While the S&P 500's all-time high hasn't been accompanied by other parts of the market (notably, small caps), further gains are possible if breadth firms up.

Bank loan income may decline if the Federal Reserve cuts interest rates. That doesn't mean investors should avoid them altogether, but it's important to understand the risks.

Investor sentiment toward China has soured after a tough year for the economy and stock market. But the painful economic transition is also creating real opportunity.

Treasury yields have steadily climbed since the start of the year, with the 10-year Treasury yield rising back to 4.16% after reaching a low of 3.79% in late December.

This year is already shaping up to be a tough one for investors to navigate, with heightened debate over central bank moves, prospects for economic slowdowns and crucial elections around the world all weighing on fund managers’ minds.

Institutional investors may want to consider an allocation to Quality equities as well as a sufficient allocation to government bonds.

While capital markets are expecting rate cuts to come this year, the pace at which they occur and when certainly comes into question. While the Fed continues to mull rates, fixed income investors can consider three specific ETFs from Vanguard to get more yield.

After two years of fighting inflation amid fears of recession, markets and policy makers appear unified in their sanguine outlook. While interest rate increases designed to slow economies may well be nearing an end, markets are never without risk.

Rate cuts don’t happen in a vacuum—staying nimble with asset allocation can help investors adapt.

Stronger-than-expected growth, concerns about the U.S. government's fiscal outlook and the Federal Reserve's (Fed's) pledge to keep interest rates higher for longer drove yields to levels not seen in decades.

Treasury yields rose on Wednesday following stronger-than-expected retail sales and encouraging remarks from a Federal Reserve member.

A sense of torpor that’s descended on Wall Street’s chief fear gauge since the fall is starting to disappear.

Still doing “T-bill and chill”? As a strategy, rolling Treasury bills may have worked well so far this year, but history suggests it’s time for municipal bond investors to get off the sidelines and back into the market—and soon.

Citigroup Inc.’s option volume was light on a recent Wednesday, until the session’s last 90 minutes when a wave of trades hit. These weren’t bets on the shares moving — rather, they were part of a long-dormant strategy that’s back in vogue thanks to the Federal Reserve’s interest rate hikes.

Bond traders are growing convinced that US Treasury yields are on the brink of returning to the way they’ve traded for most of their existence — it’s the how, why and when of the normalization that keeps financial markets bouncing around.

We did an internal survey among our associates, attempting to get a feel for their views on various economic and fixed income topics. Any survey result concerning the future can net inexact results but nonetheless reveal general sentiment. Attitude, outlook, and opinions can help shape the market.

Emerging markets bonds issuance is already reaching record highs early in 2024. The Financial Times reported that EM debt issuance is already at $50 billion, opening opportunities in EM bond ETFs.

Bond traders abandoned wagers that the Federal Reserve will cut interest rates in March, pushing swap rates to levels consistent with only about 50% odds of a quarter-point reduction in the federal funds target during the first quarter.

Fast-money bears are feasting in the new-year equity selloff as traders recalibrate bets on the path of Federal Reserve policy.

Economic data has provided encouragement for both stock market bulls and bears.

The market has taken a one-sided view on inflation and the Fed's reaction to it, even though other very plausible explanations exist. This illustrates both the power of narrative and the vulnerability of the current consensus.

Digital events are more environmentally friendly than in person ones, but did you know that studies show that marketing webinars generate as much as five times more qualified leads than the same budget spent on marketing seminars?

Wall Street corporate bond desks are seeing a major increase in demand for hedges as debt issuers grapple with soaring interest-rate volatility.

Federal Reserve Governor Christopher Waller said the US central bank should take a cautious and systematic approach when it begins cutting interest rates, a process that can start this year absent a rebound in inflation.

After sidestepping last year’s scorching stock rally on concern about higher interest rates, Wall Street’s top forecasters can’t get bullish fast enough amid expectations for cuts by mid-year.

Bond traders are growing more convinced that US yields are heading lower as they bet on a series of Federal Reserve interest-rate cuts, yet the path to cheaper borrowing costs is set to be extremely bumpy.

Municipals experienced their strongest two-month performance since 1986 during the final two months of 2023.

Today’s “finance-based” global economies are moving in the wrong direction.

With the Federal Reserve poised to begin cutting interest rates this year, the dollar may drift generally downward. However, its performance against individual currencies may vary widely.

Beware of investing in cash with a plan to extend maturities when the yield curve is no longer inverted. My research shows that this decision is historically difficult to time.

Corporate bonds delivered solid gains last year. And market observers expect more of the same in 2024. But it’s important to note that the consensus is leaning toward investment-grade over junk-rated corporate issues.

Soaring borrowing costs and plunging prices walloped the global commercial-property market last year. Now, more clarity around values and an urgent need to address looming debt maturities are expected to spark more deals.

The January effect, named for the market anomaly where stock returns in January are typically higher than in other months, has been a subject of interest since it was first documented in 1942.

Risk assets surged to end 2023 as the Federal Reserve blessed market hopes for rate cuts. That momentum could persist for some time as inflation cools.

Bond traders shrugged off higher-than-anticipated inflation readings for December, pricing in a larger total amount of Federal Reserve interest-rate cuts this year beginning in May.

Earnings season starts Friday as major investment banks report, and the focus is on rates.

In this article, Russ Koesterich discusses why equity performance in 2024 may be more muted and warrant more focused positioning across segments of the market.

We see both advantages and disadvantages to IBM's retirement program changes. One advantage is that more capital will be freed up for other corporate initiatives, while one disadvantage is that without a 401(k) match, participants may save less for retirement.

On this episode of the “ETF of the Week” podcast, Tom Lydon discussed the PIMCO Enhanced Short Maturity Active ETF (MINT) with Chuck Jaffe of “Money Life.” The pair talked about several topics regarding the fund to give investors a deeper understanding of the ETF overall.

The Federal Reserve won’t want a repeat of 2023 where 10-year Treasury yields soared from a low of 3.3% in April to peak at 5% in October — only to plummet back to 3.8% by year-end.

US inflation accelerated in December as Americans paid more for housing and driving, challenging investor bets that the Federal Reserve will cut interest rates soon.

Roaring inflation and rapid rate hikes have brought a welcome return of the kind of big swings and dislocations beloved by investing’s smart set, but it hasn’t been a blessing for every breed of quant.

In this video, Chuck Carnevale, Co-Founder of FAST Graphs, a.k.a. Mr. Valuation, discusses the potential for real estate investment trusts (REITs) in 2024. He analyzes the performance of various REITs, focusing on dividend yields, operating cash flow, and FFO growth.

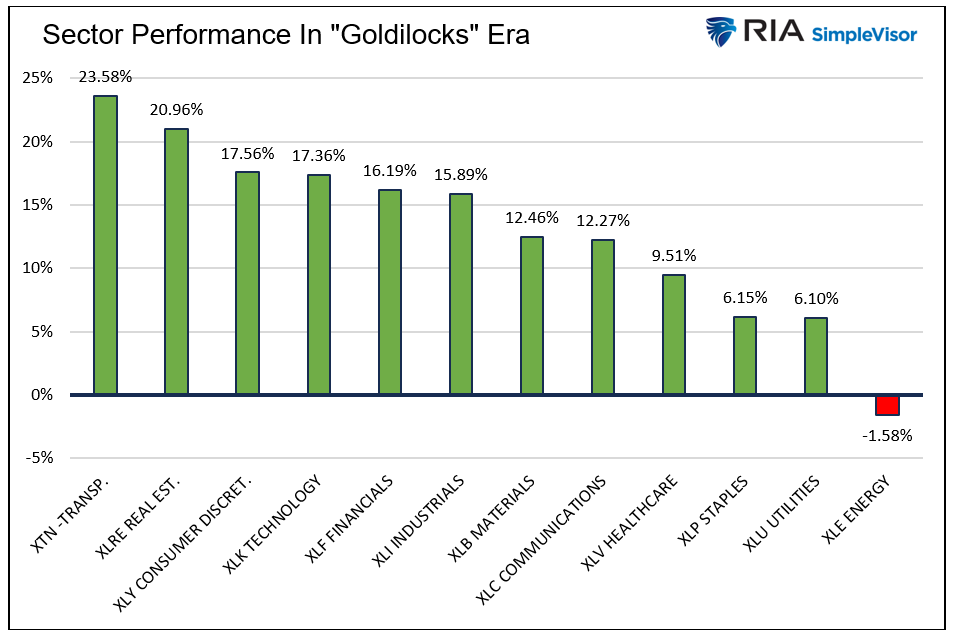

Today's popular narrative is a growing consensus for the Fed to engineer a soft landing and a “Goldilocks” economy.

Advisor Perspectives has announced its Venerated Voices™ awards for commentaries published in 2023.

Right around the start of November, two words suddenly disappeared from the chatter in the bond market: debt supply.

The 60/40 portfolio has long been the foundation of portfolio construction. But over the past two years, this portfolio strategy has broken down. The 60/40 portfolio faces several challenges. To understand what might lie ahead, investors need to assess both recent inflationary forces and historic trends.

The Federal Reserve (Fed) left the door so wide open after the end of the Federal Open Market Committee (FOMC) meeting in mid-December 2023, that markets have run ahead and have continued to push long-term rates lower since the decision was announced.

In December 2022, I published Sea Change, a memo that primarily discussed the 13-year period from the end of 2008, when the U.S. Federal Reserve cut the fed funds rate to zero to counter the effects of the Global Financial Crisis, to the end of 2021, when the Fed abandoned the idea that inflation was transitory and readied what turned out to be a rapid-fire succession of interest rate increases.

A record amount of zero-coupon bonds were created in December as investors scrambled to lock in US government bond yields that were retreating from multiyear highs.