Wall Street corporate bond desks are seeing a major increase in demand for hedges as debt issuers grapple with soaring interest-rate volatility.

Six leading bond underwriters — Bank of America Corp., JPMorgan Chase & Co., Goldman Sachs Group Inc., HSBC Holdings Plc, Mizuho Financial Group Inc. and MUFG Bank Ltd. — are all seeing elevated appetite from companies to tap pre-issuance hedges, or products that allow them to lock in a portion of their borrowing costs ahead of time, according to interviews and people familiar with the matter.

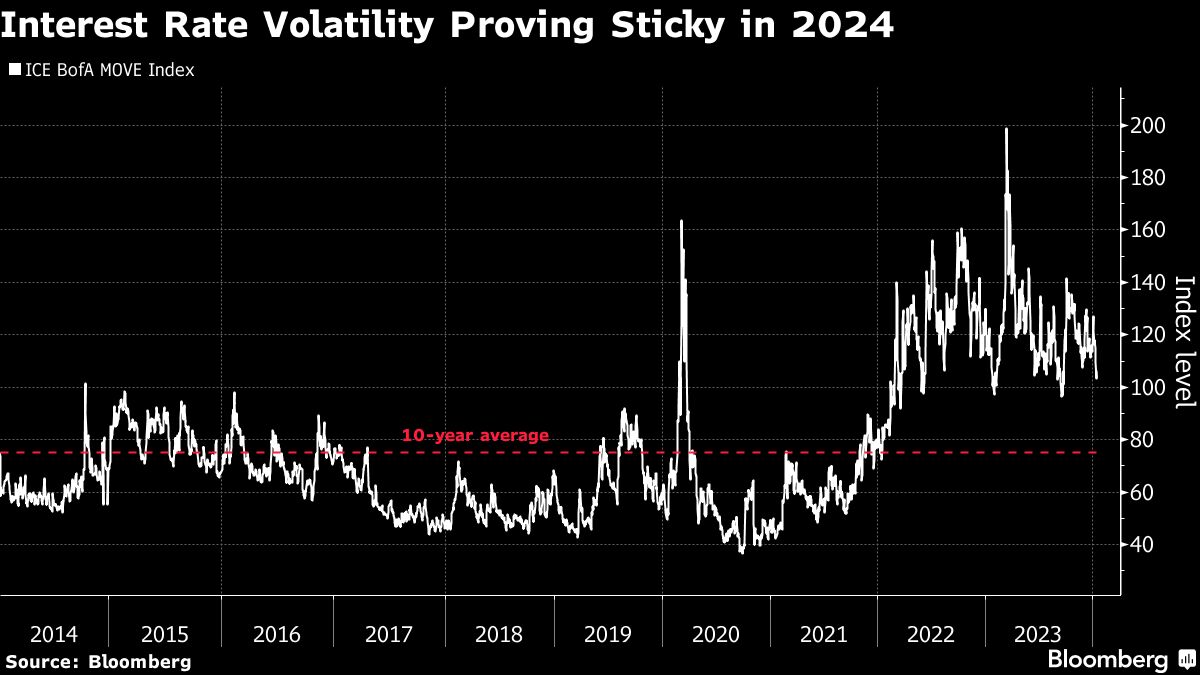

They’ve become all the more appealing after a roller-coaster ride for Treasuries in recent months, which saw yields on 10-year notes rise above 5% in October, plunge to nearly 3.75% in December and end last week around 3.94%. The ICE BofA MOVE Index, which measures volatility in interest-rate swaps, this month is running more than 50% higher than its 10-year average.

While not a new instrument — companies have used locks and hedges for decades — their increasing popularity of late indicates a desire by corporates to gain visibility into future financing costs and protect themselves against sudden rate shocks, especially if they have upcoming maturities or plan mergers and acquisitions.

“With rates coming down dramatically and corporations having financing needs in 2024 and beyond, treasurers are jumping on the ability to lock in lower Treasury yields,” said Amy Yan, co-head of global rates and currencies solutions at BofA.

Pre-issuance hedges can come in a number of forms. One entails a T-lock, which is a synthetic agreement with a bank that allows the issuer to essentially lock in an underlying benchmark Treasury rate. Some companies use so-called collars, which limit a borrower’s downside if rates rise, but cap their upside if they fall.

Corporations may also use derivatives such as forward-starting swaps, or options on swaps known as swaptions, to get more certainty around future funding costs. The tools allow them to hedge issuances as far out as two or more years, though many are used for bond sales within the coming months. The bank on the other side of the trade usually charges a fee based on the size and length of the lock or hedge.

With the Federal Reserve envisaging cutting rates by roughly 0.75 percentage point in 2024, strong employment, sticky price growth and an uncertain outlook with upcoming elections in many countries around the world point to more volatility ahead. Swaps traders, meanwhile, are more dovish — betting on roughly six quarter-point cuts this year.

“This is a very confusing, dangerous time,” Vineer Bhansali, founder of LongTail Alpha LLC and a former executive at Pacific Investment Management Co., said earlier this month in an interview with Bloomberg TV. Bhansali expects 10-year Treasury yields to trade in a wide range between 3.65% and 5% in the months ahead.

Investment-grade bond markets have had a strong start to the year with rates down from last year’s peak levels. Issuers have priced about $100 billion in new debt through Jan. 12, according to data compiled by Bloomberg, and monthly projections call for $160 billion in fresh supply, more than last January’s $144 billion and the most since 2017.

Some companies “think the market has overadjusted,” said Reid Hamilton, head of corporate risk solutions in the Americas at HSBC, pointing to recent declines in Treasury yields that led firms to seek protection in case they go up again. That protection, however, comes at a cost, as banks charge a fee for those derivatives and companies can find themselves trapped if rates fall.

By the same token, they can profit. Safehold Inc., a New York-based company specializing in ground leases, secured long-term interest rate hedges for $400 million of future debt issuance.

“While these hedges protect us through next year, they can be unwound for cash at any point,” Chief Financial Officer Brett Asnas said on an earnings call in November. “As we look to term out revolver borrowings with long-term debt, we would unwind the hedges and attach the gain to the debt, lowering the effective economic rate we pay,” Asnas said.

Companies that plan to take out debt to fund M&A are also looking to hedge, bankers said.

“The percentage of M&A financings that are being locked continues to surge as companies increasingly look to hedge their rates shortly after signing to protect the economics of the underlying deal,” said Shiv Vasisht, co-head of global rates and currencies solutions at BofA.

S&P Global Inc. shaved 75 basis points off a $750 million bond offering in September as a result of a lock, Chief Financial Officer Ewout Steenbergen said in an interview. The company put it in place for its 2020 acquisition of IHS Markit, and still has some left that could be used for a 2025 refinancing, Steenbergen said.

“I think there’s opportunity to do those kind of steps and still refinance in an attractive way despite the higher rate environment,” he said.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nina Trentmann, Carter Johnson