Use This 'Goldilocks Market' to Prepare for Its Eventual End

Talk of Goldilocks has taken hold in the markets, and with it the risk-taking allure of not-too-hot and not-too-cold investing conditions. Just a few weeks ago the market was preparing for two or more hikes and a well-telegraphed recession to prompt the start of a Federal Reserve (Fed) easing cycle in the second half of 2023, but now consensus is rapidly building for no more hikes after July and no recession at all. Two-year and 10-year Treasury yields have retreated some 30 basis points from recent peaks, and stocks have rebounded. “Markets Appear Convinced the Fed Can Pull Off a Soft Landing,” read the headline in the Wall Street Journal on July 16.

Several encouraging developments have helped stoke this rapid change in market perception. The June “miss” in nonfarm payrolls, the first since March 2022, along with the significant downward revisions of prior months, was followed by a weaker-than-expected June Consumer Price Index (CPI) release. The latest reading for the University of Michigan consumer confidence hit its highest level in almost two years, while inflation expectations hit the lowest rate since January 2021. Now, fear of missing out (FOMO) is encouraging more investors to wade even further into risk assets, taking equity price-to-earnings multiples to their highest level since before the Fed delivered its first rate hike of this cycle.

I say not so fast.

Investors may be thinking that the rebound in equity markets is foreshadowing future economic strength, but there are times when the market behaves in a way that is completely uncorrelated with the economy. Often, markets lead or lag economic conditions, but sometimes they chase a hot sector or story. The economy has proven to be resilient despite the Fed’s inflation-quashing efforts, and being overly bearish has not been rewarded. Equity markets have handily outperformed fixed income, with the S&P 500 up nearly 20 percent and the Nasdaq up a whopping 37 percent year to date while the Bloomberg U.S. Aggregate Index and the Bloomberg U.S Investment-Grade Corporate Bond Index are up just 2.5 percent and 3.6 percent, respectively. The artificial intelligence frenzy has boosted valuations of megacap tech and powered equity indexes higher. Part of what started to fuel this rally in mid-March was the Fed’s change of heart about financial conditions when it sought to limit the fallout from regional bank failures, giving market participants the confidence to buy risk without “fighting the Fed.”

Despite this positive market news, the Fed’s roadmap is telling us that the stance of monetary policy will remain tight for some time, suggesting that conditions are due for a change. This may be one of those times when the market and economy are disconnected. Monetary policy works in long and variable lags, and we are only starting to see the lagged effects of 525 basis points of hikes and quantitative tightening. The economy might be on a glide path to a mild recession, but we are seeing many cracks—from the large investment-grade rated U.S. regional bank failures that battered over $5 billion in their corporate debt and preferred securities (which doesn’t count another $17 billion in Credit Suisse’s AT1 bonds), to several large retail companies that went bankrupt when lifelines that had been available in more borrower-friendly periods were no longer available to them, and the numerous occasions where commercial real estate owners have simply handed the keys over to their lenders. Credit trends are getting worse, with rising downgrades, defaults, and bankruptcies, falling recoveries, and higher borrowing costs and debt burdens starting to bite leveraged issuers.

The credit cycle hasn’t even started in earnest. The 12-month default rate in U.S. leveraged credit is only 3 percent and we expect it to peak between 5–7 percent. The full reach of recent commercial real estate stress is unknown so far, but this sector has meaningful links to the banking and insurance industries which themselves play an important role in supplying credit to others. Despite these trends, markets are pricing in a high degree of certainty that everything will be just fine and that the little damage that rate hikes have caused will be isolated to the unlucky few.

As for the Fed, Chairman Powell and his colleagues may be pleased with recent data, but they are not anywhere close to declaring Mission Accomplished. The Fed is going to err on the side of overdoing it and, fearing the inflationary tendencies of a resurgent economy, hiked in July and is likely to do so again in September. Meanwhile, the process of quantitative tightening via a shrinking Fed balance sheet continues at an annualized pace of about $1 trillion (give or take $100 billion), and the Fed has not signaled plans to change that. Quantitative tightening (QT) has not had a significant impact on markets yet. However, the expansion of the balance sheet through quantitative easing helped inflate asset prices, so it makes sense to surmise that asset prices will come under pressure as it shrinks.

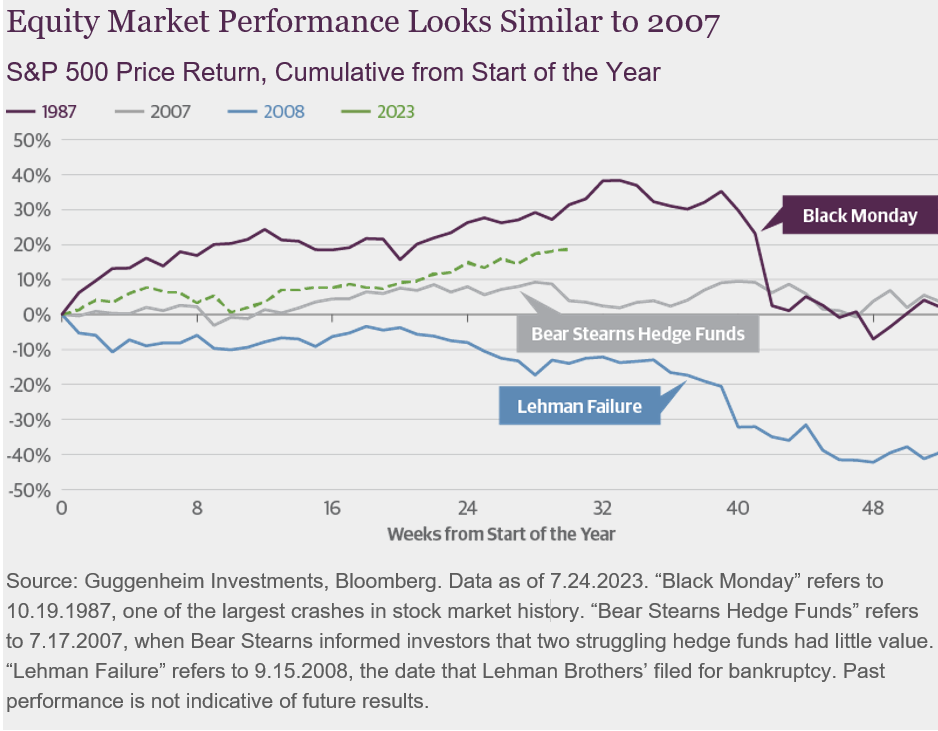

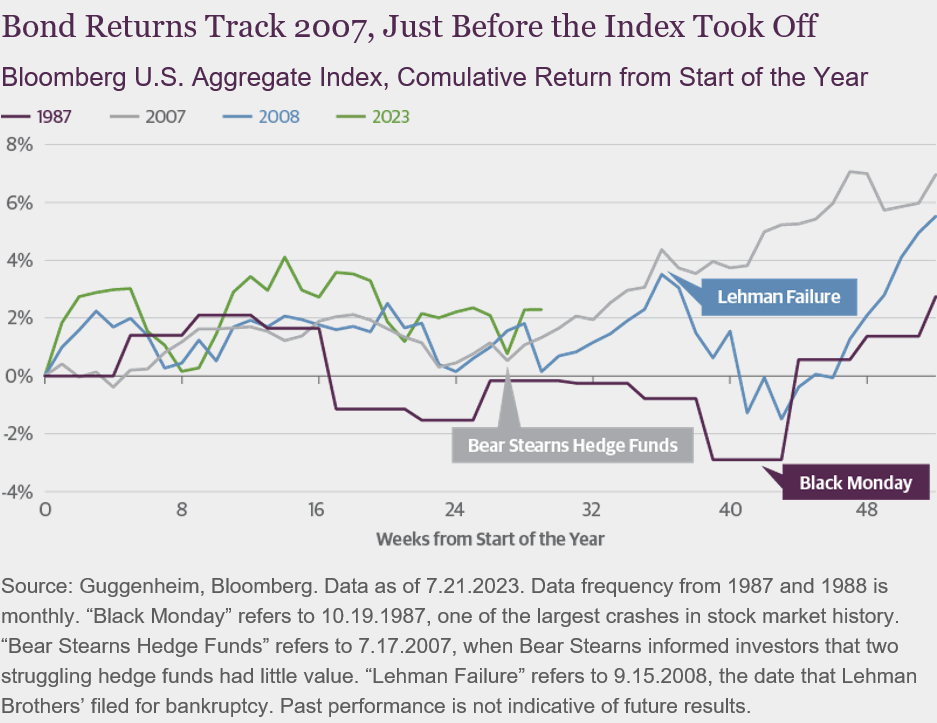

This market backdrop tells me that the current Goldilocks market, like those that came before, won’t last. History shows that this calm before a storm is consistent with some of the worst market drawdowns. Our Macroeconomic and Investment Research Group looked at several to track market performance in the wake of Fed efforts to control overheating. Two that come to mind are the Black Monday stock market crash that occurred in October 1987 and two phases of the Global Financial Crisis (GFC) in 2007 and 2008. The glaring similarity across all of these time periods is the withdrawal of liquidity that preceded them.

Financial Crisis (GFC) in 2007 and 2008. The glaring similarity across all of these time periods is the withdrawal of liquidity that preceded them.

Today’s year-to-date performance in risk assets and Treasury yields looks similar to 2007. Although the integrity of systemically important bank balance sheets and wholesale funding markets is better today than in 2007, there are also some interesting similarities that highlight how long it takes to fully realize the second- and third-order effects of tighter conditions. The Fed concluded two years and 425 basis points of tightening in June 2006, but the largest subprime lender bankruptcy, New Century Financial Corporation, occurred in April 2007. Bear Stearns announced that two of its hedge funds with significant exposure to subprime mortgages had lost all value in July 2007. Meanwhile, equity markets rallied in the first half of 2007 while the Fed was on hold and credit spreads were contained. The Fed’s easing cycle wouldn’t begin until September 2007, and ended in December 2008, before the equity market bottomed.

Equity markets and credit spreads have followed the 2007 path like a stenciled outline. Market participants in 2007 might have thought everything would be okay and that the full impact of policy tightening was behind them after a one-year pause in the hiking cycle, but the long and variable effects of policy extended well beyond that period.

While we are not predicting a GFC-magnitude financial crisis in 2024, mainly because of regulation put in place since then, we believe that the timeline for that recession—and other periods that followed Fed tightening—indicate that tighter conditions take a long time to work through the economy and markets. We are still near an early stage where capital is being rationed as lenders become more selective, bank loan officers continue to tighten lending standards, and primary market issuance declines. Conditions do not seem to warrant the optimism that is fueling equity valuations to these levels. In addition, our seasonality work suggests that most of the 10 percent or more six-month drawdowns in the S&P 500 since 1950 began in August. Large stock market declines—when they occur—tend to happen more often in the second half of the calendar year.

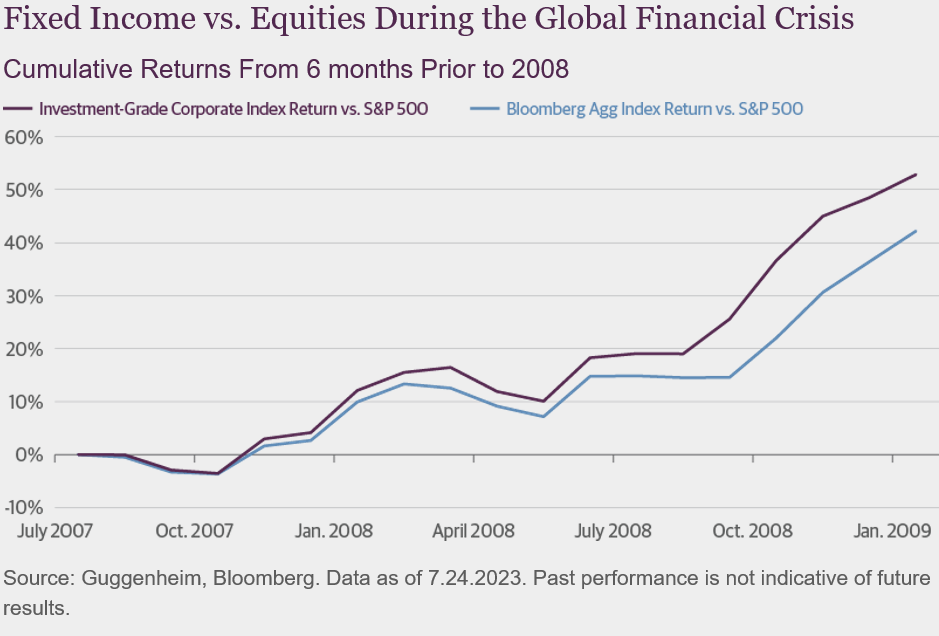

Some asset allocators and investors may be rethinking their relative equity versus fixed-income allocations as they struggle with FOMO. This would be premature. Once Goldilocks conditions end, we believe high quality bonds will outperform equities. The 2007 experience shows that in the 18 months following the Bear Stearns hedge funds collapse, investment grade bonds outperformed stocks by a cumulative 50 percent.

The good news for investors is that this Goldilocks period may persist in the short term, which means there is still time to take appropriate portfolio measures. Taking cues from history, we remain defensive and have been reducing high beta exposure and using market strength to increase allocations to high quality credit. In high yield, we are implementing a more defensive approach by going up in the capital stack and obtaining stronger investor protections. But we do not believe that we are sacrificing yield in the process. Investment-grade corporate bond yields remain attractive at over 5 percent. In structured credit, we can obtain even higher yields with solid structural protections—supported by the historically lower default rates in asset-backed securities and collateralized loan obligations—when compared to corporate bonds of similar ratings. These sectors have delivered steady returns in the first half of this year. As we near the end of the hiking cycle, the stability in rates will result in steady coupon returns, as many subsectors have exhibited over the first half of 2023. A decline in rates as the economy slows could support performance further in 2024.

The swimming is fine while the waters appear calm, but we expect it won’t last. Investors should consider preparing for it now, otherwise, as Warren Buffett famously said, we will see who is swimming naked when the tide rolls out.

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal. Investments in fixed-income instruments are subject to the possibility that interest rates could rise, causing their values to decline. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners or its subsidiaries. The opinions contained herein are subject to change without notice. Forward-looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Partners Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

©2023, Guggenheim Partners, LLC. All Rights Reserved. No part of this document may be reproduced, stored, or transmitted by any means without the express written consent of Guggenheim Partners, LLC.

GPIM 58135