Managing Reinvestment Risk When the Yield Curve is Inverted

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Beware of investing in cash with a plan to extend maturities when the yield curve is no longer inverted. My research shows that this decision is historically difficult to time.

Beware of investing in cash with a plan to extend maturities when the yield curve is no longer inverted. My research shows that this decision is historically difficult to time.

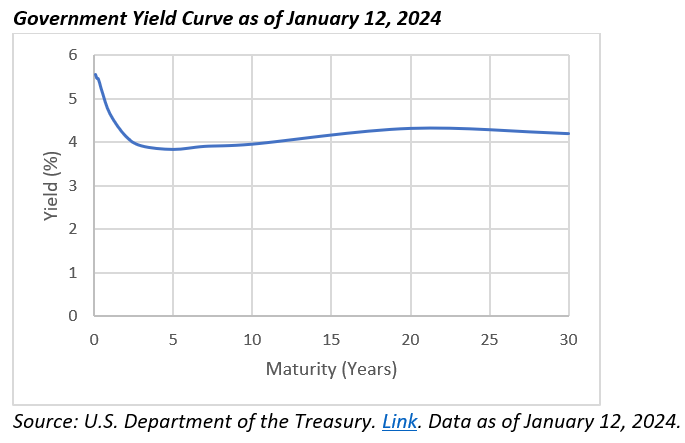

Cash can be an attractive fixed income investment during periods when the yield curve is inverted, like today. As of January 12, 2024, cash (defined as 3-month Treasury bills) had an annualized yield of 5.45% versus 3.94% for 10-year Treasury notes, a spread of 151 basis points. There is a spread difference of only 44 basis points between cash and core bonds, given a yield to maturity of 5.01% on the Bloomberg US Aggregate Bond Index.

While cash may seem risk-free, long-term investors face reinvestment risk: being forced to reinvest in bonds in the future with lower yields if interest rates fall. This is the conundrum facing investors questioning whether to pivot out of core bonds into cash.

This analysis, which relies on historical U.S. data from January 1926 to September 2023, shows that cash yields have declined notably after periods when the yield curve was inverted, while future yields on core bonds have remained roughly flat or fallen slightly at the median. Taken together, the historical evidence says the potential benefits of pivoting to cash during an inverted yield curve environment have been fleeting and that investors may be worse off unless they pivot quickly into bonds when the yield curve normalizes.

A brief look at history

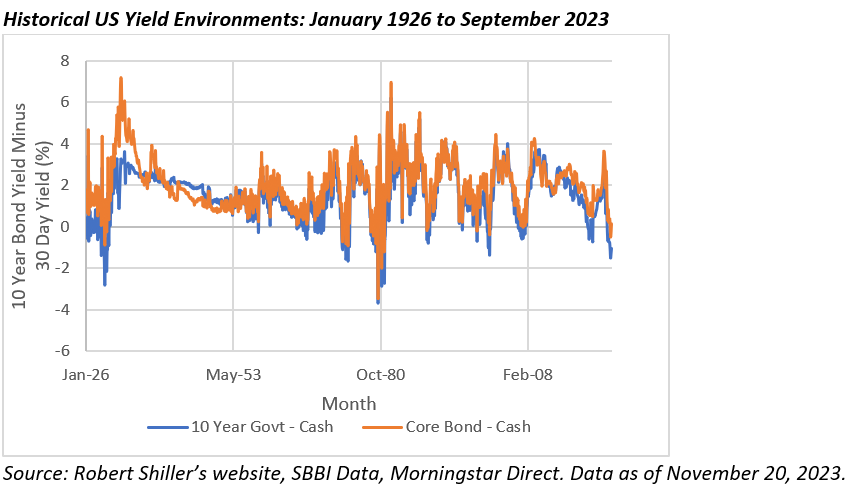

Times when the yield on cash exceeded the yield on longer-dated bonds (e.g., 10-year Treasury bonds) have been rare historically. For example, the next exhibit includes the monthly spread between 10-year government bonds and cash, as well as core bonds and cash, from January 1926 to September 2023. Cash is defined as the yield on 30-day Treasury bills (using the SBBI series) and I used a synthetic proxy for core bonds in my analysis, which is detailed in the Appendix.

From January 1926 to September 2023, which includes 1,173 observations, the yield on cash has only exceeded the yield on 10-year Treasury bonds for 118 months, which was 10.1% of the time. The yield on cash has only exceeded core bonds for 29 months, which was 2.5% of the time.

Since the yield on cash is roughly equivalent to the yield on core bonds, one might think the smart decision is to invest in cash, which is commonly described as being “risk free.” A problem with this perspective, especially for long-term investors, is that it ignores reinvestment risk.

Reinvestment risk affects investors if future interest rates on bonds fall, or the yield on cash declines relative to core bonds and the investor remains in cash. In theory, an investor could watch the market and pivot, but market timing rarely works in an investor’s favor.

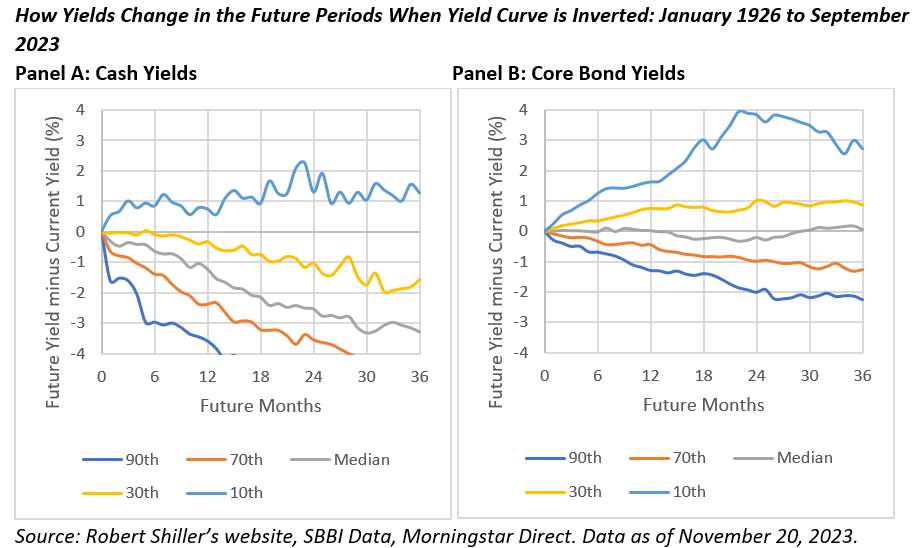

The next exhibit includes information about how yield have historically evolved when the yield curve has been inverted. The analysis compares the current yield to what it is in the future, where the maximum number of months is 36 (or three years).

The yield on cash has historically fallen dramatically during periods when the yield curve was inverted. For example, after a year, the median yield has been 123 basis points lower, after two years 253 basis points lower, and after three years 328 basis points lower. In other words, cash returns have historically dropped significantly during periods when the yield curve was inverted.

For core bonds, the effect was more muted. Median yields were roughly the same, but they were lower approximately 12 to 30 months after the inversion ended. While there may appear to have been an opportunity to pivot to cash in the near term, historically this has been a relatively short-term anomaly and the length of time it could take an investor to pivot back into bonds could result in lower returns.

Appendix: Creating core bonds proxy historical yields

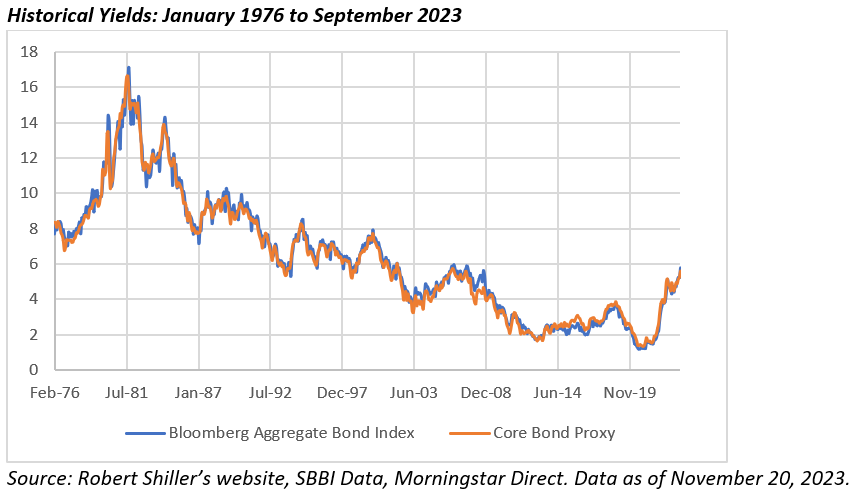

Yields on the Bloomberg Aggregate Bond Index, which is the proxy for core bonds, are only available from January 1976. In contrast, yields on the Moody's Seasoned Baa Corporate Bond Index are available from 1919. Since these indices are relatively different in terms of credit quality and duration, I analyzed how to accurately “back-cast” yields for core bonds.

I did this by creating a “credit factor” by subtracting the yield from the Moody's Seasoned Baa Corporate Bond Yield from the Ibbotson Associates SBBI US Long-term Government Bond Index. I then determined what weight to apply to that factor, by adding that value to the Ibbotson Associates SBBI US Intermediate Government Bond Index to best replicate the historical yield of the Bloomberg Aggregate Bond Index. I found that a factor of .5 was roughly optimal. In other words, adding a half the estimated credit factor to the return of the SBBI US Intermediate Government Bond Index best approximated the historical yield of the Bloomberg Aggregate Bond Index, as demonstrated in the exhibit below. I then applied this approach to the remaining historical data to create a proxy for core bonds going back to January 1926.

David Blanchett, PhD, CFA, CFP®, is managing director, portfolio manager and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an adjunct professor of wealth management at The American College of Financial Services and a research fellow for the Retirement Income Institute.

A message from Advisor Perspectives and VettaFi: Advisors: You're Invited to Exchange! Nothing would be a better start to the new year than if you joined us at Exchange, an in-person conference for members of the financial services community in Miami, Florida on February 11-14th. For a limited time, we're offering you a free Exchange ticket!* Register today with code WINTER24 to claim your pass.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All