The COVID-19 Recession is the weirdest we've ever had. There is no way anyone could have forecast it. It did not happen because the Fed was too tight. It did not happen because of a trade war. It was self-inflicted, caused by COVID shutdowns.

The year 2020 will be remembered for any number of things, including how wrong so many were about so much. From the pandemic to the election, and from the economy to financial markets, prognosticators did a horrible job.

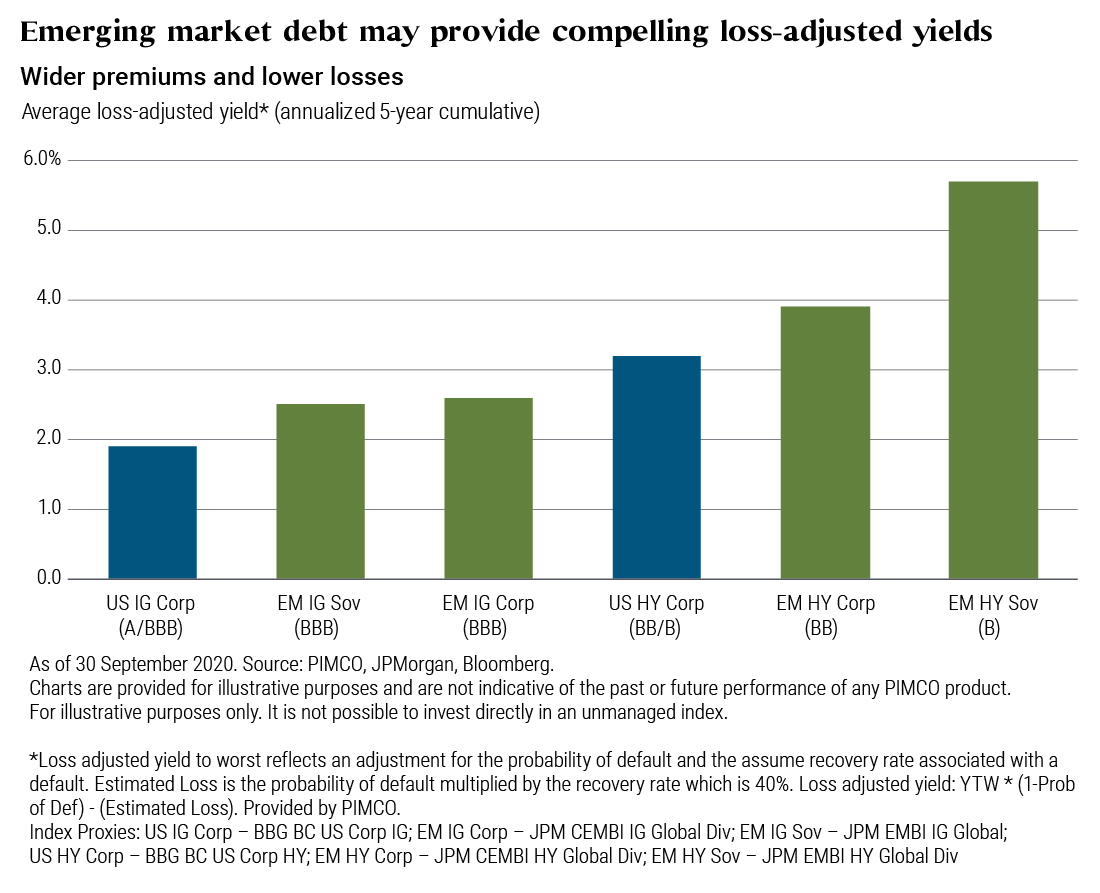

Debt of many emerging market countries can offer robust yields and enhance portfolio diversification, provided the asset manager has the resources and sophistication to avoid potential pitfalls.

The financial health of state pension plans has worsened and advisors should avoid municipal bonds from certain issuers.

In the year 2020, lower coupon bonds are cannibalizing higher coupon bonds.

Two weeks ago I talked about Peter Turchin’s idea of “elite overproduction” leading to social and economic crisis. While he doesn’t have any solutions, Turchin helps illuminate how we reached this point. Today we’ll go a little deeper and think about the implications.

Some changes unfold over time and it’s possible to see them coming. There are demographic changes coming in the next decade that will change the direction of the U.S. since the Silent Generation and the Baby Boomers hold a different view of government than Gen Z’s and Millennials.

With a greater level of clarity than we’ve had since the COVID-19 pandemic, we’re getting a better sense of how the US economy might shape up over the next few months, into 2022 and beyond. We see three distinct stages over that time frame.

For global fixed income investors, diversification is key. In our latest Q&A, Portfolio Manager Teresa Kong, CFA, discusses where she's finding opportunities across Asia today.

The better informed the investor is, the better the investment decisions they can make. But being an informed investor can be a very arduous task, and some would even say that conducting research on common stocks is a real snoozer.

Meeting cash flow needs through distributions is challenging, with Treasury yields at rock-bottom levels and investors enduring widespread dividend cuts this year. Trying to generate a meaningful yield means unacceptable credit risk at a time when the bankruptcies are getting announced following months of government-mandated shutdowns. For investors looking to fund their day-to-day lives, a better approach is to focus on maximizing risk-adjusted returns to meet individual cash flow needs.

Target-distribution strategies, such as those developed by my guest today, leverage a modern-portfolio theory approach focused on risk-adjusted returns to deliver steady cash flow to investors while maintaining the principal over the long-run.

Each market milestone passed in 2020 is a reminder of the Federal Reserve’s extraordinary efforts to hold things aloft -- and a belief that it’ll continue.

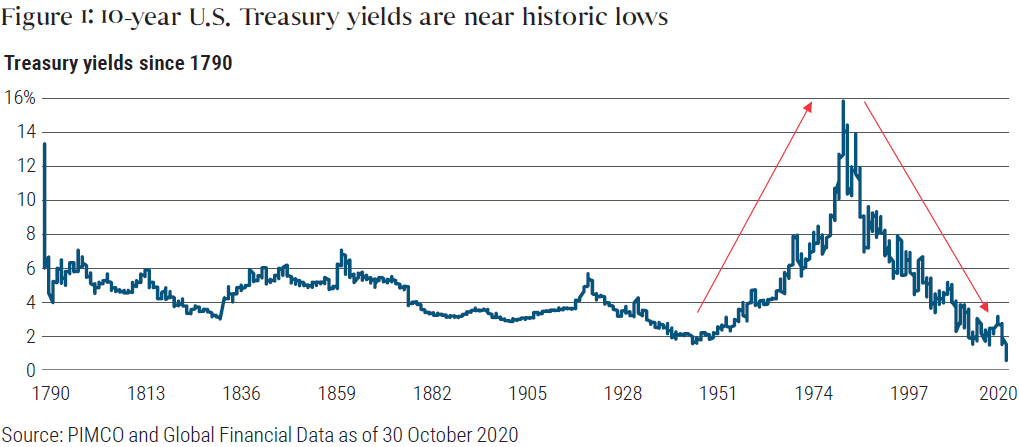

A familiar scenario may be about to play out in the world’s biggest debt market, with a major breakout in long-term Treasury yields at risk of faltering after a banner couple of days for bond bears.

As the global stockpile of debt with negative yields has climbed to a record $17.4 trillion, it’s gotten very tempting to buy less creditworthy bonds to earn more income.

One of the most insidious ideas foisted on investors by Wall Street, in tacit cooperation with activist policy makers at the Federal Reserve, is the fiction that zero interest rates offer investors “no alternative” but to speculate in risky securities.

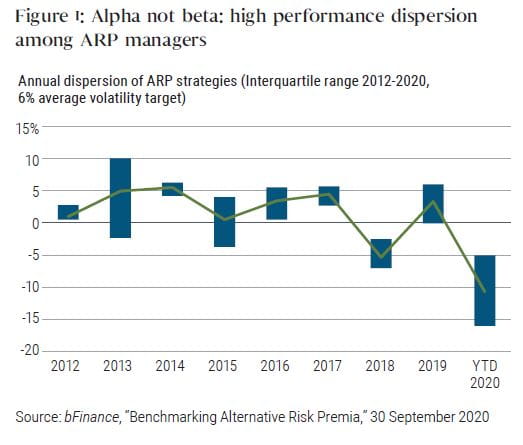

Wide performance dispersion underscores the importance of portfolio construction.

With COVID-19 vaccines on the horizon, the longer-term economic outlook appears brighter.

Many have been puzzled that the world’s stock markets haven’t collapsed in the face of the COVID-19 pandemic and the economic downturn it has wrought. But with interest rates low and likely to stay there, equities will continue to look attractive, particularly when compared to bonds.

We expect the municipal bond market to return to a sense of normalcy in 2021.

After a difficult winter, we expect the global economy to rebound strongly next year. But structural headwinds remain. Will the post-pandemic bounce trigger a durable and broad-based global reflation?

We have recently written a couple of posts about the “exuberance” that has invaded the market since the election. Such is often seen near short- to intermediate-term peaks in markets as investors go “all-in” without a net.

So far this year, shares of HIVE Blockchain Technologies have soared an incredible 715%, well past Ethereum’s gain of 273%. 2020 has been marked by healthy expansion in mining capacity, the most recent example being HIVE’s acquisition of additional access to low-cost green energy.

Applications for U.S. state unemployment benefits unexpectedly posted the first back-to-back weekly increase since July, while Americans’ incomes and savings fell last month.

The biggest private equity firms in the U.S. are unleashing a flurry of new leveraged buyouts and debt-funded dividends, seeking to make up for lost time after staying on the sidelines for much of 2020.

We are cautiously optimistic about economic growth over the next year, but over the longer term, disruptive factors will likely contribute to heightened volatility and lower returns across both fixed income and equity markets.

Since early August the “barbarous relic” has corrected some 9% while many other assets have ascended to all-time highs. This has no doubt caused a bit of consternation for holders of gold who have been using the metal not as a hedge, but as a capital appreciation vehicle unto itself.

The tide in the $20 trillion Treasury market appears to be turning in favor of the bulls for now, with expectations growing that the Federal Reserve will boost purchases of longer-maturity debt as soon as next month.

A balanced portfolio of stocks and bonds for decades was among the few venerated precepts in investing. Yet doubts about the approach grew after the pandemic hit and turned 2020 into a year like no other.

Amid historically low rates, the income solutions of yesterday are not going to cut it. Global X ETFs has recognized and reacted to this paradigm shift by developing alternative, higher-yielding strategies.

“I predict the bull market will continue next year,” says Jeremy Siegel. “Stocks are not overpriced.”

In a market ruled by historically low bond yields, income-seeking investors are being driven to products that carry risks, many of which are hard to identify or evaluate.

Amid an environment of near-zero benchmark and T-bill yields, for a modest increase in risk, PIMCO's short-term strategies may offer higher levels of total return and income for stepping beyond the confines of money market fund strategies.

Gold “is a hedge on policymakers screwing up, and there has been a lot of screwing up in the last 20 years.”

It was a bumpy ride for corporate bond investors this year. After the sharp, pandemic-driven selloff in February and March, total returns for most corporate bond investments have climbed their way back into positive territory.

Whether you’re celebrating in-person or virtually, we’re wishing you and your family a Happy Thanksgiving! Giving thanks may seem difficult to do in a year that’s resulted in the loss of so many lives, jobs, and businesses, but we believe this holiday is the perfect time to reflect on all we are grateful for.

In our view, inflation-fighting asset classes look considerably cheaper and offer higher long-term estimated returns than mainstream stocks and bonds.

In calling the current market the third “Real McCoy” bubble of recent decades, Jeremy Grantham described, in his own words, what I call the Iron Law of Valuation: a security is nothing more than a claim on some set of future cash flows that investors expect to be delivered into their hands over time. The higher the price an investor pays today for some amount of cash in the future, the lower the long-term return the investor can expect on that investment.

Ten-year Treasury bond yields may rise as high as 1.6% in 2021, reflecting prospects for faster economic growth.

With yields near zero, many investors may question the value of fixed income within a portfolio. Western Asset’s Head of Product Management, Doug Hulsey, joins our Head of Equities, Stephen Dover, to discuss fixed income investing with an active-management lens. He makes a case for the asset class for investors in light of market uncertainties and outlines where he sees opportunities today.

He is not sure when it will happen, but David Rosenberg is confident investors will face another big correction in the stock market.

When the definitive story is written about U.S. financial markets during the coronavirus pandemic of 2020, expect America’s housing market to play a starring role.

The traditional “60/40” portfolio of stocks and bonds can be saved with a few modest tweaks.

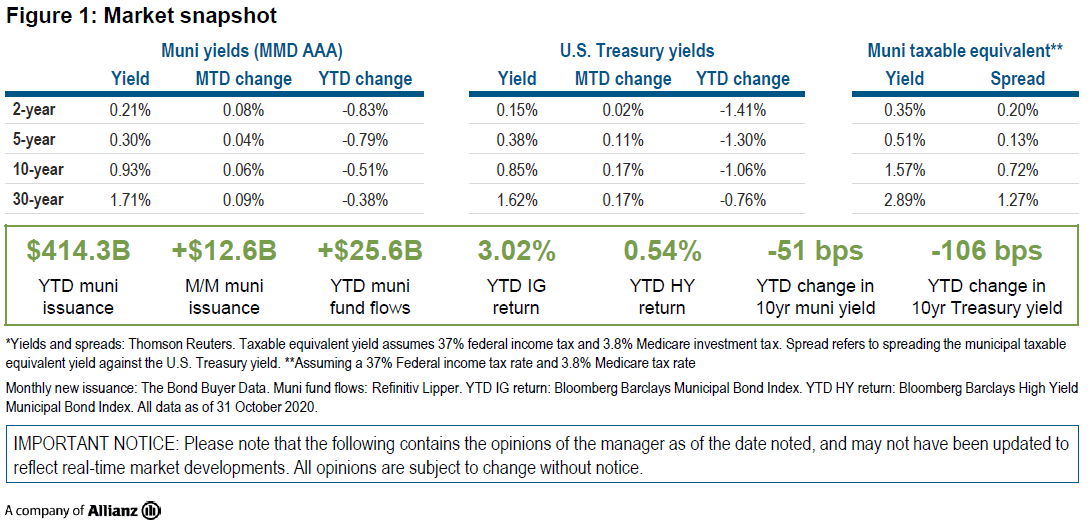

A brief monthly update on what's happening in the municipal bond market.

This short article investigates the rebalancing premium that investors may expect from risk-parity portfolios.

This article highlights the real golden goose behind retirement accounts – the immense value in not having to pay taxes on investment income and rebalancing.

Actual third-quarter earnings may be less important than what business leaders say about their expectations.

Bundling may help plan sponsors unlock alpha potential and supplement low returns from long Treasury bonds.

The Franklin Templeton–Gallup Economics of Recovery Study has heralded some interesting results in regard to the attitudes and behavior of Americans in response to the ongoing pandemic—and what developments could change both.

Meeting cash flow needs through distributions is becoming challenging with Treasury yields at rock bottom levels and investors enduring widespread dividend cuts this year. Trying to generate a meaningful yield often means unacceptable credit risk at a time when the bankruptcies are just starting to get announced following months of government-mandated shutdowns. For investors looking to fund their day-to-day lives, a better approach may be to focus on maximizing risk-adjusted returns and manufacturing a distribution to meet individual cash flow needs while managing risk and return. Target distribution strategies seek to leverage a modern portfolio theory approach focused on risk-adjusted returns to deliver steady cash flow to investors while maintaining the principal over the long-run.

In this webinar, participants will learn about:

We’ve seen aggressive government and central bank support to stimulate economies sickened from COVID-19 slowdowns, but will the global economy right itself in 2021?