Investor sentiment is telling a mixed story about the market’s ascent since the March low; begging the question, will the skeptics converge with the optimists?

Here in the U.S., I estimate that the actual number of people infected by SARS-CoV-2 to-date is currently just over four times the number of reported cases. Actual cases are undercounted partly because, based on very large-scale, unbiased testing, roughly 45% of people who acquire SARS-CoV-2 infection are asymptomatic.

There is nothing normal about the 2020 recession. Massive nationwide shutdowns of "non-essential" businesses caused real GDP to drop at a 31.4% annual rate in the second quarter, the biggest drop since the 1930s. However, as we expected, a V-shaped recovery is being traced out.

It is a given that you should never mention the “R” word. People immediately assume you mean the end of the world: death, disaster, and destruction. Unfortunately, the Federal Reserve and the Government also believe recessions “are bad.” As such, they have gone to great lengths to avoid them. However, what if “recessions are a good thing,” and we just let them happen?

“Resilience” was this week’s theme as better-than-expected market data came to light. Earnings season has begun, and so far reports have proven the doomsayers wrong. Even industries that have been hardest hit by the economic downturn, including air travel, are expressing optimism that we’re at the “end of the beginning” in terms of recovering from the worst health crisis in 100 years.

We are in a debt trap. Our political process can’t reduce spending and/or raise taxes enough to balance the budget, so the debt grows and grows. As it does, paying the interest plus the accumulated debt load pulls more capital away from more productive uses. This depresses economic growth, thereby generating even more spending and debt.

Actual third-quarter earnings may be less important than what business leaders say about their expectations.

Euro-area countries were struggling to achieve growth and inflation even before the coronavirus pandemic. Now global lockdowns and trade disputes have compounded their problems. Still, we believe euro fixed-income markets offer active investors attractive opportunities and worthwhile income.

I recently did a search of the life and health insurance subsector and came up with 25 names that I considered the highest quality in the overall subsector. All of them carried investment grade credit ratings of BBB+ or better – except for one.

The transition toward a more sustainable energy system presents potential opportunities for investors. We explore what those opportunities are, and identify potential watchpoints.

Passive investing continues to gain share at the expense of active. In doing so, however, it is also substantially increasing systemic risk.

In his latest memo, Howard Marks walks readers through the unusual characteristics of this year’s economy; the impact of Covid-related monetary and fiscal policy actions, including low interest rates, on today’s markets; and the possible ramifications of the Fed/Treasury’s rescue efforts. What does it all mean for investors who face an environment marked by some of the lowest prospective returns in history?

There’s more consensus than usual over the likely winner of the U.S. presidential election. After that, there’s plenty of disagreement on strategies to wager on an election that’s been flashing warnings of chaos ahead in volatility markets.

Asset managers that had been longtime ETF holdouts -- including Wells Fargo, Federated Investors and Dimensional Fund Advisors -- are finally diving in.

It is well-established that “lottery” stocks – those offering the potential for outsized returns, like penny and growth stocks – deliver poor performance. While one might expect that naïve, retail investors are the ones buying those stocks, new research shows that is not the case.

There is currently much hope for another fiscal stimulus package to be delivered to the economy from Congress. While President Trump recently doused hopes of a quick passage, there a demand for more stimulus by both parties. While most hope more stimulus will cure the economy’s ills, it will likely disappoint due to the “2nd derivative effect.”

To some critics, Trump’s behavior and decision-making process may seem erratic, but I believe they make a sort of sense when viewed through the lens of game theory.

Today I want to make some informed speculation about how the next year will unfold. We’re going to reach some key decision points in the coming months and you’ll make better decisions if you think about them before we get there.

We believe now is as good a time as any to do a portfolio assessment. Here’s why investors and their advisors shouldn’t lose sight of how diversification and taxes affect portfolio returns.

The acquisition of the Boston-based firm by Morgan Stanley checks all the boxes.

The beat went on in the third quarter as growth stocks once again shone, propelling the S&P 500 to a 9% gain. The market continues to be narrow, with the index being carried by a relatively small number of companies. While the index is up this year, the average stock is down. This is generally considered to be unhealthy.

President Trump has declared rare earth metals a national emergency and asks that the U.S develop a “commercially viable” mineral supply chain that does not depend on imports from China or elsewhere.

We continue to experience an unprecedented market environment. We were able to again outperform in the third quarter, aided by the significant repositioning we had done in portfolios amidst the sell-off in March. However, we are wary of the risks to the market rally, including elevated valuation multiples...

The pandemic has amplified four long-term macroeconomic disruptors, and fiscal policy – a key swing factor – may hold the key to upside or downside surprises. Read our long-term outlook and learn implications to consider when investing.

As long-time readers know, I tend to be upbeat about the economy and the stock and bond markets, and that has certainly proven to be the correct position to hold over the last 20-30 years.

Wilmington Trust, the wealth-management arm of M&T Bank Corp., is extending its hiring spree and considering acquisitions of RIAs.

If we do not know how to bounce back from failure or hardship, then we may never achieve the success we seek.

If we do a good job of investing in high-quality companies with the potential for strong, long-duration earnings growth, we think starting valuations will matter less in generating attractive long-term performance. When we invest in a company with a high P/E ratio today, we don’t do so with the expectation the ratio will stay high indefinitely.

Rick Rieder and team highlight the critical facts that will drive the markets in the year ahead, as well as the myths that could mislead investors.

U.S. Healthcare Reform Proposals, Childcare Needed to Support Workers, Past U.S. Debt Recovery Won’t Repeat.

The amount of outstanding debt, and the subsequent deficit, has long been a problem in the U.S. For the last two decades, policymakers have made annual promises for more substantial economic growth. Yet with each passing year, growth rates weaken, and economic prosperity worsens.

Investors should try to avoid getting distracted by the feuding political parties within the U.S. A lot of the infighting is being fueled by outside actors, who thrive on the chaos and the division. Russia’s Putin and China’s Xi Jinping are delighted that we’re so divided right now.

I will try to make the case for a much slower recovery thus much higher debt by 2030. Note first, I’m not saying there will be no recovery. I am simply postulating it will look like the slow recovery from the Great Recession, unless the government makes it worse, which is a nontrivial possibility.

While the US economy has been staging a strong recovery from the COVID-19 pandemic, the challenge is far from over, says Franklin Templeton Fixed Income CIO Sonal Desai. She says the tug of war between the virus and the economy seems likely to continue until an effective vaccine is made available at scale.

The fastest, most economically destructive recession is now in investors’ rearview mirrors. CIO Larry Adam shares his perspective on the unfolding recovery.

We believe paying taxes is a scenario where kicking the can down the road can actually be a good thing for taxable investors. Here’s why.

Modern Monetary Theory (MMT) is a rather unconventional economic concept – at least if you are a classically trained economist as I am. That said, over the years, I have learned that, every now and then, it pays to think out of the box, so I am willing to take a closer look.

As economies reopen from COVID-19 lockdowns, there have been fundamental shifts to daily life and work, as well as the investment landscape.

It's a new cycle for the economy, but some asset classes look decidedly late cycle in terms of valuation. What might this mean for markets through the remainder of the year?

The biggest political risk facing investors may be the potential for politicians to implement national lockdowns in response to a rise in new COVID-19 cases that could lead to renewed recession and a new bear market for stocks.

The first of three presidential debates is set for the evening of September 29. The topics, chosen by the Chris Wallace, the moderator, will be the Trump and Biden records, the Supreme Court, COVID-19, the economy, racial tensions, and election integrity.

We have a huge economic calendar and the first of three scheduled Presidential debates. The employment report will be the last one before the election, so I expect it to get special attention. Most of the other important economic data will also be reported during the week.

Ultra-low interest rates and a flood of private equity dollars seeking a decent return have driven the valuations paid in the M&A market to crazy levels, according to two of the most prominent acquirers.

You may have seen headlines questioning whether this is the end of the gold rally. Hardly. Corrections are normal and healthy. During the rally of the 2000s that culminated in gold hitting its previous record high of $1,900, there were several significant pullbacks, some of them exceeding 20 percent.

I’ve warned for several years now that our growing global debt load is unpayable and we will eventually “reorganize” it in what I call The Great Reset. I believe this event is still coming, likely later in this decade. Recent developments suggest it will be even bigger than I expected. You could even say I’ve been too optimistic.

The death of Supreme Court Justice Ruth Bader Ginsburg ignited a fight over her replacement. The increased animosity in Washington lowered the odds that lawmakers will reach agreement on a further fiscal support package and dampened investor sentiment.

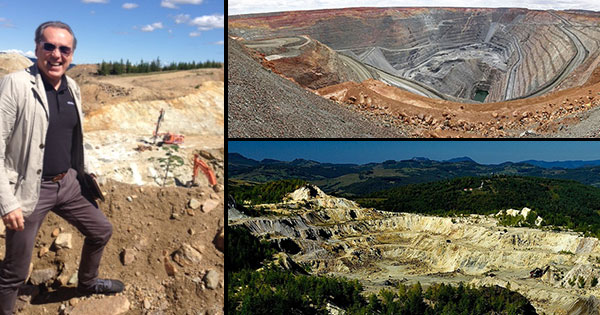

Gold is one of the rarest elements in the world, making up roughly 0.003 parts per million of the earth’s crust. But how much gold is the world digging up each year and what countries produce the most?

Will Danoff has been wondering why billions of dollars keep flowing out of the giant mutual fund he manages. Performance isn’t the problem; demographics appear to be.

The coronavirus pandemic and the response by governments and central banks have family offices and ultra-wealthy individuals around the world on the defensive.

Imagine if you could show your clients the impact of taxes between funds and categories. Now you can. Here’s an exclusive first look at our Tax Impact Comparison Tool.