The Elusive Benefits of “Lite” Annuities

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The growing focus on lower investment fees is affecting longevity-protected solutions (i.e., annuities). This article explores the benefits of annuities with lower explicit fees, a category I dubbed as “annuities Lite” in a previous article that focused on guaranteed lifetime withdrawal benefits (GLWBs).

The growing focus on lower investment fees is affecting longevity-protected solutions (i.e., annuities). This article explores the benefits of annuities with lower explicit fees, a category I dubbed as “annuities Lite” in a previous article that focused on guaranteed lifetime withdrawal benefits (GLWBs).

While lite annuities have attributes that make them seem more seem attractive, in particular lower explicit fees, the elimination (or reduction) of certain features, whose benefits are often complex and difficult to model (e.g., step-up provisions within GLWBs), can significantly reduce the expected income of the strategy, resulting in an illusion of lifetime income protection.

This article demonstrates that lite annuities are effectively “stuck in the middle” between non-annuity investments and more traditional annuity strategies. Their expected income is likely to be notably lower than other products with more generous benefits, while adding relatively little value beyond a pure unprotected strategy.

While fees are an incredibly important consideration when purchasing any product or investment, financial advisors, plan sponsors and retirees should do extra diligence on longevity-protected solutions with reduced income (but potentially lower fees). They are less likely to offer meaningful longevity protection.

Fees… a race to the bottom?

There has been an increased focus on investment expenses in the asset management industry, especially in the defined contribution (DC) space. For example, the asset-weighted expense ratios for target-date funds, the most popular default investment in DC plans, have declined from 67 basis points (bps) in 2009 to 34 bps in 2021, based on data from the Morningstar 2022 Target-Date Landscape Report.

This low-fee focus is spilling into other domains, such as longevity-protected solutions (i.e., annuities), where products have been introduced with lower explicit fees. Those strategies are designed to appeal to fee-conscious investors.

This effect is especially pronounced with annuities which provide GLWBs given the more explicit nature of pricing (e.g., versus single-premium immediate annuities, where the fee is implicit and baked into the payout rate). GLWB lite annuities often have attributes that are similar to more traditional GLWB products, especially the more salient attributes such as payout rates and equity allocations. But they tend to reduce (or eliminate) additional benefits that provide meaningful income to retirees but are harder to quantify, such as step-ups, in exchange for a lower rider (or all-in) fee.

The problem with lite annuities is that they only truly benefit the investor/annuitant if the fundamental purpose of the annuity is not realized, which is providing longevity tail risk. Yes, lower fees may result in a higher residual balance that passes to an heir (e.g., if the annuitant passes away early in retirement); however, if this were to occur, the individual would likely have had more wealth (potentially significantly more wealth) had they not annuitized in the first place.

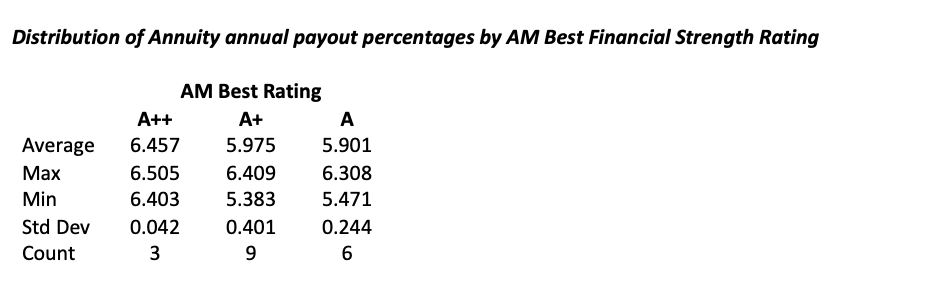

This is not to suggest that just because an annuity has a higher payout means that it’s “better” (context is important). For example, there are notable differences in the payouts in immediate annuities, which are a commoditized product. This effect is demonstrated in the table below, which includes information on annual payout rates for single-premium immediate life-only annuities (SPIAs) for a 65-year old male, obtained from CANNEX on April 29, 2022, and grouped by AM Best financial strength rating.

While there are many factors to consider when assessing the quality of an insurance company beyond its financial strength rating, the table demonstrates that there is a notable variation in payout rates and that it’s possible to get a significantly higher payout from some insurers with higher financial strength ratings. While this isn’t necessarily an entirely “free lunch,” it illustrates that insurers price products differently and that actively searching for the best product can yield more income for clients.

Certain annuities, such as GLWBs, are complex and it is difficult for an investor or advisor to assess the value of the product without a comprehensive analysis. Therefore, providers are incentivized to introduce products that appear to be like existing products based on the salient features but reduce (or eliminate) other features that are less salient, thereby reducing the total cost.

One notable example is the elimination (or reduction in frequency) of the step-provision with GLWBs. With step-ups, if the contract value exceeds the existing income/benefit base at some point (e.g., the contract anniversary date) the income/benefit level will be “stepped up” to the new contract value. This can result in a meaningful benefit to investors in the accumulation and decumulation (i.e., payout) phases. While step-ups have been relatively common among GLWBs, newer products have notably reduced this benefit, for example only offering a step-up at retirement rather than annually during the accumulation phase or even during retirement.

Analysis

To provide additional context around the implications of lite annuities, I conducted an analysis. For the analysis, I assumed a retiree is choosing between two flavors of a GLWB, a “GLWB regular” and a “GLWB lite.” The GLWB regular has a traditional structure with a 5% payout rate (based on income/benefit base), 60% equity allocation, and a 1.6% annual fee applied to the contract value. The GLWB lite has the same initial payout rate (5%), same equity allocation (60%), but only a 1% fee applied to the contract value. However, the assumed step-up for the GLWB lite product is only at retirement.

Let’s look at these two products and focus on the quantitative aspects. They have the same initial payout rate and equity allocation, and since the GLWB lite has a lower fee, it appears to be the better option. While the GLWB lite offers significantly fewer step-ups, this benefit is less salient and its value more difficult to quantify (especially for non-mathletes); therefore, one might naively select the GLWB lite.

Is this the best choice? Let’s explore the options below!

The analysis focuses on a single individual who retires at age 65 and is either age 55 (retiring in 10 years) or age 65 (retiring immediately).

For both cases, the portfolio balance is assumed to be $500,000 with an annual assumed portfolio fee of .5%. The annuity is assumed to be 50% of the total portfolio balance, so $250,000 would be in the respective GLWB and the remainder in the portfolio. The assumed spending need at retirement is $35,000, in today’s dollars, for the 55-year-old and $25,000, in today’s dollars, for the 65-year-old. The spending need is higher for the younger individual because the assets will grow for the 10 years until retirement.

I used Monte Carlo model to simulate future changes in bond yields, which dictate future bond returns. The model targets a 3.5% assumed constant (average) bond yield for the duration of the projection, resulting in approximately a 3.5% bond return and with a 6.0% annual volatility. The return for stocks and inflation is 8.5% and 2.5% respectively, with standard deviations of 18.0% and 1.0%, respectively. The implied correlation among the asset classes is zero. The analysis considers 1,000 runs and ignores taxes. Equity allocations are assumed to evolve based on the Morningstar Moderate Lifetime index.

My analysis focused on the differences in income, balances, and the combined mortality weighted net present values for the respective strategies.

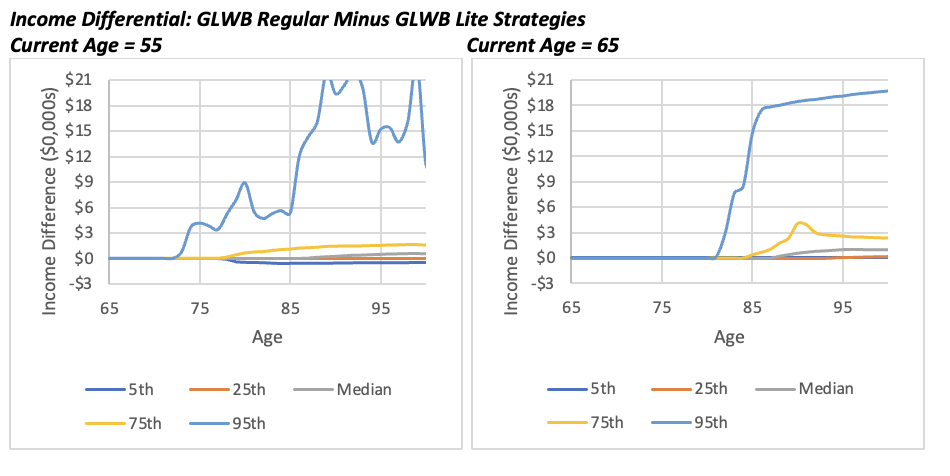

The exhibit below includes information about the income differential between the two approaches (the GLWB regular minus the GLWB lite). If the value in the exhibit is positive, it means the GLWB regular strategy generated more income, and vice versa. The 5th percentile is the worst one in 20 outcomes.

The GLWB regular strategy clearly generated more income than the GLWB lite strategy, which is expected. There are a few instances for the age-55 scenario where the GLWB lite generated more income (where the income difference is negative). This is due to the lower fee for the GLWB lite, which is assumed to step-up to a higher contract value at retirement, but where the GLWB regular never steps up. Clearly, though, a retiree focused on generating lifetime income would favor the GLWB regular over the GLWB lite.

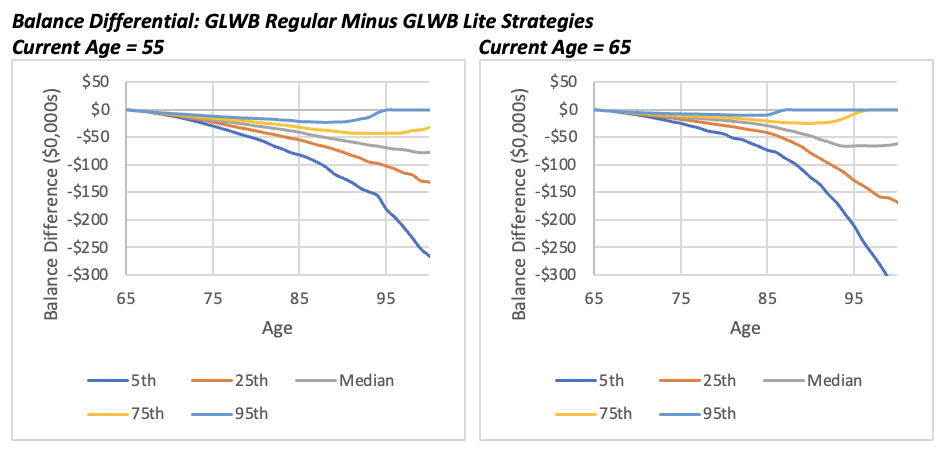

Next, we review the differential in the total balances, which is the total balance from the GLWB regular strategy minus that of the GLWB lite strategy.

While the income differentials for the GLWB regular strategy were positive, as expected, the balances for the GLWB regular strategy are lower than the GLWB lite. This is also expected because the income from the GLWB regular is going to be higher, reducing the balance, and the GLWB regular strategy has higher fees.

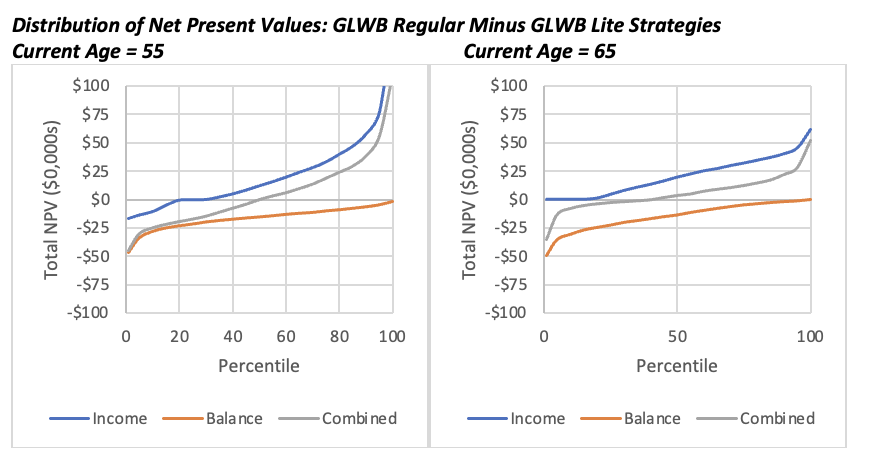

Therefore, to consider the balance more accurately (i.e., to the extent the retiree is concerned about residual wealth upon death) I estimated the mortality weighted net present values (NPV) of income and balances for each run and provide context about the distribution of the income, balances, and combined values (income plus balance) in the following exhibits. For the NPV calculations, the respective values are discounted based on mortality (using the Society of Actuaries 2012 Immediate Annuity Mortality table with improvement to 2022) and a discount rate (based on the assumed risk of the values, i.e., bonds for the income and the portfolio return for the balance).

The median combined NPV for the two products is relatively similar, which is roughly expected. In other words, the expected aggregate value of the products is relatively similar; but the nature of the benefits is vastly different. The GLWB regular dominates based on income, which is typically the primary objective for retirees interested in these products.

A retiree who uses the GLWB as intended, which is for lifetime income, should care significantly more about the income generated from the strategy than the residual balance. In most retirement-income models, the residual wealth that could pass on to an heir is either completely ignored or not deemed as important as the lifetime income. But the above model treats the two components as equal. In other words, while the median combined NPV of the two approaches is similar, the utility from the strategies is vastly different; the GLWB regular dominates the GLWB lite for the vast majority of retirees.

Conclusions

Fees are a salient attribute of any given product or strategy. While lower costs are often viewed favorably in the investment domain, they should be viewed with greater skepticism with respect to longevity-protected solutions (i.e., annuities). Strategies providing protected/guaranteed lifetime income are designed to provide longevity tail-risk protection, but by watering down the effective income benefits, annuity lite strategies offer a benefit illusion of less value to retirees.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an Adjunct Professor of Wealth Management at The American College of Financial Services and a Research Fellow for the Retirement Income Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All