations issued by the U.S. Government. With government bonds, the investor is a creditor of the government. Treasury Bills and U.S. Government Bonds are guaranteed by the full faith and credit of the United States government, are generally considered to be free of credit risk and typically carry lower yields than other securities.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

The opinions and views expressed are as of the date published and are subject to change without notice. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

This material may not be reproduced in whole or in part in any form, or referred to in any other publication, without express written permission.

Janus Henderson is a trademark of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc

C-0522-43607 05-15-23

© Janus Henderson Investors

Read more commentaries by Janus Henderson Investors