Our outlook for municipals this year

BlackRock’s municipal bond experts share their market outlook and the actions you can take to raise your portfolio’s potential in 2021.

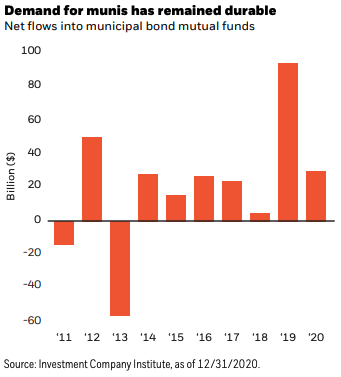

The assets that command demand

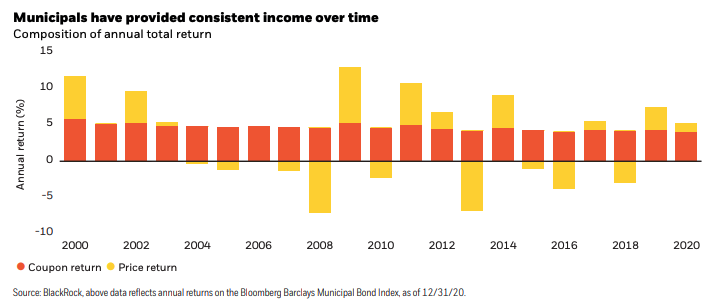

Even as the pandemic spurred the most abrupt and severe selloff of modern history, the S&P Municipal Bond Index finished 2020 with a gain of 4.95% as strong demand for muni bonds broadly outpaced supply. We expect the positive momentum to continue in the coming year, albeit with moderated returns.

Municipal bond mutual funds have attracted positive flows from investors in each of the past seven years — since the extreme rate volatility infamously known as the “Taper Tantrum” stressed fixed income assets broadly in 2013. Demand for municipal bonds continues to be supported by highly accommodative monetary policy, while the potential for higher taxes under the new political regime underscores the appeal of tax-advantaged investments. Notching a solid return for a tumultuous 2020 also bodes well for munis in the months ahead as positive returns tend to create further demand.

Some volatility in fund flows can be expected given the forecast for low- to mid-single-digit returns and the likelihood of interest rates moving modestly higher and creating a steeper yield curve. Nevertheless, we anticipate another year of net positive flows into the asset class.

We view high yield municipals as a particularly appealing area to look for opportunities in 2021. The sector has lagged in the broader muni rebound from the pandemicinduced selloff, suggesting the potential existence of underpriced assets and room to move higher. By the end of 2020, investment grade municipals had recouped 138% of its outflows from the March selloff, while the high yield sector regained only 37%. In our view, high yield is poised to readily outperform investment grade. Nevertheless, investors need to be highly selective as the impact of the pandemic varies across market segments and issuers.

Supply remains robust but more diverse

Supply is likely to remain elevated this year albeit not to the extent believed prior to the Georgia runoff elections. Historically low interest rates create a favorable environment for issuing debt. We anticipate annual issuance in the range of $450-475 billion, albeit with periods of volatility, and continued strong demand to absorb it. (Demand creates supply in credit markets.)

More important than the amount of issuance, however, is its underlying composition. Taxable municipals, which had historically represented a very small portion of total muni issuance, have become a meaningful contingent since the ability for issuers to advance refund their debt via taxexempt issuance was eliminated as part of the tax reform in 2017. The probability of the new administration restoring the advance refunding exemption will have a large influence on the amount of taxable municipal debt issued this year; however, under current tax law, we project taxable bonds constituting 30% of municipal issuance in 2021. The increasing amount of taxable issuance implies a reduced amount of tax-exempt issuance, further strengthening the positive technical environment for tax-exempt municipals.

We expect another year of net-negative issuance in the tax-exempt space (i.e., when the total amount of debt that is called, refunded or reaches maturity exceeds the amount of newly issued debt). This tailwind has occurred more frequently in recent years versus the seasonal trends that once provided some degree of predictability.

As a new and more centralized administration steps into office, we anticipate a renewed focus on infrastructure. The impact on muni issuance is likely to be minimal, absent a significant subsidized program similar to the Build America Bond program that rolled out in 2009.

Strategy insights for a volatile 2021

Volatility is a central theme of our 2021 outlook given the myriad of uncertainties around the spread of COVID, the success of rapidly developed vaccines, the timing of a fully re-opened economy, and the effectiveness of government stimulus. While interest rates are set to remain broadly low, we expect a further increase when economic activity returns to normal. Municipals tend to outperform Treasuries when rates rise, retaining the appeal of the asset class even for investors holding the most skeptical views on yields.

Despite higher volatility in rates, flows and issuance, we expect demand for municipals to remain durable and continue to outpace elevated supply in 2021. We anticipate low- to mid-single-digit returns for the asset class, with notable contributions from the high yield sector both in terms of income generation and outperformance versus investment grade. Security selection will be paramount given increased performance disparity among market segments.

We begin 2021 with a neutral stance on duration (interest rate risk) and a “barbell” yield curve positioning, i.e., heavier exposure to short- and long-term bonds vs. intermediate terms. We hold an overweight to credit sectors and particularly high yield. In anticipation of an economic restart, we favor travel-related areas that could benefit from pent-up demand. We also hold a preference for local communities with strong housing demand in Colorado, Florida, Virginia and North Carolina.

We believe the municipal bond market will continue to offer attractive opportunities in the year ahead, but if there’s one thing investors learned in 2020, it’s the importance of prudent risk management, flexibility and expertise to navigate an increasingly diverse and volatile marketplace.

Credit views for 2021

Budgets in recovery. The pandemic has taken its toll on 2020 budgets for state and local governments. Lockdowns curtailed revenue collections while the expansion of social programs and the spike in unemployment drove spending well above forecasts. Whereas a resurgence of the virus and further lockdowns are worrisome, there are plenty of reasons to believe 2021 will be a year of recovery for U.S. public finance: the roll out of vaccines, an economic boost from pent-up demand, the resiliency of sales and income taxes, strength in U.S. housing and equity markets, and very low borrowing rates. Additionally, we believe the new administration will be more supportive to state and local governments and willing to provide stimulus as necessary.

Bargains await. Continued downgrades in municipal ratings are anticipated. This typically drives credit spreads wider, creating prospects to buy solid credits that are poised to benefit from the recovery. Sharp rebounds are likely in travel destination cities, the airports that serve them, and dedicated hotel tax bonds in those markets. Hospitals that are experiencing compressed margins coinciding with the pandemic will mend when their volumes shift back to normal. Likewise, most colleges and student housing issuers are looking forward to the return of students this fall.

What’s trending in taxes. States in the mountain west and mid-south that benefit from low tax burdens and a highly educated labor force with the ability to work from home are well situated. Caution is warranted in high-tax states and their large cities that are vulnerable to corporate flight and outmigration if remote working becomes the new norm. At the local level, demand for homes in suburban areas is driving property values, and consequently, tax receipts higher, buoying the fundamental outlook for local governments and school districts. Pension funding levels remain problematic for a handful of municipal issuers, although in our view, this concern does not have to be addressed in the near term, especially given the strong investment performance across the capital markets.

High hopes for high yield. Despite dramatic underperformance last March and April when the S&P Municipal High Yield Index dropped -11.2%, the high yield sector finished 2020 with a strong gain of 6.00%, besting the broader S&P Municipal Bond Index by 1.05%. We anticipate that high yield will outperform again in 2021 with the tailwinds of low rates, limited supply, improving fundamentals, attractive credit spreads, and the reversal of flows alongside investors’ increased risk appetite. Credits with measurable cash flows such as tobacco, COFINA (Puerto Rico sales tax bonds), corporates and established retirement community bonds should be favored. We believe there is significant value in the Puerto Rico general obligation and electric power authority (aka PREPA) bonds, which are expected to be restructured this year. Conversely, careful diligence is required before investing in segments deeply impacted by COVID such as long-term care facilities, small universities and highly speculative start-up projects. Overall, we remain constructive on high yield municipals for their diversification benefits, high levels of income and the potential to be rewarded for superior security selection.

1 BlackRock as of 12/31/2020.

2 BlackRock as of 12/31/2020.

Investment involves risk. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of January 15, 2021, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

Prepared by BlackRock Investments, LLC, member FINRA.

Not FDIC Insured • May Lose Value • No Bank Guarantee

Lit No. MUNI-OUTLOOK-0121 OE42008T-0121

© BlackRock

Read more commentaries by BlackRock