Today, Vanguard decided to join the target-maturity party, launching a suite of corporate bond ETFs designed to assist investors with bond laddering. Vanguard’s entry is significant due to its massive distribution scale in tandem with its low-cost reputation.

Heavily influenced by escalating geopolitical conflicts, last week's economic snapshot reveals a sharp erosion of confidence among consumers and investors alike.

The conflict in the Middle East remained a key driver of market sentiment this week, with rapidly shifting headlines contributing to heightened volatility.

For investors who understand this distinction, the current pullback may represent an opportunity rather than a warning. Short-term sentiment may dominate headlines, but long-term fundamentals continue to point in a very different direction.

In today’s era of automation, some situations demand a more active approach. Municipal bond investing is one.

Rapid advances in artificial intelligence, persistent geopolitical tensions – particularly the conflict in Iran – and ongoing trade uncertainty have kept headlines loud and emotions elevated, ultimately demanding investors remain adaptive and disciplined. In this kind of environment, the biggest mistakes come from reacting to noise rather than fundamentals.

Many people forget that gold was in a bull market in early 2008 but suffered a significant selloff at the onset of the financial crisis when the yellow metal fell 32 percent, giving up about 40 percent of its previous bull market gain. Gold then took off and soared by over 153 percent over the next few years.

Bearish sentiment has taken over the markets. As one analyst put it, “Wall Street has thrown in the towel on gold.”

In a world of intensified uncertainty and dispersion, investing becomes less about forecasting and more about favoring more liquid, high quality assets that can be resilient across a variety of scenarios.

The multi-asset playing field presents income investors with broad opportunities across asset classes. But investors that rely only on traditional stock dividends and bond interest may be missing out on other attractive income sources.

As portfolios limited to public equities capture a smaller slice of corporate growth, private investments are increasingly finding a place in long-term wealth-building strategies, including 401(k)s.

A rush by bond traders to unwind US futures positions amid the selloff triggered by war in Iran is running its course, setting the stage for new wagers that will determine whether the rout reverses or deepens.

The Fed’s decision made sense: don’t change the target for short-term interest rates if we don’t know what the world will look like tomorrow. But investors need to remember a couple of important things. Rate cuts, if they ever come, are less important than the money supply.

Geopolitical headlines rarely arrive quietly. The recent escalation in the Middle East is a reminder of how quickly tensions can feel destabilizing.

Stocks fell for the fourth consecutive week as rising interest rates and surging oil prices—driven by the ongoing conflict in the Middle East—continued to weigh on investor sentiment.

Uncertainty persists in 2026, affecting the broader fixed income market. Collateralized loan obligations (or CLO) have emerged as a viable option with the advent of exchange-traded funds (ETFs), which have democratized access to retail investors.

Corporate credit markets have become unsettled about the potential for advanced agentic AI tools from firms such as Anthropic and OpenAI to automate functions across legal, analytical, marketing, and sales workflows, effectively targeting the software as a service (SaaS)/enterprise software space.

Gold steadied after a dramatic selloff that has pushed the metal down more than 15% since the start of the Middle East conflict.

While agricultural best practices have moved on to other resources, the Guano Wars teach us that nations are willing to go to great lengths to sustain their crops.

Faster productivity growth lifts earnings, improves the long-run fiscal arithmetic, and allows the economy to run stronger without recreating the inflation regime of 2022. Historically, markets are slow to recognize when the supply side of the economy has improved. This time should be no different. The productivity story is more durable than this week’s Iran developments, which is dominate trading over the near term.

Since hostilities began in the Middle East three weeks ago, I’ve urged investors to stay calm and resist the temptation to panic-sell. While I still stand by that advice, it’s important to point out that this conflict isn’t resolving as quickly as initially expected.

With liquidity and credit stress in the private credit market rising, we must consider whether the Fed might once again ignore its mandates to backstop exuberant markets.

The artificial intelligence (AI) trade that has dominated equity markets in recent years is showing signs of fragility. As investors reexamine the scale of the AI infrastructure build-out and optimistic assumptions around AI adoption, a group of “old-economy” sectors is quietly reasserting itself.

In February, market sentiment was shaped by escalating US-Iran geopolitical tensions and sector-specific selloffs driven by concerns about AI’s potential disruption to existing business models.

Jeffrey Sherman of DoubleLine provided a candid assessment of the Federal Reserve's current trajectory and fixed income at Exchange.

Modern markets have gotten used to central bank support whenever the global economy wobbles. But as the world confronts a fresh energy shock unfolding against brittle labor markets, investors need to prepare themselves for the possibility that central bankers won’t have their backs — quite the opposite.

The past three weeks have been unsettling, and not just for markets, but for anyone paying attention to what is happening in the world.

Global markets stood on edge as the conflict in Iran upended energy markets and muddied the outlook for the global economy. Interest rate markets repriced as market participants processed the notion that hostilities and the closure of the Strait of Hormuz could last longer than expected.

The Cboe Crude Oil ETF Volatility Index (OVX), which measures implied volatility in oil ETF options, estimates the expected volatility of crude oil prices over the next 30 days. The higher the reading, the more oil prices are expected to bounce around.

A properly functioning Strait of Hormuz holds the keys to clarity around the growth, inflation, and market shock that has stemmed from the war in the Middle East.

Private credit is a key pillar of debt capital formation alongside public credit markets and bank balance sheets. But an important part of its value proposition—to borrowers and end investors—is its illiquidity relative to public markets. That distinction is by design, and we think it should stay that way.

Historically, major geopolitical or economic crises, such as the war against Iran, have prompted investors to sell riskier assets and buy “safe-haven” investments whose values were expected to remain stable or even rise amid the disruptions.

Federal Reserve officials left interest rates unchanged and continued to expect one rate cut this year as they acknowledged increased uncertainty due to war in the Middle East.

In this commentary, I’m not going to try to predict any outcomes or long-term effects but rather want to cover how markets have reacted so far and highlight some opportunities that have been created.

Comparing business-cycle-related primary trends of the falling 2-year Treasury yield shows that this is the slowest business cycle since WWII. I argue the slowness of this cycle is evidence of the 6+% average pro-cyclical fiscal deficit over the last three and a half years.

Morgan Stanley is sticking with a forecast that sees the Federal Reserve resuming interest rates cuts in June and delivering another reduction in September, even as soaring oil prices prompt traders to curb bets for how much policymakers will lower borrowing costs this year.

The word 'equilibrium' is an invitation to recognize that nothing exists by itself, alone. Subject and object are two sides of the same coin – their interaction is a single phenomenon. That perspective can offer a great deal of insight about economics, financial markets, speculative bubbles, passive investing, and nearly everything in existence.

Iran-related geopolitical risk has boosted stock volatility, especially in sectors like Energy. Uncertainty remains high and there are a range of scenarios for how this conflict could be resolved and how it might affect economic conditions and markets.

This past weekend, Adam Taggart and I discussed what happens to Treasury bond yields when the United States enters a military conflict. The conventional wisdom is reflexive and tidy.

When geopolitical tensions flare up, the natural assumption is that gold should immediately surge. War breaks out, markets panic… and the metal rallies as investors rush to safety.

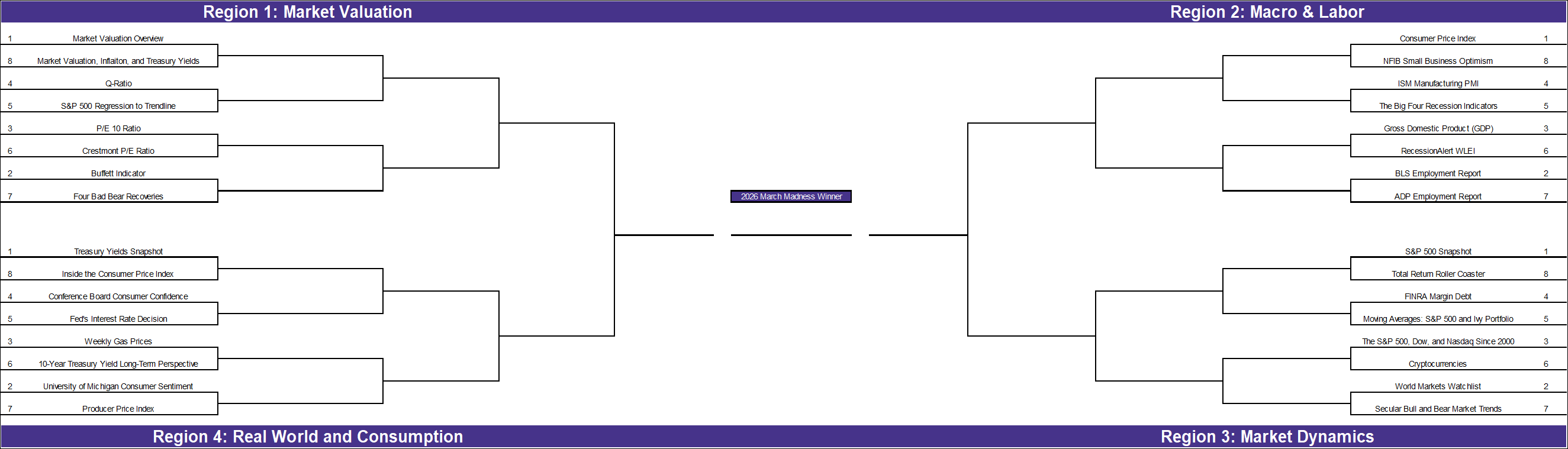

With the NCAA tournament beginning in just a few days, we’ve applied the bracket format to our own research. While economic theory often dictates what should be most important to investors, our reader engagement reveals which topics truly commanded investor attention over the past year.

In our recent article, "The Value Rotation Illusion," we explained that in the recent rotation from growth to value. In this follow-up, we take the three-tier earnings valuation framework we introduced in the previous article a step further to uncover true value stocks.

One of the things I enjoy most about producing videos and educational content is the thoughtful feedback and questions from viewers. Often, the comments themselves highlight areas where investors are seeking a deeper understanding of value investing principles.

A surprise 92k decline in February nonfarm payrolls and a rise in the unemployment rate to 4.4% signal some labor market softening, though stronger ISM manufacturing and services readings and still-low jobless claims suggest the broader U.S. growth backdrop remains intact.

Volatility in US Treasuries jumped to a nine-month high as the Iran war fanned inflation concerns and upended traders’ expectations on the Federal Reserve’s policy path.

European stocks rose Friday as oil prices slipped below $100 a barrel, following news reports of an Indian tanker’s passage from the Strait of Hormuz, a key shipping artery that’s been effectively shut amid the Iran war.

A healthy mix of income and growth potential may yield a more effective equity allocation.

Volatility spiked as investors questioned the Federal Reserve's next move, adding to existing concerns about private credit markets. Here's why investors shouldn't overreact.

State Street Investment Management is continuing its push into the intersection of public and private credit with the launch of a new ETF.

The military conflict in Iran and the Middle East is curtailing the global flow of oil and natural gas. This adds notable pressure to energy prices and the near-term inflation outlook, while also raising questions about countries’ reliance on energy imports and their economic resilience.