A clear majority of investors expect a US recession before 2024 is out, leading them to view the current bull market in stocks as ephemeral and to favor long-term US Treasuries.

A fresh fiscal showdown is brewing in Washington that threatens to complicate the Federal Reserve’s policymaking and strengthen Fitch Ratings’ warning that self-inflicted wounds are tarnishing America’s standing in the global economy.

Last week’s sharp moves in the US government bond market have people wondering about the implications not only for the outlook for other financial assets, including stocks but also for the economy and policy.

Research Affiliates explain why their long-term return forecasts have risen across asset classes and the implications of their near-term outlook for U.S. recession.

Bank of England raises interest rates again as expected. Rate hike likely to hurt first-time homebuyers in London. UK gilt curve appears to be pricing in a "higher rates for longer" scenario.

Fitch Ratings unexpectedly downgraded the U.S. credit rating from AAA to AA+, only the second downgrade in U.S. history, citing debt limit standoffs and rising entitlement costs.

The sovereign credit rating cut is unlikely to significantly change views toward U.S. Treasuries, but questions about debt sustainability may grow louder over time.

Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Raymond James CIO Larry Adam examines the reasons for the decision and what the impact may be on the financial markets.

Admittedly, I’ve glossed over the other catalysts in Ackman’s thesis — including the aforementioned supply-demand issues and the fiscal and governance challenges that Fitch underscored in its recent downgrade — but the inflation call seems to be the linchpin to his argument, at least going by the math in the post.

All told it’s hard to get worked up about the near-term implications of the latest downgrade. But it’s telling that one of the most popular defenses of America’s creditworthiness has lost its rhetorical potency.

The mood is rapidly souring in the world’s bond market, raising the stakes for Friday’s much-anticipated US monthly jobs data.

Results from Apple Inc. and Amazon.com Inc. after Thursday’s close represent the next big hurdle for the market’s tech-fueled rally, and it may be the hardest to clear.

No amount of power and prosperity can stop the irritation of getting judged for your borrowing habits, as the world’s biggest economy just experienced.

Signs of falling inflation have helped risk assets recently, but the relief is likely temporary. Volatility may continue in fixed income markets, as high-interest rates continue to weigh on balance sheets and the market digests the probability of a potential recession.

The Bank of Japan announced changes that could allow its yield curve control program to expire gradually if economic conditions are favorable.

The surprise move takes the rating to AA+ from AAA.

As that information presents itself, we may see a fair bit of market choppiness. This is why, even though the market’s monthly moves are fascinating and informative, they are far from instructive for a long-term investor.

The only constant in life is change — and Wall Street strategists trying in vain to divine the stock market’s future. After collectively missing the lion’s share of the year-to-date rally in the S&P 500 Index, the Street’s macro soothsayers appear to be getting modestly more bullish again.

Of all the signs out there that the US will manage to dodge a recession once deemed inevitable, perhaps none is more convincing than this: CEOs across the country are opting to reinvest more of their profits in expansion projects rather than handing the money back to shareholders.

The US Treasury boosted the size of its quarterly bond sales for the first time in 2 1/2 years to help finance a surge in budget deficits so alarming it prompted Fitch Ratings to cut the government’s AAA credit rating a day earlier.

Markets posted a strong first quarter, though it was a rollercoaster ride. The path forward will likely stay turbulent, with bank turmoil likely tightening credit conditions and the Fed still wrestling with inflation.

During the past decade, a turnaround in the Golden State has resulted in higher credit quality for many issuers.

A member of Putnam's Fixed Income team since 2007, Onsel Gulbiten analyzes macroeconomic issues, including inflation, interest rates, and policy developments.

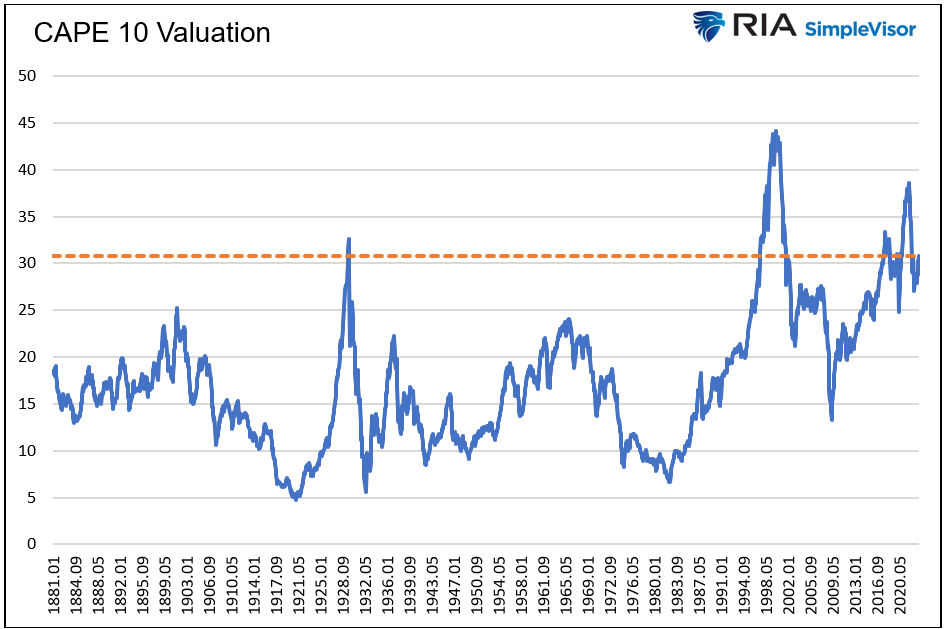

History, analytical rigor, and logic argue that long-term buy-and-hold investors should shift their allocations from stocks toward bonds.

The unexpected downgrade of US government debt sent shockwaves across the economic and political landscapes. In financial markets, the move was met with what amounts to a shrug.

Credit investors are turning more optimistic that the Federal Reserve will pull inflation under control without shoving the US economy into a deep recession.

Energy/oil may have possibly broken out of a range in the low $70s (Brent Crude), which suggests we may have seen a bottom in energy sentiments/stock prices.

While US stocks may pull back in coming weeks amid concern over Federal Reserve policy, the S&P 500 will reassert itself around September before climbing to an all-time high, according to JPMorgan Chase & Co.’s trading desk.

In a quarter filled with talk of potential Treasury default and the second largest bank failure in U.S. history, markets chose to look forward. This was a quarter of AI captivating markets.

Over the past 18 months, high inflation drove rapid monetary policy tightening, which weighed heavily on consumer spending power and corporate margins. As inflationary pressures now abate, we see eventual improvement in both real incomes and profits, which should enhance prospects for multi-asset investors.

Central bank policies are set to diverge from the steady hikes characterizing the first half of 2023, contributing to increased market volatility for the remainder of the year.

The current environment looks favorable for equity market neutral, global macro and insurance-linked securities, according to K2 Advisors. The team offers its mid-year outlook for these and other hedge fund strategies.

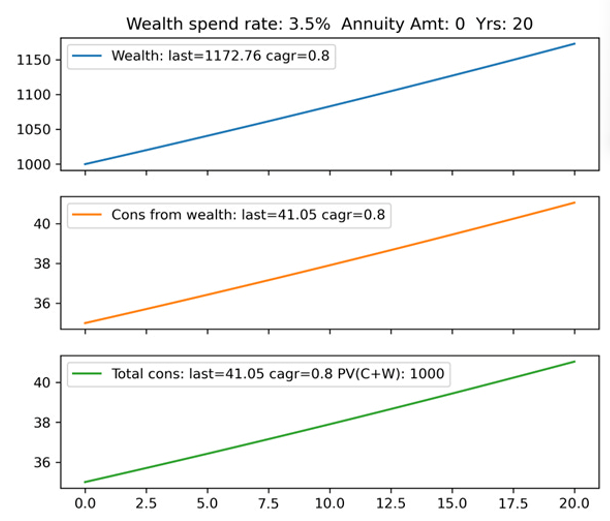

Advisors and investors wonder what role annuities should play in retirement planning. Here are the pros and cons of a common annuity product versus consuming out of invested wealth.

Talk of Goldilocks has taken hold in the markets, and with it the risk-taking allure of not-too-hot and not-too-cold investing conditions.

For stock-picking hedge funds coping with 2023’s loopy markets, risks are starting to outweigh the rewards.

Believe it or not, Emerging Markets (EM) local currency bonds have been outperforming global fixed income asset classes for the past 18-months.

All the chatter back in December was that 2023 was to be the “year of the bond.” And for a brief moment or two in the winter, that call — and the economic doom and gloom that underpinned it — looked right.

Federal Reserve Chair Jerome Powell on Wednesday appeared to give traders the positive signal they’ve been waiting for — that the central bank may finally be wrapping up its steepest interest-rate hikes since the early 1980s.

The Fed continued to signal a "meeting-by-meeting" data-dependent approach to monetary policy. While the June Summary of Economic Projections suggested that there might be one more hike after today's, we think it's also possible that today's hike may be the last one.

Healthcare stocks rank high on our like list, boasting a history of resilience amid both inflation and recession as well as attractive growth prospects thanks to potent innovation. Dr. Erin Xie examines the opportunity.

Solid fundamentals, decent valuations, and attractive income potential make a case for continued exposure to corporate credit even in an uncertain economic environment.

Fresh from the Mining Disrupt conference in Miami, Frank Holmes shares his perspective on a resilient Bitcoin market and the upcoming halving event, amid ongoing debates around the need for regulatory clarity. From an optimistic outlook for a U.S. spot Bitcoin ETF to state-level breakthroughs in Bitcoin mining laws, this account offers a comprehensive glimpse into the evolving digital asset landscape.

Biodiversity is taking on increasing importance as a consumer concern, but it isn’t always top of mind for investors. We think that could soon change. Beyond the obvious environmental benefits, there’s an economic case to be made for protecting biodiversity.

Higher yields for corporate bonds generally correspond to higher credit risk based on an issuer's credit rating.

In this video, Chuck Carnevale, co-founder of FAST Graphs, aka Mr. Valuation, will be sharing with you six incredibly consistent dividend growth stocks that you can invest in today.

The US economy expanded at a 2.4% annual pace in the second quarter, crushing consensus expectations and driving another stake into the 2023 recession narrative.

Municipal exchange-traded funds, still a relatively new and small part of the $4 trillion state and local debt market, have seen growth stall dramatically after record inflows last year as the shift away from mutual funds slowed.

In a unanimous decision, Federal Reserve policymakers raised the federal funds rate to 5.5%, the highest point since 2001.

High-quality investment grade municipal bonds provide growth-like returns for investors in a relatively more conservative investment vehicle than equities. Have your financial advisor assess the opportunity as it pertains to your specific goals.