Election Year Suggests a More Subdued ‘24

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn this article, Russ Koesterich discusses why equity performance in 2024 may be more muted and warrant more focused positioning across segments of the market.

Key takeaways

- Just as 2023 market returns proved to align with seasonal patterns, there was another underlying factor that impacted performance, the political cycle.

- Since 1926, year three of the election cycle has proven to be the strongest – with a median return that is double the average of the other three years.

- With 2024 being an election year, these patterns are worth consideration. While one small part of the broader outlook, history suggests more muted equity performance.

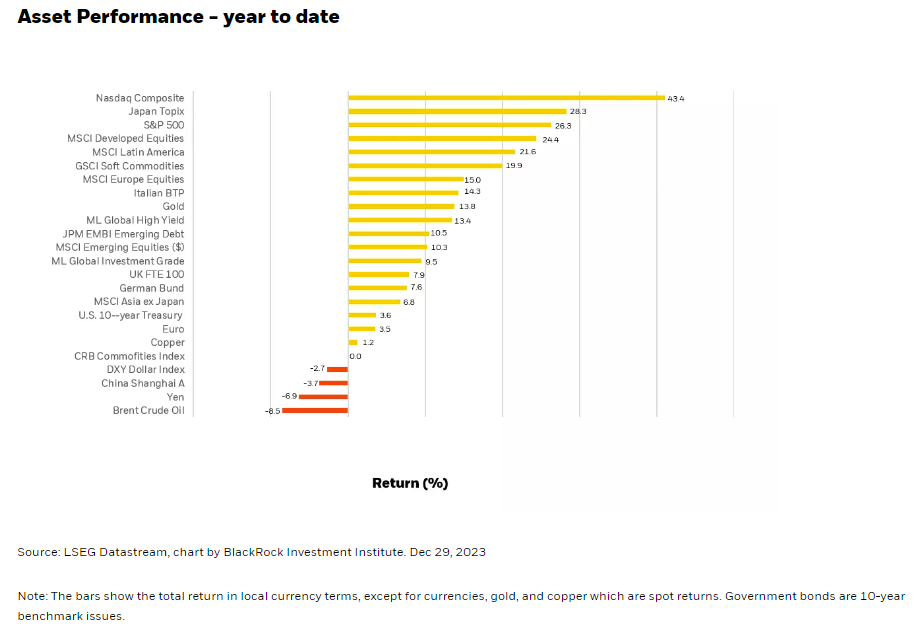

Last January, I authored a piece that discussed the tendency for market performance following a down year (2022), to be either very good or very bad, but rarely average, with the biggest source of variation being inflation. Performance in 2023 has conformed to historical trends with the S&P 500 up over +25% through year-end and the tech-heavy NASDAQ Composite +43%. In addition, while seasonal effects on stock markets can be often overstated, 2023 reminded investors why it’s worth paying some attention to the calendar. Stocks rallied in January, corrected in late summer, before rallying strongly in November. 2023 returns have mostly confirmed both historical tendencies and seasonal patterns.

There is another, longer-cycle that investors also watch: the election cycle. As with seasonality, the impact can be exaggerated. But while rarely the biggest factor in driving returns, with an election year approaching it is worth revisiting how stock returns correlate with the political cycle.

3rd Year a Charm

Despite the frequent reversals and shifts in the investment narrative throughout 2023, equities had a stellar year. U.S. large caps have returned 26%, while the Nasdaq is up by more than 43% (see Chart 1). Just as last year’s trading has generally conformed to seasonal trends, a strong 3rd year of the election cycle is also consistent with historical patterns.

Using the Dow Industrials - admittedly not the broadest index but the one with a suitably long track record - suggests a few patterns. The most pronounced of which is equity market strength in the third year of the cycle. Since 1926, the average price return in year three has been 12.50%, with a median return of more than 15%. This is double the average of the other three years. The higher average reflects the fact that third years rarely produce negative returns.

While it is not clear what drives the cycle, one theory has been tied to the economy. Re-election, either for the sitting President or their party, is more likely with strong growth. This suggests a tailwind from any fiscal stimulus, often delivered a year or more before the next election.

Across the GA Selects Model Offering, positioning is shaped by macro regime identification that informs top-down allocation and considers a variety of factors. While the past is not always prologue, things like policy and the election cycle does merit consideration when making measured bets in your asset allocation. For most of 2023, our model offerings have had “risk on” bias across risk profiles, which has served investors well.

A more muted 2024?

It's not obvious that this aggressive risk taking will continue into next year. Since bottoming in late October, equity markets surged more than 16% through year-end. The rally has been led by higher beta, lower quality names. This is consistent with seasonal patterns, but perhaps more importantly with a rapid easing in financial conditions. Investors have responded to a plunge in real, or inflation adjusted bond yields.

It's not obvious that this aggressive risk taking will continue into next years. Assuming a soft-landing, further declines in bond yields may be harder to come by. This does not suggest another correction, merely that the recent risk-led rally probably comes with an expiration date.

And while the election cycle is only one small part of the broader outlook, history also suggests more muted market moves. Returns in the last year of an election cycle are typically modest. Returns average a little over 4%, with the median around 7%. More muted returns are also reflected in less volatility and a lower standard deviation of returns. In other words, the election cycle suggests less drama after two years of more extreme performance. This suggests staying long stocks but pulling back a bit on the riskiest bets for 2024.

Russ Koesterich, CFA, is a Portfolio Manager for BlackRock's Global Allocation Fund and Lead Portfolio Manager for BlackRock’s Global Allocation (GA) Selects Model Portfolios and is a regular contributor to Market Insights.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of January 2024 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

The BlackRock Model Portfolios are provided for illustrative and educational purposes only, do not constitute research, investment advice or a fiduciary investment recommendation from BlackRock to any client of a third party financial advisor (each, a "Financial Advisor"), and are intended for use only by such Financial Advisor as a resource to help build a portfolio or as an input in the development of investment advice from such Financial Advisor to its own clients and shall not be the sole or primary basis for such Financial Advisor’s recommendation and/or decision. Such Financial Advisors are responsible for making their own independent fiduciary judgment as to how to use the BlackRock Model Portfolios and/or whether to implement any trades for their clients. BlackRock does not have investment discretion over, or place trade orders for, any portfolios or accounts derived from the BlackRock Model Portfolios. BlackRock is not responsible for determining the appropriateness or suitability of the BlackRock Model Portfolios or any of the securities included therein for any client of a Financial Advisor. Information and other marketing materials provided by BlackRock concerning the BlackRock Model Portfolios –including holdings, performance, and other characteristics –may vary materially from any portfolios or accounts derived from the BlackRock Model Portfolios. Any performance shown for the BlackRock Model Portfolios does not include brokerage fees, commissions, or any overlay fee for portfolio management, which would further reduce returns. There is no guarantee that any investment strategy will be successful or achieve any particular level of results. The BlackRock Model Portfolios themselves are not funds. The BlackRock Model Portfolios, allocations, and data are subject to change.

For financial professionals: BlackRock’s role is limited to providing you or your firm (collectively, the “Advisor”) with non-discretionary investment advice in the form of model portfolios in connection with its management of its clients’ accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of the Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for a client’s account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein for any of the Advisor’s clients. BlackRock does not place trade orders for any of the Advisor’s clients’ account(s). Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics–may not be indicative of a client’s actual experience from an account managed in accordance with the strategy.

For investors: BlackRock’s role is limited to providing your Advisor with non-discretionary investment advice in the form of model portfolios in connection with its management of its clients’ accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of your Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for your account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein. BlackRock does not place trade orders for any Managed Portfolio Strategy account. Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics—may not be indicative of a client’s actual experience from an account managed in accordance with the strategy. This material is subject to change.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2024 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: The crypto landscape is on the brink of a revolution. Are you prepared for what's coming in 2024? Dive into expert insights on the future of crypto and its influence on next year's market. Join us at the Crypto Symposium on January 12th at 11 am ET. Click here to register.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All