In his forecast for 2021, Jeffrey Gundlach predicted a “regime change.” Investors should prepare for themes that reverse prior trends: U.S. equities will underperform the rest of the world, inflation will rise, volatility will be higher, and the dollar will weaken.

Gundlach is the founder and chief investment officer of Los Angeles-based DoubleLine Capital, a leading provider of fixed-income mutual funds and ETFs. He spoke to investors via a conference call on January 12. Slides from that presentation are available here. This webinar was his annual forecast for the global markets and economies for 2021.

Before we look at Gundlach’s 2021 predictions, let’s see how well his forecast from last year, which I reported on here, held up:

- The yield curve will steepen – Correct, the 2-30 year spread went from 75 to 152 basis points

- Long-term rates will rise – Incorrect, the 30-year yield went from 2.33% to 1.65%;

- Gold will go up – Correct, the GLD ETF returned 24.81%;

- There is a 30-35% chance of a recession – Correct;

- Inflation will be subdued – Correct, inflation was 0.62%;

- Stocks and bonds will not do as well in 2020 as in 2019 – Stocks correct (based on SPY, 31.22% in 2019 versus 18.27% in 2020); Bonds incorrect (based on AGG, 8.46% in 2019 versus 7.48% in 2020);

- The dollar will weaken – Correct, the DXY went from 96.85 to 89.94

- Bernie Sanders would be the Democratic nominee – Incorrect

- Commodity prices will be higher – Incorrect, the GSCI index had a return of -23.94%;

- Emerging markets would do well – Correct, the EEM ETF returned 17.03%

- European stocks will do poorly – Correct, the SPEU ETF returned 6.37%, about 12% worse than SPY);

- China would do poorly – Incorrect, the MCHI ETF returned 27.78%

- Among bonds, BBB would outperform B bonds – Correct, BBB returned 9.88% versus 4.59% for B bonds

That is nine correct and five incorrect predictions.

The subtitle of his talk was Aqualung, in recognition of a Jeff Koons sculpture from the 1970s (Gundlach is a follower of contemporary art). The aqualung is an artificial breathing device, and he used it to signify the tools (such as monetary policy) that are benefiting the capital markets to help them survive.

Across the capital markets

Based on a Deutsche Bank summary of investors, U.S. and emerging market equities are the most favored asset classes, and least favored are core fixed income, cash and U.K. equities.

World GDP forecasts have not changed since the middle of last year, despite the development of vaccines. We are still in a recession, Gundlach said. “You need to fully reverse the negative performance – and get back to pre-COVID GDP trend,” he said. “We remain mired in a house of mirrors with all these policies.”

GDP trend growth was about 2.5% since 2016, and we are $1 trillion below that trend line. That is where we need to be to be out of recession, according to Gundlach.

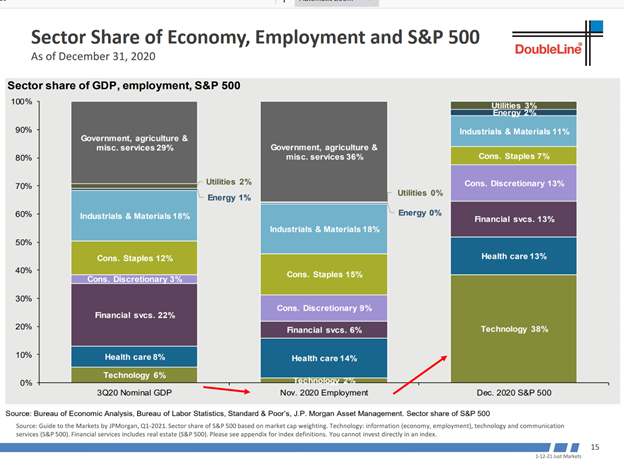

Technology is 6% of GDP and 2% of employment, but it represents 38% of the market capitalization of the S&P 500. That was one takeaway from the chart below, which he said is a symbol of “wealth inequality writ large”:

Travel, based on TSA data, is less than half of pre-COVID levels, but there were upticks around Thanksgiving and Christmas. He said those upticks support the idea that there is pent-up demand.

Survey data shows that the percentage of people who prefer to work from home five days a week went from 27% pre-COVID to 61% in October, and 95% of respondents want to work one day a week. This will force business leaders to make “tough decisions” to restructure to accommodate extended working from home, he said.

Once the pandemic began, the first layoffs were in the travel, leisure and hospitality sectors. As the economy restructures, layoffs will climb the income ladder. Gundlach thinks that climb has already begun.

The consumption of goods has grown, but there is less employment. He called this the “dark underside” of stimulus. Consumers are spending more, but in ways (such as on-line retail) that create fewer jobs.

Among large countries, those with the biggest increase in debt-to-GDP from the end of 2019 to Q3 of 2020 were Canada, China, the U.S. and Japan. U.S. government debt grew from 98% to 127% of GDP.

Gundlach showed familiar charts depicting the growth in the Fed’s balance sheet. The Fed plans to increase it by an additional $120 billion/month in 2021 – $80 billion from QE and $40 billion from the purchase of mortgage-backed securities.

The trade deficit has started to expand, albeit slightly, to 3.4% of GDP, and that is the largest since 2008. The fiscal deficit is “exploding,” he said. That growth of the twin deficits means the dollar is in a secular decline. There is an 18- to 24-month lag in the effect of those deficits on the dollar, so Gundlach is neutral on the dollar for now.

“The big directional change will be lower on the dollar,” he said. The DXY peaked in 2016 and again at the start of the pandemic. “Now it is in decline.”

The S&P 500 is supported by zero interest rates, he said, but inflation is the big “game changer.” Inflation has been very stable and supported both stocks and bond prices. But higher inflation could lead to higher correlation between those asset classes.

The forward P/E ratio of the S&P 500 is 6% higher than for non-U.S. markets. It is usually 2% higher, he said. This is the biggest difference between U.S. and non-U.S. valuations since 2008. “Maybe the U.S. has topped out versus the rest of the world,” Gundlach said. Since 2009, the U.S. has outperformed the rest of the world by a factor of three.

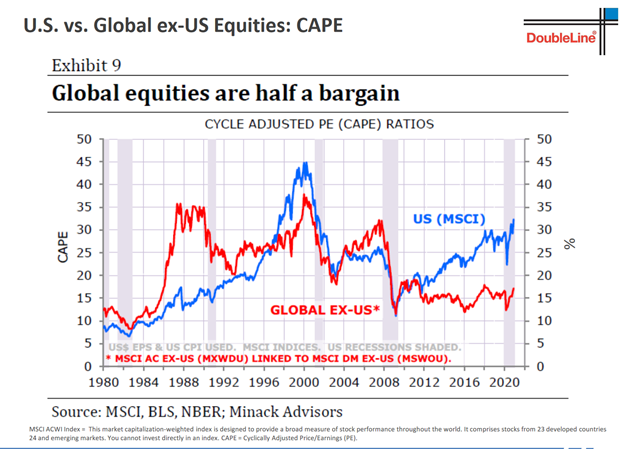

The CAPE ratio for U.S. stocks is 32, but for the rest of the world it is about 16, he said. The U.S. ratio has not always been higher, particularly prior to the dot-com era. “The U.S. does not have a historical birthright of a higher CAPE relative to the rest of the world,” Gundlach said.

Emerging markets, based on the EEM ETF, have been outperforming the SPY since June, after underperforming since the beginning of 2019. He recommended that investors overweight Asian markets. Latin American markets have done poorly, and Asia is driving the entire move, particularly Korea. But Latin America is coming back, he said, as a result of the vaccine; it is one of the primary beneficiaries of vaccines. He said to invest in Latin America if you have the risk tolerance.

Volatility, based on the VIX, averaged almost 30 in 2020, about three times its average starting in 2013. This is a harbinger of “significant regime change,” Gundlach said.

The Nasdaq, when compared to the S&P 500, has reached the same level it achieved in the dot-com era. But Gundlach warned that the FAANGS are “sputtering.” If we take out the 1999 extreme, “it’s over,” he said, implying that U.S. equity prices would broadly decline.

In other signs of regime change, the Dow industrials are no longer outperforming micro caps, and the S&P 500 is no longer outperforming the Russell 2000 small-cap index. This year has seen a “roaring start” for small caps, he said, and companies with weak balance sheets are no longer outperforming.

Zombie companies, those with interest costs greater than profits, have grown from 8% to 15% of the corporate universe over the last decade. That is deflationary and supports lower prices, as those companies use aggressive pricing.

Gundlach provided data on global bank stocks. Since 1995, Japanese banks are down 84%. European banks followed U.S. banks until the global financial crisis. Since then, the U.S. did much better than those in Europe. This was because of low and negative interest rates, which he said have afflicted Japanese and European banks. U.S. banks have benefited from the Fed’s position of not going to negative interest rates.

Inflation has not reached 3% for more than 20 years, he said, based on core CPI data. This will not continue, according to Gundlach. But the result could be deflation (due to debt levels) or inflation (due to money printing). Nonetheless, he predicted the CPI will go above 2.5% by June of 2021.

He recommended a barbell portfolio. Half should be in cash and Treasury bonds, as a hedge against deflation. Of the remainder, put 25% in equities, mostly emerging markets and especially Asia, and 25% in real assets (real estate or gold), as a hedge against inflation. “This is a winning formula,” he said.

He said he is neutral on gold. It is not in a good “trade location” for buying. He is neutral on bitcoin as well, but it is too volatile for him (“you could lose 20% in an hour”). The recent rise in bitcoin’s price is based on a narrative of institutional endorsement, including from the famed investor Paul Tudor Jones.

Equities are expensive, but they are not expensive relative to bonds. He used the chart below to show the yield based on the Shiller (CAPE) earnings relative to the 10-year bond yield. Equities are near the band that makes them very cheap relative to bonds.

The copper-gold ratio indicates that the 10-year yield should be 2%. Gundlach added that many metrics say bond yields are too low.

Expect the yield curve to steepen, he said, at least until the Fed does yield-curve control. “We could go to a 300 basis point 2-10 year spread if there is no yield curve control,” Gundlach said.

Another factor pointing to higher yields is that foreigners have been selling Treasury bonds for the last seven years. Gundlach questions whether there would be sufficient buyers of newly issued Treasury bonds to prevent yields from spiking higher.

He said bank loans look “cheap” and will benefit from rising inflation and rates.

Read more articles by Robert Huebscher