Bill Ackman’s Treasury Short May Be Right for Wrong Reasons

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLong-dated government bonds are going through a rough patch. Just in the past week or so:

- The Bank of Japan tweaked its yield curve control policy (adding to worries that Japanese money could leave international markets and return home).

- The US Treasury upsized its quarterly bond sales (raising concern that supply would swamp demand).

- The ADP Research Institute’s payrolls report surprised to the upside (suggesting to some that the US labor market was running too hot to tame inflation and that the Federal Reserve might take interest rates higher to rein it in).

- And Fitch Ratings downgraded the US from AAA to AA+ (a move that meant two-thirds of the main rating companies now view the nation as a less-than-sterling credit, although — for a variety of reasons — the conventional wisdom is that this last factor probably moved markets less than the others).

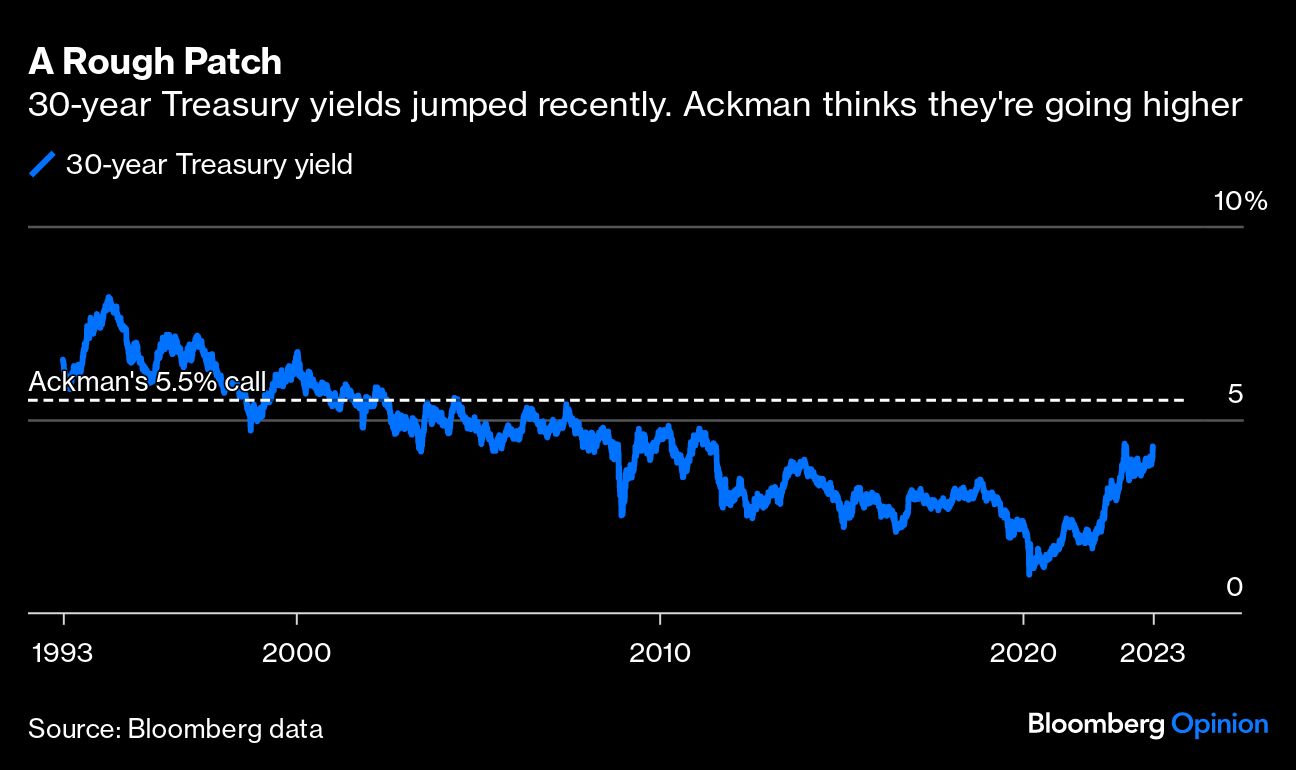

The upshot is that yields on 30-year Treasuries jumped about 29 basis points since Monday and were poised to test their 12-year highs set last October.

Enter Bill Ackman, the hedge fund investor turned social media provocateur, who knows how to seize upon a news cycle for maximum attention and impact. Just as yields were rocketing higher, the Pershing Square Capital Management founder posted on X — the platform formerly known as Twitter that he invested in as part of Elon Musk’s leveraged buyout — that he was using the options market to make what was effectively a short bet on long-dated US bonds.

He lists several drivers — and you should read the whole rationale here — but he seemed to focus on his belief that inflation would remain durably higher than the market now appreciates, driven by factors including “de-globalization, higher defense costs, the energy transition, growing entitlements, and the greater bargaining power of workers.” Here’s the clincher (emphasis mine):

So if long-term inflation is 3% instead of 2% and history holds, then we could see the 30-year T yield = 3% + 0.5% (the real rate) + 2% (term premium) or 5.5%, and it can happen soon. There are many times in history where the bond market reprices the long end of the curve in a matter of weeks, and this seems like one of those times.

That’s why we are short in size the 30-year T — first as a hedge on the impact of higher LT rates on stocks, and second because we believe it is a high probability standalone bet. There are few macro investments that still offer reasonably probable asymmetric payoffs and this is one of them.

If Ackman turns out to be right, it would probably be for the wrong reasons.

The simple fact is that the Federal Reserve has a 2% inflation target and the tools to achieve it. Any long-run forecast above that would hinge on the US central bank losing the will to meet the target, and — for all the chin-stroking that goes on about raising the target by a notch or two — I just don’t see that happening before Ackman’s options expire.

First, doing so now would have consequences for the nation’s inflationary psychology. Having changed the rules in the middle of an inflation fight, the public would come to assume that the bar could be moved again and again. The expectations “anchor” that the Fed has worked so hard to establish since Paul Volcker would be lost, and the consequences would be dire. Policymakers know this, and they won’t let it happen. If the target were ever to be lifted, it could happen only years down the road once the entire episode — and the Ackman trade — had been forgotten.

Second, inflation is improving. Policymakers would never contemplate throwing in the towel on 2% inflation unless new evidence suggested that the costs of the policy were clearly outweighing the benefits. If the process of getting inflation back to a vanity target of 2% ultimately puts millions of people out of work, then economists may understandably conclude that it wasn’t worth it. But that hasn’t happened yet, and no one’s sure how it will play out. In fact, if policymakers have learned anything from the past several months, it’s that the costs of fighting inflation are (so far) quite modest.

Inflation measured by the personal consumption expenditures deflator has plummeted from about 7% last year to 3% now, leaving central bankers surprisingly close to their goal — and with unemployment still at an ultra-low 3.6%. Ackman is right to underscore the potential challenges ahead, and I’d be surprised if the inflation fight doesn’t become more difficult from here on out. But it’d have to get drastically more challenging to shake policymakers’ conviction.

Of course, a part of me says that Ackman is just trying to stir the pot on a social media platform he has a stake in. It’s an instinct that he’s also showcased in his posts about Kyle Rittenhouse, Sam Bankman-Fried and — most recently — longshot Democratic presidential hopeful Robert Kennedy Jr., whose voice Ackman has repeatedly amplified despite Kennedy’s association with the anti-vaccine movement and fringe conspiracy theories.

Ackman calls the long-bond short a “high probability standalone bet”— and boy would I love to know how he defines a low probability one.

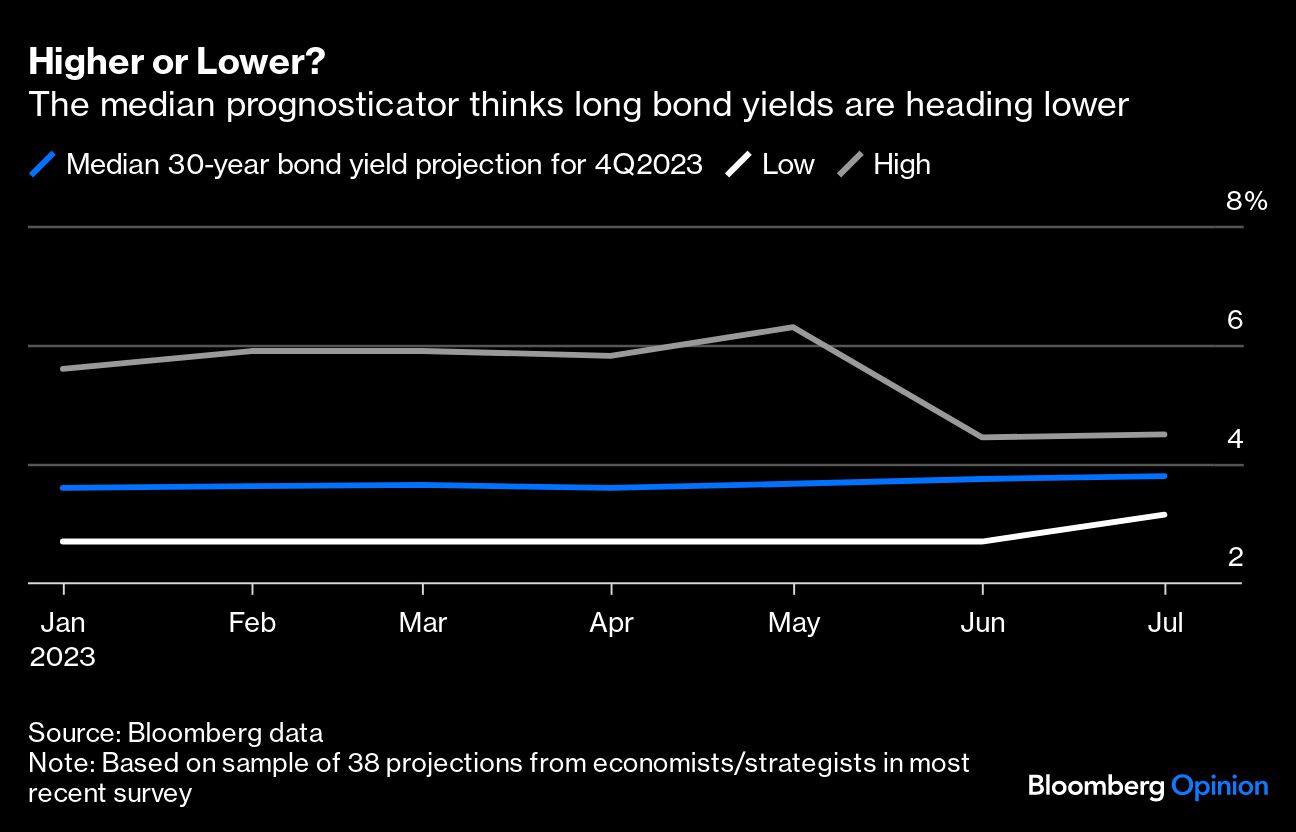

In Bloomberg’s survey of bond strategists, there isn’t one economist or strategist who shares Ackman’s view that the 30-year yield will reach 5.5% at any point before the end of 2025. The next most pessimistic outlook comes from Tom Fullerton, a professor at the University of Texas at El Paso, who thinks it could graze 5% early next year, but the median of the 38 prognosticators in the July survey had the 30-year at about 3.75% at the end of this year. I’m not saying I put a lot of stock in the consensus targets, which have been egregiously wrong recently. (In January 2022, the median forecast put the 30-year yield at 2.48% at the end of the year, and that proved too low by 148 basis points.) But nor do I think Ackman can predict the future more reliably. (See: his failed trades around Herbalife Nutrition Ltd. and Valeant Pharmaceuticals International Inc.)

Admittedly, I’ve glossed over the other catalysts in Ackman’s thesis — including the aforementioned supply-demand issues and the fiscal and governance challenges that Fitch underscored in its recent downgrade — but the inflation call seems to be the linchpin to his argument, at least going by the math in the post. And while bonds have proved volatile and there’s always a chance that he hits his target, it takes a lot of imagination to envision a world in which it will happen in accordance with Ackman’s arithmetic.

A message from Advisor Perspectives and VettaFi: Our latest white papers offer research and analysis covering the most important topics and trends in financial planning, investing, and practice management. Click here to read the top insights from our valued partners.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All