Earlier this year, Jeremy Siegel said that, “75/25 is the new 60/40,” a recommendation to raise stock allocations to make up for lower bond yields. However, what matters for investors saving for retirement is not the asset class performance, but how those returns translate into retirement consumption.

Earlier this year, Jeremy Siegel said that, “75/25 is the new 60/40,” a recommendation to raise stock allocations to make up for lower bond yields. However, what matters for investors saving for retirement is not the asset class performance, but how those returns translate into retirement consumption.

To examine the impact of increasing stock allocations, I’ll focus on retirement planning and show impacts on both the average and variability of retirement withdrawals.

Spoiler alert – as the title hints, 75/25 versus 60/40 doesn’t matter that much.

Background

The importance of asset allocation received a boost from the 1980s from a paper by Brinson, Hood, and Beebower (BBH), which many interpreted as “proving” that the key differentiator of pension plan performance was the stock/bond mix, and manager selection didn’t have much influence.1 In fact, BBH demonstrated that asset allocation explained the variability of the performance in the sample they studied, not the performance itself. More recently, with increased focus on index funds and passive investing, asset allocation has become a more prominent consideration as attention has shifted away from selecting active funds or individual stocks. Over the past few years, I have received questions from DIY investors trying to decide on the best allocation to target. Typically, they are trying to decide between relatively high stock allocations such as 60/40 versus 75/25, not 20/80 versus 30/70, and not wide differences like 30% stocks versus 100% stocks.

Example

I’ll use an example of a retirement-age couple with a 30-year planning horizon and $1 million in savings, trying to decide between 60/40 and 75/25. I assume that they have sufficient sources of sustainable lifetime income such as Social Security, pensions, or annuities so that they can comfortably take market risk, and I’ll focus the analysis on the savings portfolio.

A key assumption for modeling retirement outcomes is future average stock returns. The size of the assumed equity return premium (ERP) of stocks over bonds will directly impact the sensitivity of retirement outcomes to different asset allocations.

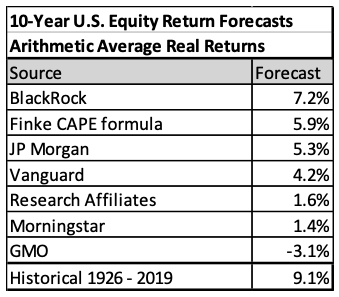

In January of this year, Christine Benz of Morningstar provided a summary of predictions for the next 10 years from various investment firms and research organizations. I show those in the table below expressed as real arithmetic average returns, which is the return definition I will use for Monte Carlo modeling. Besides the forecasts provided by Benz, I also include a CAPE-based forecast derived from Michael Finke’s recent Advisor Perspectives article, and I also show the historical average (1926 – 2019) for large capitalization U.S. stocks from Ibbotson/Morningstar.

These forecasts all assume lower than historical-average stock returns. These are forecasts for the U.S., and some of the forecasters also assume that higher equity returns may be found internationally and/or returns after 10 years may be somewhat higher.

The wide variation in forecasts reflects double uncertainty about the average equity premium to expect plus year-to-year return variability as I discussed in this 2015 Advisor Perspectives article. Bill Sharpe, in chapter 7 of his RISMAT book on retirement income, also discussed the uncertainty in future equity-return forecasting. He offered the insight that, based purely on a statistical view, estimation errors are smaller for second moments (standard deviations) than for first moments (means). He cautioned that, “When estimating future return distributions, humility is very much in order.”

For my analysis, I will use an estimated real arithmetic average equity return of 5%, but also include a separate analysis based on 7.5%, slightly above the most optimistic forecast above. I’ll assume a 16% standard deviation for stocks, based on Ibbotson/Morningstar data since 1980. For bonds, I’ll use a 1% real return with a 7% standard deviation. I’ll assume stock and bond returns are independent.

For this modeling, I’ll also need to select a particular method for taking withdrawals from retirement savings. There are numerous possibilities, but I’ll base withdrawals on scaled-up factors for required minimum distributions (RMDs). I’ve chosen 1.5 times RMDs because, based on testing, this multiple produces reasonably level average withdrawals over the bulk of the retirement period. This is important because I want to compare asset allocations in terms of withdrawal variability from year-to-year and avoid having those measures overly influenced by tilts in withdrawal patterns.

Results – 5% average equity return

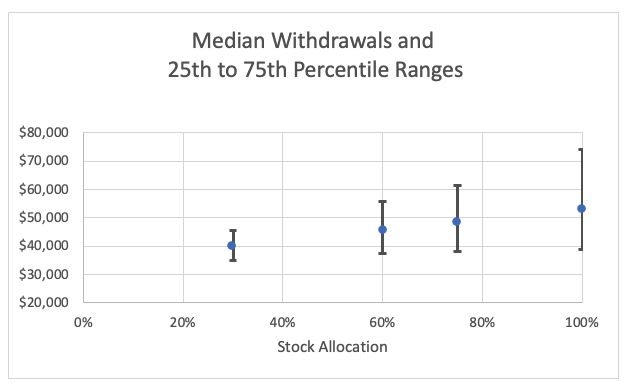

In the chart below, I show results for different asset allocations based on an average equity return premium (ERP) of 4% – a 5% average return for stocks minus 1% for bonds. Besides stock/bond allocations of 60/40 and 75/25, I also bracket these by showing results of 30/70 and 100% stocks. For each asset allocation, I ran 5,000 Monte Carlo retirement simulations, and for each simulation calculated the average annual withdrawal in real dollars over the assumed 30-year retirement period. I then calculated percentiles for the 5,000 withdrawal averages.

The chart shows the medians (blue dots) from the Monte Carlo runs plus the range from the 25th to 75th percentile. If a client were considering a 60/40 allocation, these projections would show median expected average real withdrawals of $45,600 and a 25th to 75th quartile range of $37,400 to $55,900. This range includes only half of the expected outcomes; there’s a 50% chance of average withdrawals either below $37,400 or above $55,900. There may be a tendency to focus on the median, but it’s more important to be aware of the wide confidence interval.

If we examine increasing the stock allocation from 60% to 75%, we see that median withdrawals increase from $45,600 to $48,300 and the 25th to 75th range is now $38,000 to $61,400. Again, this range covers only 50% of the possible outcomes. The key consideration in comparting 60/40 versus 75/25 is that the increase in the median (of less than $3,000) is swamped by a very wide 25th to 75th quartile range, and that range is only covering 50% of potential outcomes. It raises the question of whether it’s worth spending much time agonizing over 60/40 versus 75/25. On the other hand, the chart indicates that, if the client was trying to decide between 30/70 versus 100% stocks, it would be worth a careful examination of potential outcomes.

Withdrawal variability

A client trying to decide between 60/40 and 75/25 might look at these projections and conclude in favor of 75/25 because the chart shows upside but not downside potential – even the 25th percentile is slightly higher for 75/25. However, it does not consider the potential one-quarter of outcomes below the 25th percentile where low-probability, bad outcomes lurk. It also doesn’t consider the potential planning disruption caused by year-to-year variability in withdrawals. Since stocks have a higher expected variability in year-to-year returns than bonds (16% assumed standard deviation for stocks versus 7% for bonds), increasing the stock allocation increases the portfolio volatility, which in turn increases the year-to-year volatility of withdrawals. There may also be more nervousness with a higher stock allocation when the stock market takes a bad turn such as we experienced a few months ago.

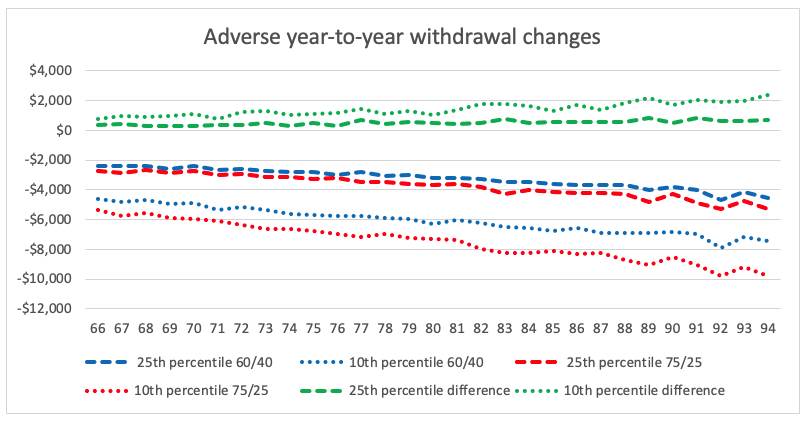

The chart below focuses on downside volatility and compares 60/40 to 75/25.

To build this chart, I calculated the year-to-year dollar changes in real withdrawals for each year in each of the 5,000 Monte Carlo runs for each allocation, and then plotted the adverse cases – 25th and 10th percentiles. At the top of the chart, I show the projected additional downside volatility from moving from a 60/40 allocation to 75/25. At the 25th percentile the additional average annual adverse change is $500 and this grows to $1,400 at the 10th percentile. There is some tradeoff in raising the stock allocation in terms of increasing the year-to-year volatility of withdrawals.

Results – 7.5% average equity return

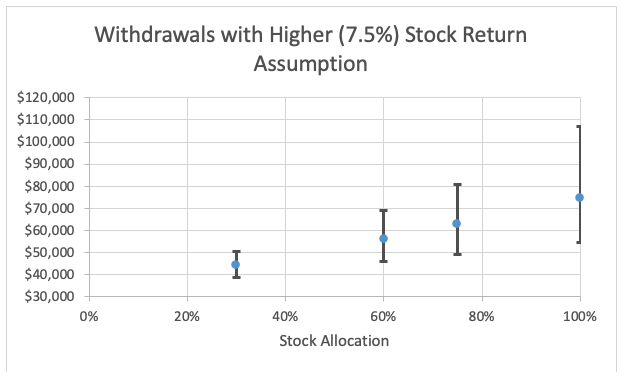

The following chart provides the distribution of average withdrawals based on a 7.5% average stock return substituted for my base case of 5%.

The increase in the median from 60/40 to 75/25 (from $56,000 to $62,400) is more than $6,000, compared to slightly less than $3,000 in my base case 5% stock return assumption. However, the differences still get swamped by the potential ranges of average withdrawals. If an advisor had good reason to believe in future stock returns significantly higher than my base case, there’s more of a rationale to fine-tune allocations. But the benefits are still questionable.

This casts doubt on the importance of asset allocation and raises related questions about rebalancing and the use of non-level asset allocation glide paths during retirement. If 60/40 versus 75/25 doesn’t make much difference, the allocation bouncing around or deliberately shifting within this range doesn’t matter much either. The wide variation of average withdrawal levels for either 60/40 or 75/25 highlights the importance a solid base of secure lifetime income to pay for essential expenses. Relying on stock-heavy portfolios to meet basic needs carries a lot of risk.

Taming the withdrawals

It could be argued that I have rigged my examples by choosing a withdrawal method based on current savings values that respond directly to underlying investment performance. There are other methods that either utilize fixed withdrawals or at least smooth out fluctuations in some way. As a counter example, I’ll change the withdrawal method to one where annual withdrawals are fixed in real terms at 2% of the initial portfolio, a real level $20,000 withdrawn each year from an initial $1 million portfolio. With such a modest withdrawal rate, the chances of depleting the portfolio within 30 years are minuscule, so ranges in the first chart above collapse to a single point at $20,000, and the year-to-year variability in the second chart goes to zero. I’ll use my base case stock return assumption of 5% for this example.

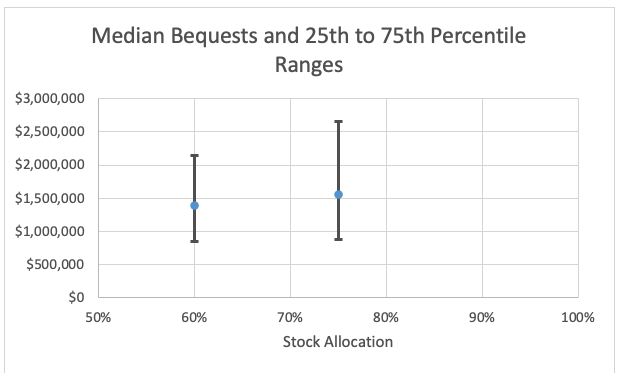

What does vary with this new withdrawal approach are the expected bequests at 30 years. The following chart shows ranges of bequests for 60/40 and 75/25 portfolios.

Again, raising the stock allocations increases in the median outcome, but that gets swamped by the range of possible outcomes. But in this case, it is for bequests rather than withdrawals. One should not get too excited about the increase in the projected median result, because there will be a very wide range for the eventual outcome. As a general rule, if we tighten up the potential range of one important variable, we push the uncertainty into a different important variable.

Pre-retirement

This example has been for a retired couple, but additional considerations come into play when considering the importance of asset allocation during the working years. It turns out that asset allocation becomes even less important, because there are additional levers that workers can use to build a secure retirement. A 2012 paper from the Center for Retirement Research at Boston College used a variety of approaches to assess the importance of various factors contributing to building a secure retirement. The findings were that the key determinants were the age for starting savings, the split between savings and consumption during the working years, and age at retirement. Retiring later was particularly important because of impacts on additional savings and time for savings to grow, increased Social Security benefits, and shortening of the retirement period. Tests of sensitivity of outcomes to even wide variations in asset allocations showed much less impact.

Conclusion

Most retirement research attempts to fine-tune decision parameters, whereas I point things in the opposite direction to asset allocation. For those targeting significant equity allocations, I’ve shown that the impact of fine-tuning the stock/bond mix gets swamped by the wide range of potential outcomes. To some extent, this result reflects an assumption of a lower-than-historical equity return premium. This study also highlights that high equity allocations go hand-in-hand with significant uncertainty in retirement cash flows, and highlights the importance of a secure base of sustainable lifetime income to support essential expenses. There are many ways advisors can provide value for clients other than focusing on asset allocation.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England.

1 This 2017 Advisor Perspectives article by Michael Edesess raises questions about the Brinson et al. paper and the importance of asset allocation, although with quite a different focus than I provide in this article.

Read more articles by Joe Tomlinson

Earlier this year, Jeremy Siegel said that, “75/25 is the new 60/40,” a recommendation to raise stock allocations to make up for lower bond yields. However, what matters for investors saving for retirement is not the asset class performance, but how those returns translate into retirement consumption.

Earlier this year, Jeremy Siegel said that, “75/25 is the new 60/40,” a recommendation to raise stock allocations to make up for lower bond yields. However, what matters for investors saving for retirement is not the asset class performance, but how those returns translate into retirement consumption.