The subject of rebalancing investment portfolios has generated much discussion as well as confusion among advisors and researchers. A recent example is the October 2020 Advisor Perspectives article by Michael Edesess, which has drawn more than 100 comments on APViewpoint. There are upsides and downsides associated with various rebalancing strategies (including the strategy of not rebalancing), and it’s important to look at the full picture. For this analysis, I’ll mainly focus on rebalancing versus buy-and-hold (not rebalancing) with a focus on retirement withdrawals. I’ll utilize Monte Carlo simulations and provide measures of benefits and risks.

The subject of rebalancing investment portfolios has generated much discussion as well as confusion among advisors and researchers. A recent example is the October 2020 Advisor Perspectives article by Michael Edesess, which has drawn more than 100 comments on APViewpoint. There are upsides and downsides associated with various rebalancing strategies (including the strategy of not rebalancing), and it’s important to look at the full picture. For this analysis, I’ll mainly focus on rebalancing versus buy-and-hold (not rebalancing) with a focus on retirement withdrawals. I’ll utilize Monte Carlo simulations and provide measures of benefits and risks.

Background

My interest in the subject of rebalancing stemmed from my earlier analysis of asset allocation where I made the case (in this article) that modest differences in stock/bond mixes were not an important determinant of retirement results – such allocation differences tended to get swamped by variability of year-by-year performance of the underlying asset classes, principally stocks. There is considerable overlap between rebalancing and asset allocation, so I wondered if those arguing for and against rebalancing were debating something that does not matter much.

Example

For this analysis I’ll use an example of a 35-year retirement that starts with $1 million of savings. I’ll assume variable retirement withdrawals based on RMD factors, and a target 60/40 stock/bond allocation.

I will use a Monte Carlo generation based on historical stock and bond returns, but with a downward adjustment to reflect my personal view about future returns. More specifically, I’ll use bootstrapped annual real returns (after inflation) by randomly selecting 20-year blocks from Ibbotson’s 1926 – 2019 data and subtract 4.85% from each of the stock returns generated and 1.95% from bond returns. The result is that arithmetic real returns will average 0% for bonds, reflecting current yields, and 4% for stocks, assuming a lower-than-historical equity premium. The purpose of using bootstrapped historical returns is to capture any correlation between stock and bond returns as well as any year-by-year correlation.

For each analysis, I generate 5,000 Monte Carlo simulations, but I caution that the end results are limited by the scarcity of historical data. Although there are 94 individual years of data between 1926 and 2019, that is less than three independent 35-year retirement periods. This points to the more general limitations in the use of historical data – there’s both the statistical significance of the data, and the question of whether historical financial relationships will persist into the future.

But I do the best I can with what I have.

To rebalance or not

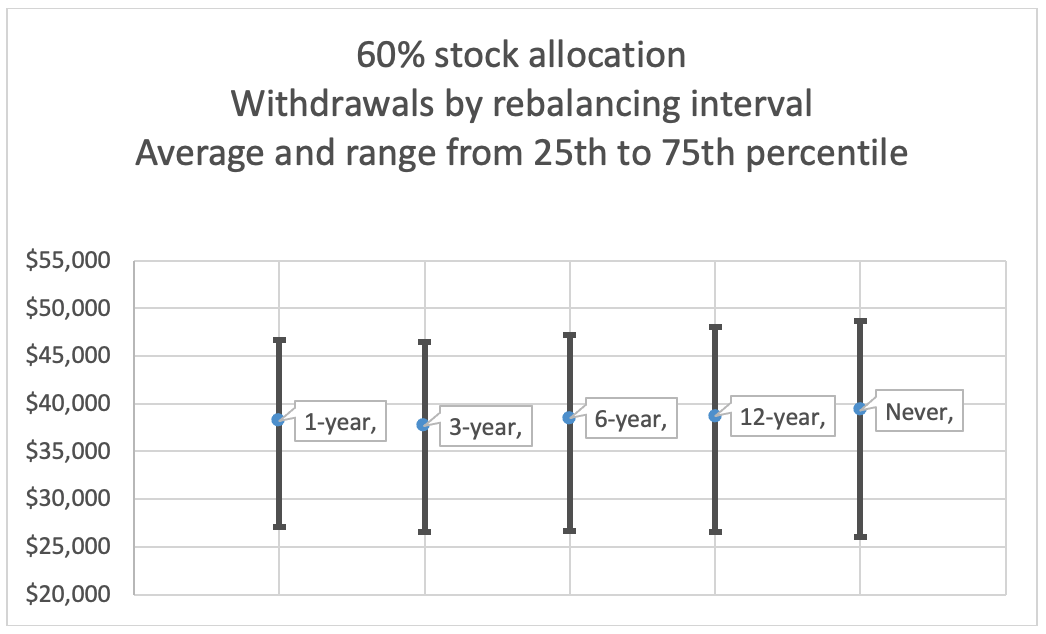

This first analysis compares results for regular periodic rebalancing versus buy and hold for the full 35-year retirement. Rebalancing intervals tested are one, three, six, 12 years and never, and the remaining savings are rebalanced back to a 60/40 stock/bond allocation at those intervals. Because I use annual data, it is not possible to rebalance more frequently than annually.1 Withdrawals are based on 1.25 times RMD factors, which produces reasonably level withdrawals over most of the retirement period with a 60/40 allocation.

For each of the 5,000 simulations, I calculate the average withdrawal over the 35-year retirement, and the chart below reflects the distribution of those averages. We end up with the 5,000 averages arrayed into percentiles, and the overall average of the 5,000 averages displayed as well.

What we see here is akin to the charts in my article mentioned earlier on asset allocation. Differences in average outcomes are tiny compared to ranges of potential outcomes. Since the ranges shown are for the 25th to 75th percentile, they only contain half the potential outcomes. The full range of possibilities is much wider.

In terms of discussion with a client, it could go something like, “If we rebalance to 60/40 every year, I’d expect your withdrawals to average $38,200, but with a 50% probability of this falling somewhere between $27,100 and $46,700, and an equal chance the range could be even wider. If we just let the portfolio run and never rebalance, things barely change– the average moves up to $39,300 and the range widens to $26,000 to $48,700.” Based on this presentation alone, one could understand the client responding, “It looks like a total crapshoot; we might as well go with not rebalancing.”

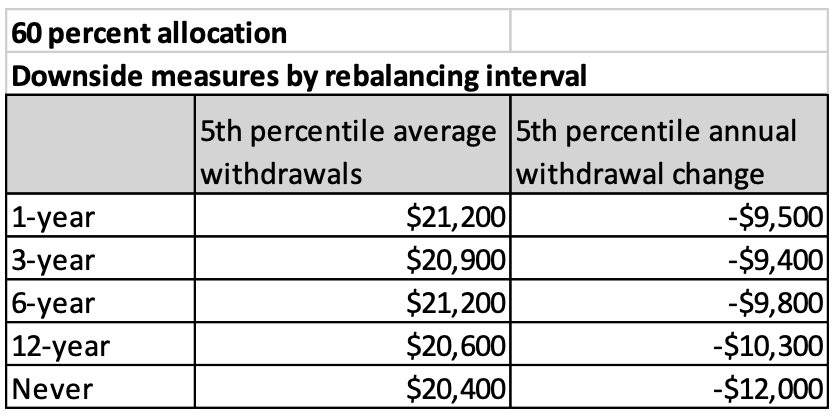

However, there is a risk side that may change the discussion somewhat. In the chart below I show a comparison based on two risk measures.

Here I display two downside measures. The 5th percentile average withdrawals portray a worst-case average akin to the 25th and 75th percentiles shown previously to represent the middle of the potential range. The withdrawal change column portrays the expected worst-case, year-to-year change in withdrawals. These two measures can be thought of as a layman’s utility analysis – a bad outcome would be low withdrawals that are volatile from year to year. There is slight deterioration in the 5th percentile withdrawals as we go in the direction of buy-and-hold, and a more adverse change in the year-to-year volatility. Having these downside risk measures might give some pause to going for the highest expected withdrawals via not rebalancing.

The results for both charts above reflect underlying changes in stock/bond mixes. Since expected returns are higher for stocks than for bonds, without rebalancing one would expect the stock allocation to increase over the course of retirement. Rebalancing, if any, resets the allocation at 60/40. With annual rebalancing in this example, the allocation remains at 60/40 throughout all simulated retirements. At the other extreme of no rebalancing, the allocation shifts to about 75/25 by the end of retirement, and averages about 67/33 over the course of retirement. Rebalancing, even at long intervals, holds down the allocation drift. For example, with rebalancing at six-year intervals, the average stock allocation is 61.7%, only a slight difference from the 60% target allocation, which explains why we don’t see much difference in outcomes for varying rebalancing intervals.

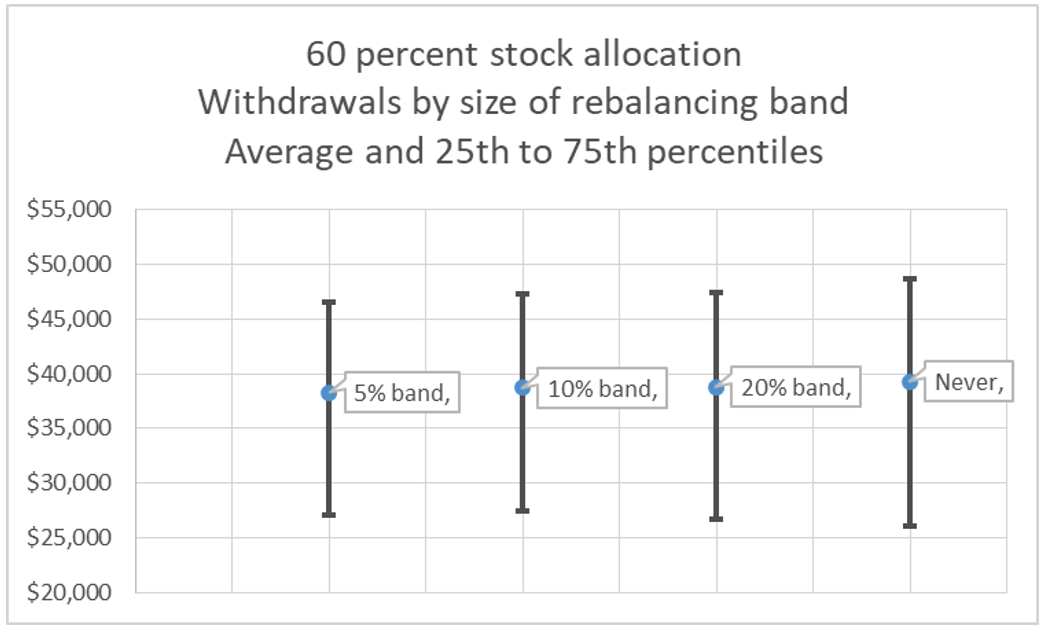

Percentage band rebalancing

Rather than rebalance at fixed intervals, another approach involves rebalancing only when the asset allocation drifts by a given percentage from target. The charts below are in the same format as the previous charts and show results for bands of 5% (e.g., 55% to 65%), 10% and 20% and for never rebalancing.

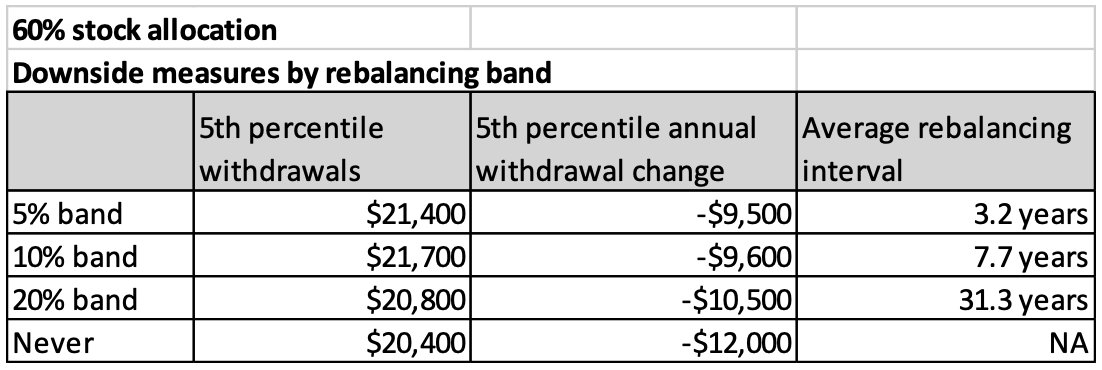

These results are similar to the previous analysis of rebalancing by fixed intervals in that the risk measures worsen slightly as the band size increases. The rightmost column shows the average rebalancing interval in years. Rebalancing based on bands may be more efficient than at fixed intervals. For example, using a 10% band requires rebalancing every 7.7 years on average, and results compare favorably with rebalancing at one-year and three-year fixed intervals. However, using bands requires more monitoring and may meet client resistance, particularly if the strategy calls for increasing the stock allocation immediately after a big stock market fall.

Discussion

At the beginning of this article, I speculated that rebalancing may not matter that much. After reviewing the evidence, this is indeed the case. The choice of rebalancing methodology doesn’t guarantee retirement success nor doom a plan to failure.

Getting into more specifics, loosening rebalancing to wider intervals or bands increases upside measures such as average withdrawals slightly but with a slight deterioration in the risk measures. But the rebalancing effects get swamped by investment return variability. As for the risk measures, the year-to-year volatility of withdrawals is more sensitive than the 5th percentile of average withdrawals.

As for practical implementation issues, the above results don’t make a case for never rebalancing. They support infrequent rebalancing, such as utilizing a 10% band. Such an approach would provide a means of getting back to the target allocation quickly when major stock market moves significantly disrupt the allocation. But, of course, there might be behavioral resistance from some clients. Infrequent rebalancing also holds down costs and fees associated with performing the rebalancing and reduces tax costs for taxable savings.

Additional comments

Below are comments about a few subtopics related to rebalancing that have surfaced in the recent APViewpoint discussions.

Other strategies

Besides constant-mix and buy-and-hold strategies, there are also constant proportion strategies where the dollar stock allocation is maintained at a constant multiple of the total amount of savings minus a floor value. Such strategies are related to what is known as “portfolio insurance.”

Strategies do better or worse under stock market trend behaviors. For example, constant mix does best in volatile sideways markets. Perold and Sharpe describe the performance characteristics of the various strategies in this paper, and there is also an article from Commonwealth Financial that provides a briefer comparison of performance characteristics.

Rebalancing bonus

This could also be labeled “diversification bonus.” If one combines multiple asset classes with returns that are not perfectly correlated (or even better, negatively correlated), the lack of correlation lowers the volatility of year-by-year returns compared to a single asset class with the same expected return. This reduction in the variance and standard deviation of returns has the further impact of increasing the compound or geometric returns. This Advisor Perspectives article by Adam Butler estimates the rebalancing premiums that may be achieved with a variety of risk-parity portfolios.

Regarding the rebalancing bonus and the bootstrapping approach I used, I also ran examples with Monte Carlo-generated returns that assumed zero correlation between bonds and stocks. These examples performed better on risk measures than those based on bootstrapping. It turns out there has been positive correlation between stock and bond returns over the 1926 -2019 period utilized for bootstrapping, so there would not have been as much diversification benefit as with the zero-correlation Monte Carlo modeling – hence bootstrapping’s worse results on risk measures. Over the past 20 years the correlation between stock and bond returns has turned negative. If this negative correlation continues it will be a plus for diversified stock/bond portfolios.

Rising equity glidepath

Various studies have shown performance benefits from a rising equity allocation glidepath over the course of retirement, selling bonds first, and from buy-and-hold. All such strategies involve increasing the stock allocation over the course of retirement, so they are variations on the same theme. Research studies have examined these strategies in the context of fixed withdrawals. Considerations are different with variable withdrawals such as using RMDs. A rising equity glidepath entails increasing year-by-year volatility of withdrawals with age – probably not a good fit for aging retirees.

Sequence risk

Some have asserted that rebalancing eliminates sequence risk. This is not the case. Poor investment performance when savings balances are the highest – late in the accumulation phase or early in the decumulation phase – is the essence of sequence risk, and such unfortunate timing is not eliminated by rebalancing.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England.

1 I did not study high-frequency rebalancing such as daily, weekly, or monthly. Some research, such as this Vanguard study have demonstrated little, if any, value to be gained from such high-frequency strategies.

More Fixed Income Topics >

The subject of rebalancing investment portfolios has generated much discussion as well as confusion among advisors and researchers. A recent example is the October 2020 Advisor Perspectives article by Michael Edesess, which has drawn more than 100 comments on APViewpoint. There are upsides and downsides associated with various rebalancing strategies (including the strategy of not rebalancing), and it’s important to look at the full picture. For this analysis, I’ll mainly focus on rebalancing versus buy-and-hold (not rebalancing) with a focus on retirement withdrawals. I’ll utilize Monte Carlo simulations and provide measures of benefits and risks.

The subject of rebalancing investment portfolios has generated much discussion as well as confusion among advisors and researchers. A recent example is the October 2020 Advisor Perspectives article by Michael Edesess, which has drawn more than 100 comments on APViewpoint. There are upsides and downsides associated with various rebalancing strategies (including the strategy of not rebalancing), and it’s important to look at the full picture. For this analysis, I’ll mainly focus on rebalancing versus buy-and-hold (not rebalancing) with a focus on retirement withdrawals. I’ll utilize Monte Carlo simulations and provide measures of benefits and risks.