In times of higher volatility, a multi-asset strategy can offer more consistent income, diversification and upside potential relative to bonds.

Several pundits have raised the possibility that the current Covid-recession will be followed by a boom reminiscent of the Roaring '20s. Although we think that may be a tad too optimistic, we think the recovery will continue and feel “real economy” stocks could fare particularly well.

2020 was a remarkable year, to say the least. As we begin 2021, we are faced with as many questions as we have answers. While the global pandemic caused economies to come to an abrupt halt in early 2020, we are now seeing some recovery, albeit tempered by recent spikes in infections.

Janet Yellen encountered early Republican resistance to President-elect Joe Biden’s $1.9 trillion Covid-19 relief plan in her confirmation hearing to become Treasury secretary Tuesday, as she sought backing for what she described as vital support for the economy.

Despite seeing major market swings following the 2016 Brexit referendum, we don’t expect Britain’s departure from the European Union (EU) to have any major economic effects in our baseline outlook for 2021 and beyond. Far more important are COVID-19, fiscal policy, and bigger questions around future productivity growth.

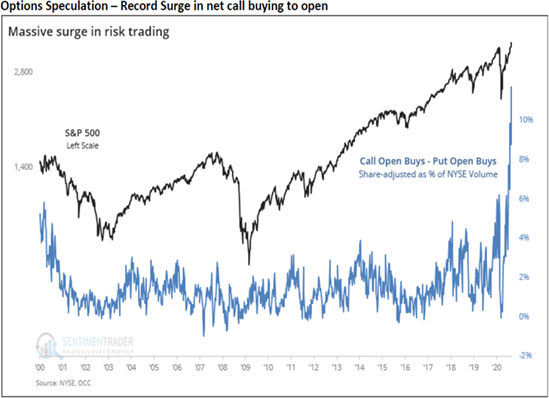

The speculative “V” is one of the most interesting and challenging features of the market cycle. For passive investors, it can be a period of exhilaration followed by panic.

The new year kicked off with a sharp rise in Treasury bond yields, despite unprecedented political turmoil and signs that the economic recovery is slowing.

2021 market outlook from BlackRock's municipal bond team.

A confluence of dynamics are set to accelerate global capital flows to emerging markets amid attractive valuations.

U.S. Treasury Secretary nominee Janet Yellen on Tuesday steps into a new role following more than a quarter-century in government: salesperson for economic policy after years of defending Federal Reserve thinking and actions.

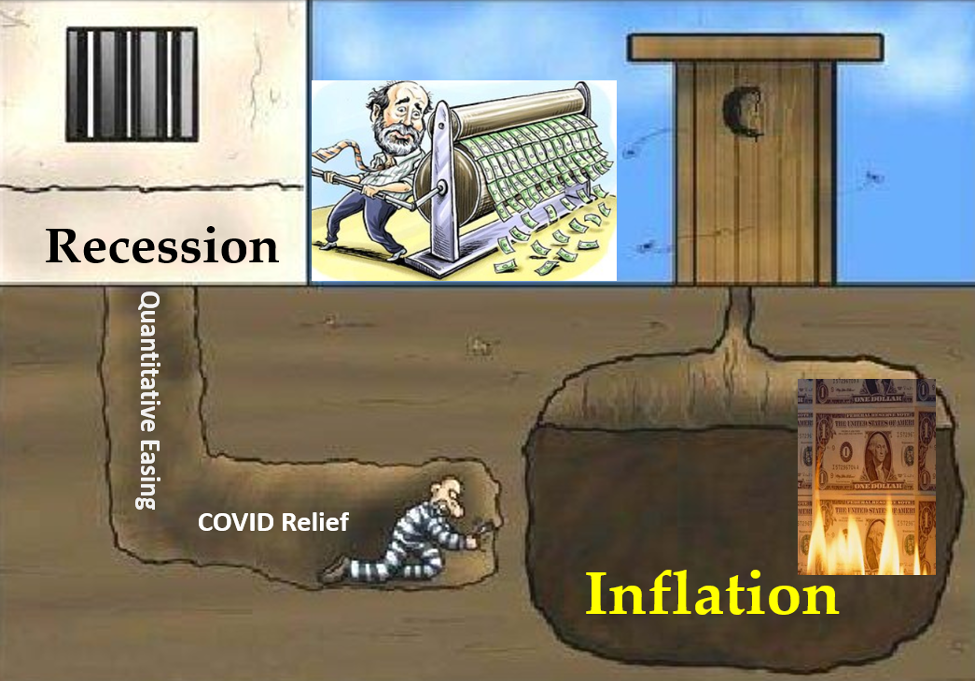

Rescues by the Federal Reserve and aggressive monetary policies have helped stock and bond investors, but the degree of money printing will be paid for by future generations.

Founding Father Benjamin Franklin said it best: “They who can give up essential liberty to obtain a little temporary safety deserve neither liberty nor safety.” In this light, what are we to make of Trump’s social media suspension?

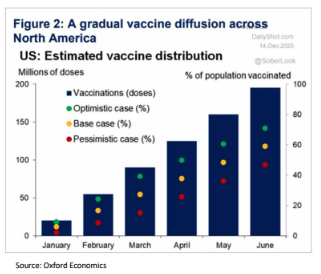

U.S. stocks have continued to climb amid optimism about a vaccine-led economic recovery, but it’s a narrow path—buoyant investor sentiment could easily be deflated by bad news. Although global economic growth has struggled, an acceleration in vaccinations in major countries could support stronger growth in the second quarter.

A brief monthly update on what's happening in the municipal bond market.

Our K2 Advisors team is optimistic about the opportunity set in the year ahead, and thinks that active management alpha will be key to success in 2021. Brooks Ritchey and Robert Christian provide the team’s first-quarter hedge-fund strategy outlook.

The Loomis Sayles Investment Grade Sector Team answers three questions on their outlook for 2021.

The forceful rise of the markets from March depths continued in the fourth quarter. After stalling out in early Fall, market participants floored the accelerator in November with vaccine approval in tow and the election overhang in the rearview.

The conventional wisdom that inflation will be rekindled in the U.S. -- ending the massive Treasuries rally and driving up yields -- is bunk, according to a Texas fund manager whose three-decade bullish stance on bonds propelled another banner year in 2020.

Municipal bond issuers’ financial health and resiliency—which helped in 2020—should support opportunities for active muni investors in 2021.

John Bell shares his thoughts on yields, defaults and the role of CLOs in the loan market in 2021.

Federal Reserve officials are beginning to split over when they may need to start pulling back on their massive monetary stimulus, drawing nervous glances from investors who remember how markets were roiled during the 2013 taper tantrum.

Bitcoin rebounded after Monday’s steep plunge left investors grasping for clues about what lies ahead for the world’s largest cryptocurrency.

Global output and demand are likely to rebound strongly in 2021, but we see risks that call for careful portfolio positioning.

Equity markets continued a torrid run in the fourth quarter, propelling nearly all sectors and asset classes back into the black for 2020. But Q4 was defined by a notable shift in market leadership as cyclical sectors and asset classes bested defensives and growth stocks.

The trouble with bubbles is they prey on human weakness. They are also high impact investment events.

In his forecast for 2021, Jeffrey Gundlach predicted a “regime change.” Investors should prepare for themes that reverse prior trends: U.S. equities will underperform the rest of the world, inflation will rise, volatility will be higher, and the dollar will weaken.

Credit markets have staged an epic rebound from the depths of March 2020. But in a low-growth, low-yield world, we believe there may be more room to run in 2021.

The Loomis Sayles Emerging Markets Debt Sector Team shares their views on corporate spreads, foreign exchange and leverage in 2021.

Wall Street strategists are going all-in on reflation bets that powered global markets through last week’s U.S. political mayhem and the spreading pandemic.

They’re still in the minority, but investors and economists who think America is in for a bout of inflation -- perhaps a serious one -- start the year with some fresh ammunition for their arguments.

The dichotomy of “value” and “growth” investing has become a sharp stylistic divide. But is it helpful? Howard Marks writes in his latest memo how he views the art and science of value investing, especially in the increasingly efficient and complex world we face today.

How does one then make the case for a cautious outlook for stocks?

The Fed juices the stock market in four ways.

I’ll focus on rebalancing versus buy-and-hold with a focus on retirement withdrawals.

What can investors expect this year? Positive (but unsteady) economic growth, a powerful boost in earnings and continued success for information technology stocks, says Raymond James Chief Investment Officer Larry Adam.

This should be positive for gold, given the potential for greater government spending and, therefore, inflation.

This week’s letter is the first part of my 2021 forecast. There is simply too much to cover in one letter, and today we’ll start with the most important factor, a known unknown, that I think will be the driver for 2021.

Despite extensive economic and human costs, 2020 may be a turning point in multiple ways.

Chances of another federal stimulus package got a boost as Democrats swept this week’s Senate runoff elections in Georgia, offering the prospect of more support for people and businesses hammered by the pandemic.

LIBOR is still being retired, just a little later than initially expected.

Emerging-market sovereign debt has rebounded sharply off the lows, but this hard-hit sector offers attractive yields and compelling growth opportunities to discerning investors.

Free from a house view on economies, markets or stocks, J O Hambro Capital Management’s (JOHCM) fund managers invariably see the world in different ways. We asked a number of our managers for their thoughts on the outlook for their asset class next year, what they would like to see and the possible surprises that 2021 could bring.

In this abridged version of our latest Asset Allocation Outlook, we discuss the opportunities and risks of investing in an early cycle recovery.

As the new year begins, the investment grade (IG) market faces multiple challenges, including a recovering economy, low yields, tight spreads, and record high duration. At the same time, market technicals remain favorable, fundamentals are improving, and there are attractive sectors in the index. Overall, we are modestly bullish about 2021 and feel there are compelling opportunities for those who know where to look.

Bonds with the same S&P or Moody’s credit rating can vary greatly in terms of their risk and subsequent return. New research show that fixed income investors must also consider their credit spreads.

U.S. stocks will sink in coming months before resuming their record-setting rally and faster growth will spark inflation and higher yields in Treasuries, according to Byron Wien’s annual list of surprises.

The IPO market is manic. Stocks haven’t been this expensive since the dot-com era. The Nasdaq 100 has doubled in two years, leaving its valuation bloated -- all while volatility remains stubbornly high.

As we enter 2021, it appears that Buffett had things upside down in 2020. The things which had gone up the most by the end of 2019, went up the most in 2020.

Editor’s Note: We’re changing things up. Every year, Loomis Sayles features outlooks from our sector teams — teams composed of traders, analysts, strategists and portfolio managers immersed in their respective sectors of the market. This year, we’re tailoring our outlooks to focus on what’s top-of-mind for many investors.

Featuring extreme overvaluation, explosive price increases, frenzied issuance, and hysterically speculative investor behavior, I believe this [bull market] event will be recorded as one of the great bubbles of financial history, right along with the South Sea bubble, 1929, and 2000.