Financial advisors routinely adhere to the discipline of rebalancing portfolios, so much so that they invest tens of thousands of dollars in software to automate the process. That adherence has been regularly reinforced by financial writers. I show why this conventional wisdom is wrong and rebalancing may be as unwise an investment as the software used to do it.

Financial advisors routinely adhere to the discipline of rebalancing portfolios, so much so that they invest tens of thousands of dollars in software to automate the process. That adherence has been regularly reinforced by financial writers. I show why this conventional wisdom is wrong and rebalancing may be as unwise an investment as the software used to do it.

I have had three articles on rebalancing published in Advisor Perspectives since 2014. The first was on April 15, 2014, on whether rebalancing adds to return; the second on April 22 of the same year, on whether rebalancing reduces risk; and the third and most comprehensive on August 16, 2016. Recently Bob Huebscher, Advisor Perspectives’ CEO, sent me several articles on rebalancing that had been published since that time by Morningstari, Michael Kitcesii, and Larry Swedroeiii. He suggested that I respond to them.

They all suffer from exactly the same defect.

Nothing to fear but fear itself

On March 4, 1933, in the depths of the Great Depression, U.S. president Franklin Delano Roosevelt uttered in his inaugural address the 10 words that comprise one of the most justly famous sayings of modern times: “The only thing we have to fear is fear itself.”

This saying was not only uniquely true at the time, it applies in many situations. We often fear something most because of the fear it will induce rather than the rational fear of actual harm.

For example, the fear can be great of a shark attack or a bear attack when a lover of the outdoors swims in the ocean or hikes in the woods. But the risk of death from a lightning strike is about 100 times greater than either of those risks. People may fear more the desperate panic they believe would be induced by a bear attack or a shark attack than they fear the risk of death itself.

Similarly, people with acute fear of flying are afraid of the panic that would grip them if the plane experienced violent turbulence. And yet the risk of turbulence is not the actual risk; it is, of course, the risk of a plane crash.

Articles that advocate rebalancing often suffer from a similar fallacy of misplaced concreteness. The real risk in investing is the risk of failure to achieve one’s financial goals. But what is identified as “risk” in all the articles on rebalancing cited above is not the risk of failing to achieve one’s goals, but the risk of “turbulence” – i.e. market volatility.

For example, in the recent Morningstar article titled, “Here’s Why You Should Rebalance,” the authors note that if an initial 60/40 stock-bond portfolio starting in 1994 were not rebalanced – i.e. if it practiced buy-and-hold instead – its equity allocation would have climbed to 76% in 2000 and to 73% in 2007. The article then notes, “the elevated allocations heading into the two bear markets of the past 20 years meant more pain during those drawdowns.”

Thus, the reason that the article gives for rebalancing is to avoid that pain. Rebalancing’s purpose is not to mitigate the risk of failing to achieve a particular desired financial goal, but to avoid the pain and panic of a possible market drawdown: i.e. “turbulence.”

In all of those articles on rebalancing risk is defined this way. Incredibly, none of the articles discusses or even considers the risk of failure to achieve the investor’s financial goals.

Defining investment risk the right way

What if we instead define risk to be the risk of failure to achieve financial goals? How then does rebalancing stand up against buy-and-hold?

We’ll analyze a simple example. Suppose a 35-year-old female named Chloe has $150,000 to invest. She plans when she reaches age 65 to supplement her Social Security by purchasing an annuity that will pay her at least an extra $10,000 a year for life.

Let’s say she starts with a 60/40 stock-bond mix. To keep it as simple as possible, suppose that she will not make any further contributions to her retirement-saving fund.

Will there be a greater risk of failure if she rebalances annually or if she buys and holds?

This question can be readily answered if we make some assumptions about the probability distributions of returns. Let us assume that the expected return on stocks is 7% with a standard deviation of 18% while the expected return on bonds is 2% with a standard deviation of 7%, and that there is no correlation between them.

According to immediateannuities.com, at the present time a $100,000 premium paid by a 65-year-old female buys an immediate life annuity of $5,376 a year. Let us assume that will be the premium required when Chloe turns 65, and that therefore, a $186,000 premium will purchase a lifetime stream of $10,000 a year.

What is the risk that Chloe will not be able to achieve her financial objective? What is that risk if she rebalances, and what is the risk if she uses a simple buy-and-hold strategy? And what are the chances she can do better than $10,000 – perhaps much better – if she rebalances versus if she buys and holds?

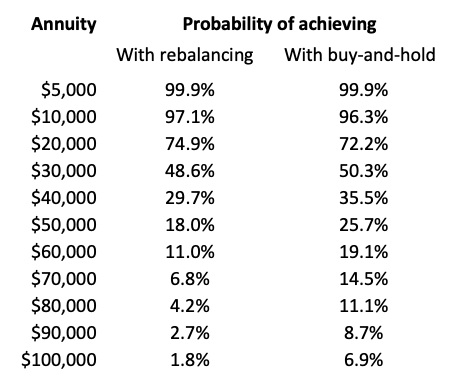

Probability calculations and Monte Carlo simulation yield the answers in Table 1 below.

Table 1. Probabilities of exceeding various levels of annuity after age 65

From this, we can see that the probability of achieving Chloe’s minimum goal of $10,000 extra income per year is very high if she either rebalances or practices buy-and-hold. The probability of achieving that goal is very slightly higher if she rebalances – 97.1% for rebalancing versus 96.3% for buy-and-hold, a negligible difference. And both provide a virtual certainty of at least $5,000 a year.

They both also provide about a three out of four chance that Chloe will realize additional income from her annuity twice as high as she hoped – $20,000 a year. The probability of this result is slightly higher with a rebalancing strategy than with a buy-and-hold strategy: 74.9% for rebalancing versus 72.2% for buy-and-hold.

In other words, rebalancing and buy-and-hold are neck-and-neck as to the risk of failing to achieve her minimum goal of $10,000 a year and are similarly close as to the chances of achieving twice that level of annuity.

But they depart markedly when it comes to the chances of a higher annuity. Buy-and-hold, for example, provides twice as much likelihood of an annuity of at least $70,000 a year and three times as much of at least $90,000 a year.

Is the trivially greater risk that buy-and-hold will fail to achieve the $10,000 minimum annuity, or the twice-as-great $20,000 sufficient to offset the substantially better chances of annual incomes much greater than that?

You be the judge.

Does risk increase when equity allocation drifts higher?

Those who admonish against rebalancing say that your “risk” will increase because your allocation to stocks may drift higher over time.

Let’s use the same framework to determine whether the risk of achieving your financial goals actually increases when your equity allocation drifts higher and you use buy-and-hold rather than rebalancing.

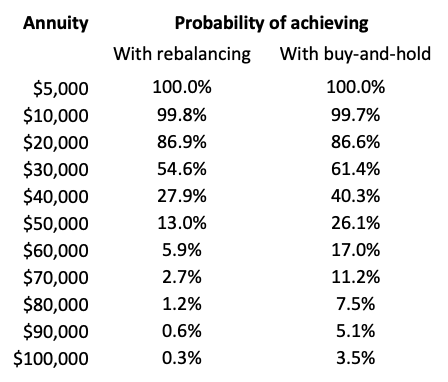

Suppose that after 15 years, when Chloe is 50, equity returns have been such that if she is using buy-and-hold her allocation to stocks will be 75% instead of the initial 60%. (This would have happened if equity returns averaged 6.82% and bonds 2%.) All of the articles cited above would say that she now has greater “risk” if she is buying and holding.

But let’s compare what the probabilities of meeting her financial goals at age 65 are now if she uses buy-and-hold as compared to rebalancing. Table 2 shows the results.

Table 2. Probabilities of achieving age-65 annuity levels if buy-and-hold equity allocation were to rise to 75% at age 50

Chloe now has no greater risk of failing to achieve her financial goals if she is practicing buy-and-hold than if she is rebalancing, and she has a much greater chance of gain. The probabilities are higher than in Table 1 because the returns have not been disappointing so far, thus reducing the chances of ultimate failure.

The probabilities that buy-and-hold will outperform rebalancing are now greater at almost every level – even though, as the six articles on rebalancing cited above would have it, Chloe’s “risk” has now risen to a dangerous level.

This example uses a specific set of input assumptions, but I believe that other assumptions will yield similar results.

Conclusion

Advising an investor to rebalance is like advising a traveller from Los Angeles to New York to drive rather than take a plane, because if you take a plane there is greater danger of turbulence. However, the risk to life is much greater if you drive, because the probability of a car crash is much greater than that of an airplane crash.

Many people believe rebalancing pays off because they confuse the past with the future. They think that because a security or an asset had a higher price recently than it has now, it will return to that higher price in the near future. But careful investigation of price patterns reveals that this is not true. The likelihoods of the direction the next price move will take – up or down – and its magnitude are independent of the direction and magnitude of the last price move. This mistaken intuition is not a valid justification for rebalancing.iv

Rebalancing should be dismissed as nothing but the poorly-examined conventional wisdom that it is – the plethora of articles in financial journals filled with largely irrelevant mathematics notwithstanding. The greatest damage done by this myth is that it helps to surround providers of financial advice with the aura of “knowing” something that they do not know at all.

Economist and mathematician Michael Edesess is adjunct associate professor and visiting faculty at the Hong Kong University of Science and Technology, chief investment strategist of Compendium Finance, adviser to mobile financial planning software company Plynty, and a research associate of the Edhec-Risk Institute. In 2007, he authored a book about the investment services industry titled The Big Investment Lie, published by Berrett-Koehler. His new book, The Three Simple Rules of Investing, co-authored with Kwok L. Tsui, Carol Fabbri and George Peacock, was published by Berrett-Koehler in June 2014.

i https://www.morningstar.com/articles/962396/heres-why-you-should-rebalance; https://www.morningstar.com/articles/988100/is-it-time-to-rebalance; https://www.morningstar.com/articles/990564/why-rebalancing-almost-always-pays-off

ii https://www.kitces.com/blog/best-opportunistic-rebalancing-frequency-time-horizons-vs-tolerance-band-thresholds/; https://www.kitces.com/blog/how-rebalancing-usually-reduces-long-term-returns-but-is-good-risk-management-anyway/

iii https://www.evidenceinvestor.com/a-strategic-approach-to-rebalancing/

iv But an academic justification under certain assumptions for rebalancing is contained in Paul Samuelson’s 1969 article “Lifetime Portfolio Selection By Dynamic Stochastic Programming.” It shows that for specified well-defined utility functions, utility is maximized by a constant “risk” strategy, i.e. in the portfolio management case, periodic rebalancing, where risk can be interpreted as stock-bond allocation. The same is shown for the continuous-time case in a companion article by Robert Merton, but its conclusion is contained in Samuelson’s article as the limiting case, and continuous rebalancing is a practical impossibility in any event. I have rarely seen either of these articles referenced in finance journal articles about rebalancing.

Read more articles by Michael Edesess

Financial advisors routinely adhere to the discipline of rebalancing portfolios, so much so that they invest tens of thousands of dollars in software to automate the process. That adherence has been regularly reinforced by financial writers. I show why this conventional wisdom is wrong and rebalancing may be as unwise an investment as the software used to do it.

Financial advisors routinely adhere to the discipline of rebalancing portfolios, so much so that they invest tens of thousands of dollars in software to automate the process. That adherence has been regularly reinforced by financial writers. I show why this conventional wisdom is wrong and rebalancing may be as unwise an investment as the software used to do it.