Introduction

Soaring commodity prices have helped drive inflation to 8.5%, by far the highest level in the last few decades. With commodity prices up and inflation creating waves, is it too late for investors to capitalize on high commodity prices? Have investors missed their chance to protect their portfolios from inflation? Historically, resource equities have provided stellar performance during inflationary periods,1 and this time has been no different. Resource equities have been the best performing asset class over the last 2 years yet continue to trade at extremely attractive levels that don’t reflect current commodity prices. Let’s consider some of the important dynamics in commodity markets and then turn to the surprisingly attractive opportunities in the resources sector. Shorter-term and longer-term dynamics in commodity markets Commodity prices are generally driven by short-term supply/demand dynamics. Currently, there are a few major factors impacting short-term supply and demand. On the demand side, we have a global economy, boosted by an abundance of stimulus, striving to return to “normal” after two miserable years dealing with Covid. Commodity producers have struggled to meet this demand, as they’ve dealt with an assortment of pandemic-related challenges, including supply disruptions and labor shortages. Into this already potent mix, the Russia/Ukraine crisis has been added.

Russia is one of the largest commodity producers in the world with critical supplies across energy, metals, and agriculture. Russia produces more than 12% of the world’s oil and is the world’s largest natural gas exporter, including, as we all know, being a major supplier to Europe. The Black Earth region spanning Russia and Ukraine is home to large swaths of extremely fertile soil, producing almost 30% of the world’s wheat and ranking as one of the top two or three producers of many agricultural commodities. On the mining front, Russia is a major producer of nickel, platinum group metals, potash, phosphate, and coal, along with many other materials. With Russia involved in a shooting war with Ukraine and an economic war with the West, already stressed commodity markets have become more stressed. Oil has traded over $120 per barrel, while nickel, phosphate, and wheat all jumped over 30% in the days following the invasion.

These shorter-term factors obscure, in some ways, and exacerbate, in others, critical underlying longer-term dynamics that will impact commodity prices for many years to come. On the demand front, we have a global population rapidly approaching eight billion and headed significantly higher from there. More importantly, a large proportion of the global population resides in developing countries that will continue to go through the stage of economic development that is particularly commodity-intensive for decades. Building out cities, infrastructure, electric grids, and so on requires tremendous amounts of resources, and the world has never seen countries the size of China, India, or even Indonesia attempt to go through this stage of development.

In addition, decarbonization efforts will spur demand for clean energy materials far beyond anything we’ve seen before. Transitioning from fossil fuels to clean energy does not absolve the world from the need for natural resources. In fact, the clean energy economy will be as reliant on natural resources as our current economy. It will just be a different set of resources. Instead of oil, coal, and natural gas, we’ll need lithium, nickel, cobalt, and manganese for our electric vehicle (EV) batteries, vanadium for our utility scale energy storage, silver and polysilicon for our solar panels, iron and zinc for our wind turbines, and copper for…well, just about everything.

Copper will be the oil that drives the engine for a decarbonized economy. Four to fifteen times as much copper goes into solar and wind projects relative to comparably sized coal or natural gas power plants. EVs use three to four times as much copper as internal combustion engine vehicles. EV charging infrastructure, energy efficiency efforts, electric grid enhancements, and electrification all rely on heavy copper usage.

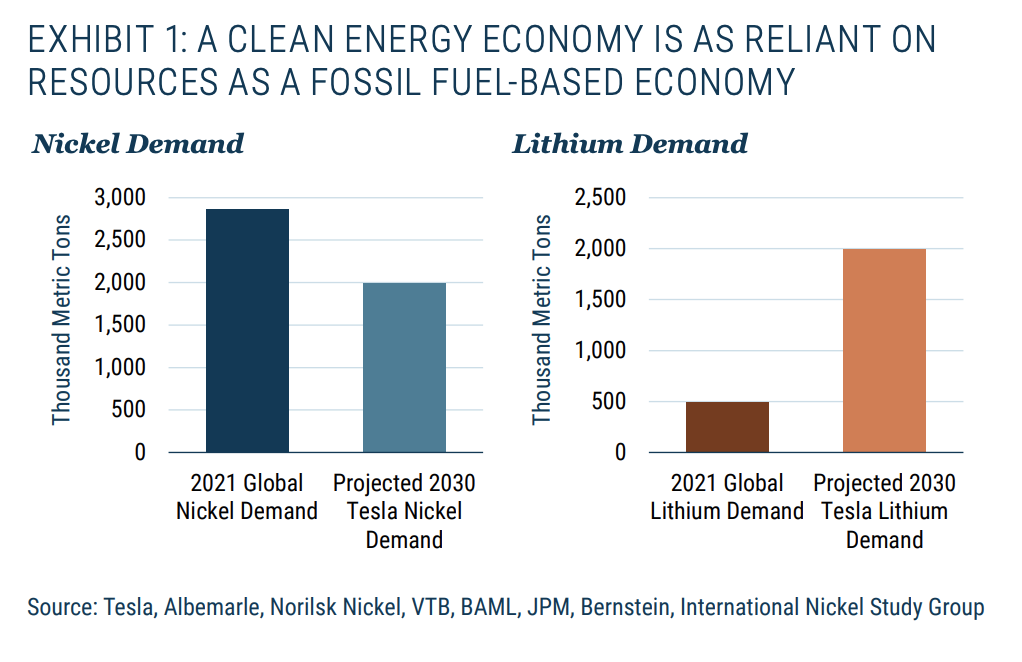

To put the demand growth for clean energy materials into perspective, let’s look at Tesla. At its Battery Day last year, Tesla projected three terawatt hours of lithium-ion battery capacity needed in 2030 for the EVs and storage they expect to produce. To reach this target, Tesla alone would gobble up approximately 75% of the world’s current nickel production and four times the world’s current lithium production (see Exhibit 1). These numbers are astounding enough, but when one considers that EVs currently represent just 15% of global nickel demand and about 45% of lithium demand and that Tesla will likely be producing only a small proportion of the world’s EVs in 2030, the implications are staggering. Clean energy materials companies will make a lot more money in the decades to come than they ever have both because they will be selling a lot more metric tons of material and because there are certain to be shortages where supply can’t keep up with the rapidly growing demand

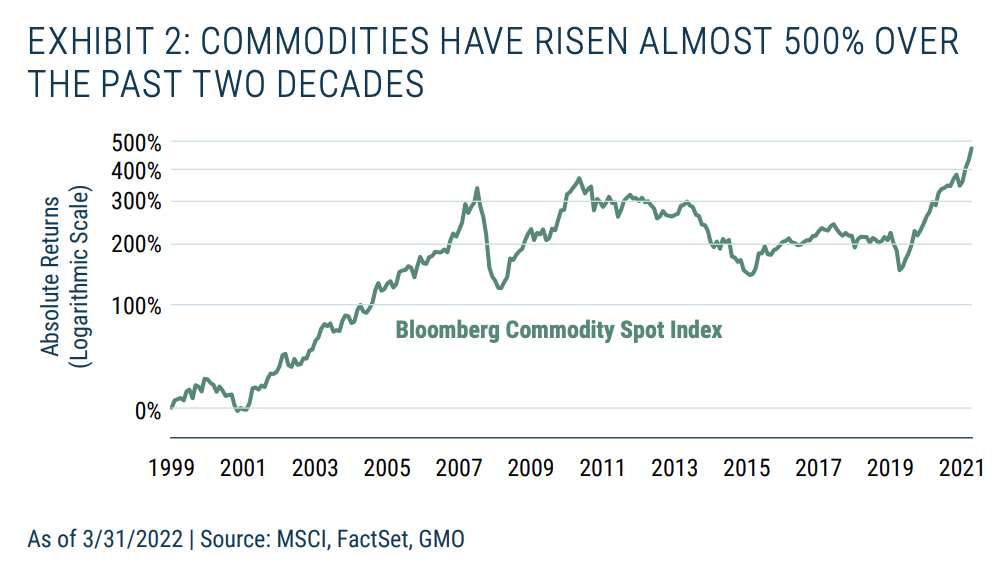

Population growth, economic development, and decarbonization pretty much guarantee substantial, potentially explosive, growth in commodity demand. We better start ramping up supply, right? That’s where things get sticky. Resource scarcity is a frightful challenge. Natural resources are, of course, inherently finite. More critically, cheap, easy to access, easy to process resources in politically stable regions with existing infrastructure, transportation systems, and available labor supply are even more scarce. Ultimately, price signals are the strongest proof of scarcity. The Bloomberg Commodity Spot index,2 perhaps the most widely followed basket of commodity prices, is up almost 500% since the beginning of 2000 (see Exhibit 2). It’s hard to imagine any plausible explanation for such a dramatic surge in commodity prices that doesn’t include a healthy dose of scarcity.

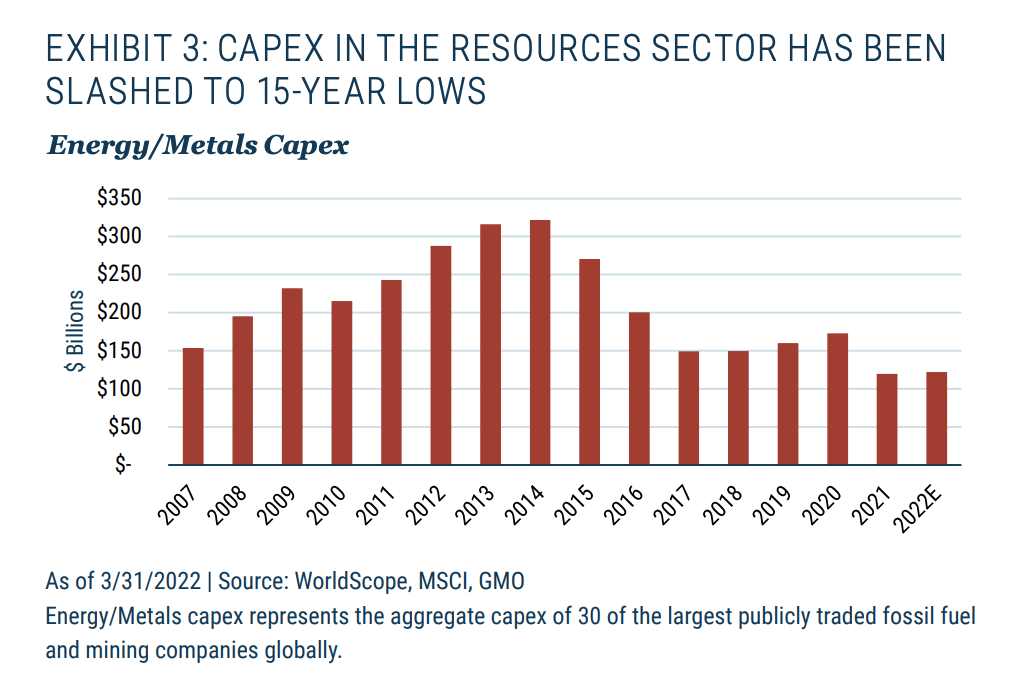

Unfortunately, resource scarcity isn’t the only supply challenge we face. Underinvestment in supply in recent years will impact production for at least the next decade. Over most of the last decade, commodity prices have been falling or low. Commodity producers, reacting to low prices and criticism that they had overinvested during the China-driven commodity supercycle, slashed capex significantly (see Exhibit 3). Pressure from ESG/sustainability circles and divestment campaigns also sought to starve fossil fuel companies of capital. Then, Covid hit, and resource companies cut capex again. Given that the world consumes around 40% more of many major commodities (e.g., natural gas, iron ore, copper) than it did 15 years ago, it’s somewhat stunning that capex levels would be at 15-year lows. Furthermore, the capital intensity of commodity production has also risen substantially in recent decades as we’ve moved from higher- to lower-quality assets. In short, current capex levels are totally insufficient if we are to meet growing global demand.

Adding fuel to the fire, ramping up commodity production generally takes a long time. First, you need an asset to develop, and in recent decades, new, high-quality discoveries are down dramatically. Once an asset has been identified and acquired, projects can take 10 years or longer to begin production. More stringent permitting and higher environmental hurdles have lengthened project lead times even further. If we end up running into the structural deficits that appear to be looming for many commodities, there will be no quick fixes.

As if scarcity and underinvestment aren’t enough to deal with, geopolitical tensions have led to increasing discussion of deglobalization, energy security, and supply chain independence. If countries move to shore up more control over their resource supplies, lost efficiencies will push commodity prices even higher (e.g., we’ll pay more for expensive U.S. shale oil rather than buying cheap Russian oil).3

Given the various supply/demand dynamics in play, it’s easy to see why many commodity analysts see the recent spike as the beginning of the next commodity supercycle.

What will happen to fossil fuel prices during the clean energy transition?

One commonly expressed view is that the clean energy transition will displace fossil fuel demand, leading to lower prices. The analyses that form this view, unfortunately, completely ignore the supply side of the equation. If you don’t invest hundreds of billions of dollars in capex each year, for example, you see depletion rates of 6-8% for conventional oil wells. Shale depletion rates are much, much higher, averaging around 70% by the end of the first year. If fossil fuel companies see demand disruption, they’re bound to cut capex, leading to a significant reduction in supply and perhaps, counterintuitively, higher prices.

Furthermore, it’s important to note that passenger cars drive just a little more than a quarter of global oil consumption. No matter how quickly we transition to EVs, it’s hard to imagine displacing even 2-3% of oil demand per year. To underscore this point, despite significant growth in EVs in recent years, the International Energy Agency (IEA) expects the world to consume a record amount of oil in 2022. You can be forgiven if you find it alarming that we haven’t even started moving in the right direction.

If investment in production is constrained, fossil fuel prices could stay high even as we eventually displace demand. On a recent quarterly earnings call, BP CEO Bernard Looney took a page out of my book and said much the same: “…you could see a world where because of lack of investment, even though the energy transition is accelerating, oil prices are much, much higher…”

Valuation of commodity producers

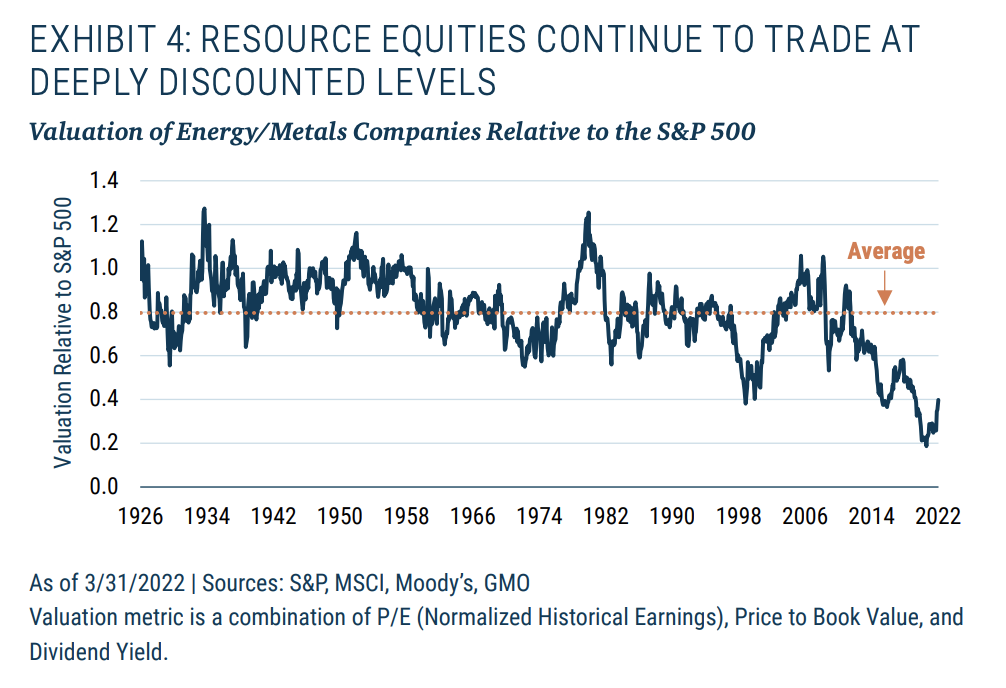

Commodity prices have skyrocketed well over 100% in the last 2 years. However, it’s not too late to invest. Though commodities are up, resource companies trade at more than a 60% discount relative to the S&P 500 (see Exhibit 4), a level that has almost never been seen. Furthermore, the current discount may be understated, as the recent spike in commodity prices has yet to flow through to the companies’ reported fundamentals. Thus, it’s reasonable to conclude that the commodity producers are actually quite a bit cheaper relative to their current ability to generate profits than the chart below would suggest.

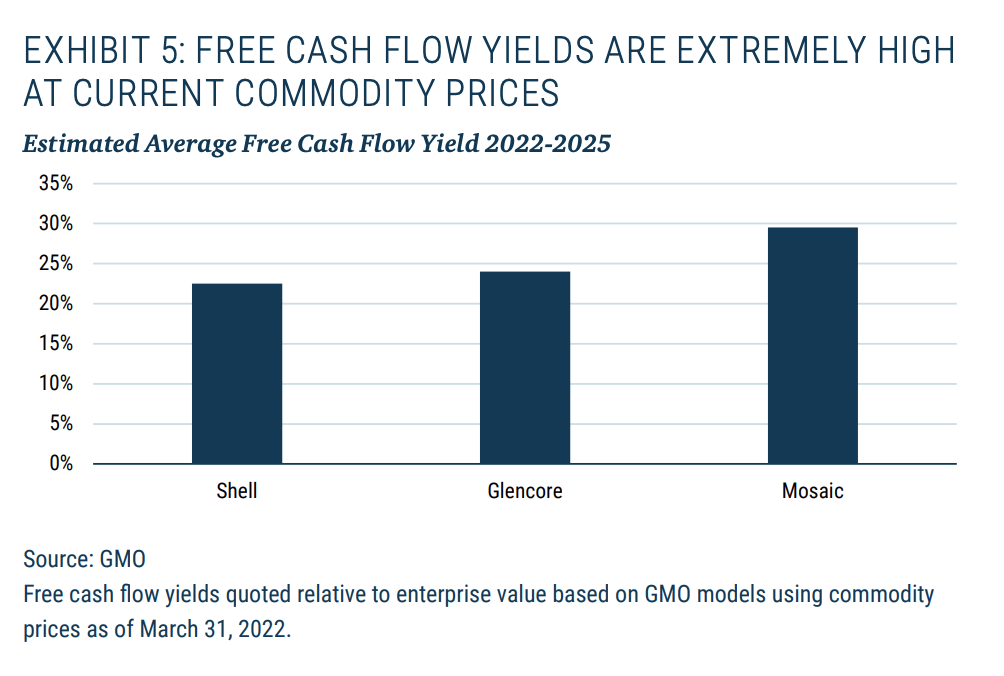

The market is simply not valuing resource companies at reasonable levels given any plausible base case for how the world might play out, in our opinion. With oil prices up around 65% and natural gas prices up hundreds of percent since the beginning of 2020, Shell, a bellwether for the oil and gas industry, is more or less flat. With the movement in oil and gas prices, one would have expected Shell’s stock price to surge. It didn’t, however, leaving Shell at very attractive valuation levels. At commodity prices as of the end of the first quarter, Shell would be cranking out free cash flow yields of 22-23% for the next few years according to our models (see Exhibit 5).

And it’s not just fossil fuel companies. U.K. listed mining titan Glencore weighs in at free cash flow yields of around 24% over the next few years, while major U.S. fertilizer player Mosaic tilts the scales at almost 30%. If you’re willing to venture into smaller cap names and/or emerging markets, the disconnects can become even larger. To put these yields into perspective, the free cash flow yield of the S&P 500 was around 4% in 2021. Think about these numbers. If commodity prices were to stay at current levels, many of the largest commodity producers on the planet could pay down all their debt and buy back all their shares in just a few years and keep their billions and billions of dollars of cash flow for themselves.

The implication of these deeply discounted valuations is that investors don’t need commodity prices to continue to rise in order to expect strong returns. In fact, flat commodity prices would be brilliant. Stable commodity prices from this point would lead to hundreds of percent returns, in expectation, for many resource equities. When we model commodity producers, we typically use trailing five-year average commodity prices. Even with these much lower commodity price assumptions, our models show double-digit free cash flow yields for many companies going forward. Hence, there’s a significant margin of safety, not a term that you typically hear applied to commodity producers. And, of course, if commodity prices rise from here, we would expect resource companies to produce truly outstanding returns.

Why are resource companies so cheap?

Why do commodity producers trade at such large discounts? One might expect resource equities to be popular given their strong diversification and inflation protection characteristics, but investors hate them. Disasters like oil spills, mining accidents, and dam collapses loom. Perhaps more importantly, the volatility, cyclicality, and commodity price uncertainty are difficult for investors to tolerate and have led many to hold trivial positions or forgo the sector altogether. These dynamics have always existed and have helped commodity producers to trade at a 20% discount on average (Exhibit 4), leading resource companies to outperform the S&P 500 by over 2% per annum since the 1920s.

The discount has become much larger in recent years, as the relatively small cadre of investors willing to wade into the sector has shrunk further. ESG, sustainability, and divestment campaigns have gathered significant momentum. Electric vehicles have dominated the headlines, if not our roads. The imminent demise of fossil fuels has been touted relentlessly by the media. Coupled with the sector’s poor performance over most of the last decade, it’s easy to understand why multiples have dropped and resources exposure in the major market indices has fallen to just a few percent.

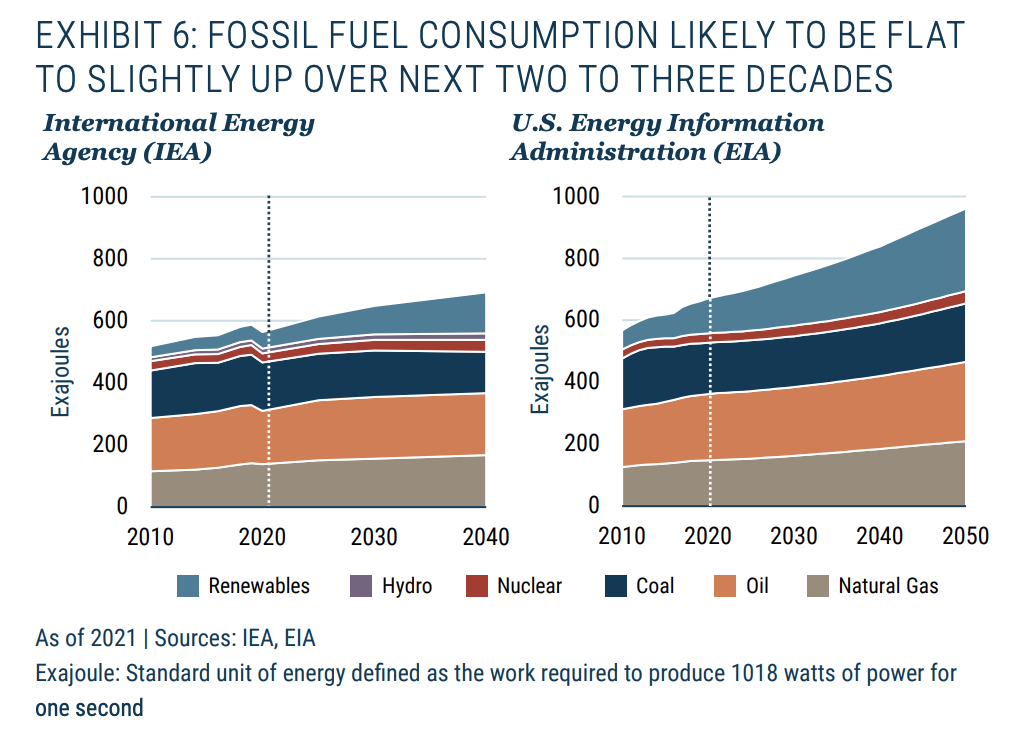

However, transitioning from fossil fuels to clean energy, while urgently needed, will take decades. It took us over 150 years to build our current fossil fuel-based energy infrastructure. We’re not going to replace it in a decade or two. In fact, the IEA and the U.S. Energy Information Administration (EIA), organizations focused on projecting energy consumption patterns to assist policymakers, paint similar pictures for the next two to three decades: fossil fuel consumption staying flat or perhaps even rising a bit with renewables servicing the growth in energy demand (see Exhibit 6).

For the sake of the planet, we’d better hope they’re wrong, but the reality is that the world is not on a path to dramatically reduce fossil fuel consumption in the next 20 to 30 years. While EV sales are growing rapidly, 97% of vehicles sold in the U.S. last year had internal combustion engines (i.e., run on oil-based fuels); globally, the number was around 94%. Despite vehicle sales having been significantly suppressed by Covid the last couple years, around 400 million internal combustion engine (ICE) vehicles were sold in the last 5 years, almost twice as many as the analogous 5-year period ending 20 years ago and 4 times as many as the period ending 30 years ago. Given a typical useful life of 10 to 15 years, we’re going to need a lot of oil to fuel these recently purchased vehicles and the ICE vehicles that are going to be sold in the years to come.

Furthermore, as mentioned earlier, passenger cars represent just a little more than a quarter of global oil consumption. Other drivers of oil demand include petrochemicals, long-haul trucking, shipping, aviation, agriculture, and electricity generation, among many other uses. There are no imminent clean solutions for many of these applications, which is, of course, why the world focuses so much on EVs. To top things off, fossil fuels and clean energy materials will be needed in massive quantities to produce the wind turbines, solar panels, EVs, and energy storage systems that the world desperately needs

As those familiar with GMO are no doubt aware, our heads aren’t in the sand on climate or the need to transition as quickly as possible to clean energy. People like easy answers, but unfortunately, there are none when it comes to climate or to the investment implications associated with climate. Whether we like it or not, fossil fuels will continue to play a critical role in the economy. Investors don’t have to choose between investing in climate or investing in natural resources. There are exciting and overlapping opportunities in both, and the world will need both in order to function for the foreseeable future.

More than one way to win

Given the disfavor the resources sector finds itself in, it’s hard to predict what, if anything, might bring valuations back to more “normal” levels. As an investor, however, it’s not clear that it matters all that much. If the market starts to appreciate the cash flows resource companies are kicking off and applies a higher multiple to them, investors will be rewarded with a quick win. However, in the absence of improved sentiment, the resources sector will continue to pile up the profits…and investors will continue to own their share of those profits. If valuations remain depressed, investors will benefit from a combination of high dividend yields, special dividends, share repurchases, and M&A activity. While the exact mechanism is unknown, if you invest in profitable businesses at attractive valuations, you will be rewarded.

Let’s look at Vale, the world’s largest iron ore producer, as a case study for how shareholders can be rewarded. Vale’s stock price is about where it was at the beginning of last year. Despite the market’s lack of enthusiasm, the company generated about $20 billion of free cash flow last year. Not bad for a company with a market cap of a little over $100 billion and no substantive debt as of the end of March.4 What did the company do with all that cash? Last year, Vale paid out about $9 billion in regularly scheduled dividends and distributed another $10 billion between extra dividends and share repurchases. Combined with dividends distributed in the first quarter of this year and a recently announced share repurchase, Vale has returned or announced the return of over $33 billion since the beginning of last year, almost a 32% yield relative to the market cap of the company. Not a bad way to win.

Of course, Vale isn’t the only company returning boatloads of capital. Shell, BP, Glencore, Rio Tinto, Mosaic, and many other companies have been funneling cash back to their shareholders, and, given that commodity prices have spiked up in recent months, one could reasonably expect these capital returns to be bigger going forward.

Of course, things can always go wrong

What could go wrong? There are always short-term risks. High commodity prices could drive demand destruction. Covid doesn’t seem like it’s done with us yet. A strong U.S. dollar could be a headwind for commodity prices in dollar terms. Supply disruptions could ease. We could see resolution of the Russia/Ukraine conflict, which, of course, would be a great thing for the world, but any normalization of the West’s relations with Russia would likely lead to a significant drop in commodity prices.

There are longer-term risks to consider, as well. Windfall taxes or higher royalties could reduce realized returns. With the rise of populist movements around the world, particularly in Latin America, politicians may go after a greater share of the profits. Of course, this is a good problem to have, to some degree, as it means there are supernormal profits worth plundering. Furthermore, countries want to harvest the benefits of their natural resources and don’t want to discourage investment. Hence, a lot of these conversations and proposals end up being more bark than bite. If commodity prices rise into the future, windfall taxes and the like will be a factor but are ultimately unlikely to change the big picture. The last two decades have seen commodity prices at much higher levels than prior decades, yet company profits have been left alone for the most part.

Another risk to keep an eye on in the long term is overinvestment in supply. As discussed, this isn’t an imminent concern, as the current challenges revolve around underinvestment, and it can take more than a decade for supply response to come to fruition. However, capital discipline needs to be carefully considered, and striking the right balance between investing in needed production growth without overinvesting is tricky to say the least.

The big long-term risk that stands out is China. If China invades Taiwan and ends up locked in economic conflict with the West, all bets are off. Such a scenario would have far-reaching impacts on many markets, not least of all commodity markets, as China is a massive consumer of natural resources.

As is always the case in the resources sector, risks abound but so do the opportunities, and investors are being well compensated to take those risks. With a long-term timeframe, we believe investors in the resources sector can expect strong returns, diversification, and inflation protection with a significant margin of safety.

Conclusions

The long-term supply/demand dynamics in natural resource markets favor high and rising prices. The clean energy transition will take decades to play out and will, in fact, be a major driver of commodity demand. The recent run in commodities has exposed some of the underlying dynamics in the sector, among them, resource scarcity, strong and inelastic fossil fuel demand, growing clean energy material demand, and underinvestment in supply in recent years.

While commodity prices have risen, the resources sector continues to trade at extremely attractive valuation levels. However, investing in the resources sector is not for the faint of heart. There is a wide dispersion in the attractiveness of companies within the sector, investors need to keep an eye on capital allocation programs, and the volatility within the sector produces entry/exit points that must be navigated nimbly. Despite the challenges, investors willing to wade into these waters are likely to be richly rewarded.

With the recent spike, inflation has become a central issue for investors again. After decades of relatively low inflation, many investors were unprepared or had even allocated away from real assets over the past decade. What if you could protect your portfolio from inflation after the fact? If commodity prices stay high from this point, resource equities are likely to produce outstanding returns given the depressed valuations in the sector. It’s not too late to protect your portfolio from inflation and invest in a sector positioned to generate strong real returns, potentially for many years to come. It’s time to take a look at an unloved sector.

© GMO

Read more commentaries by GMO