“For a time, while confidence lasted, an impetus was given to trade which could not fail to be beneficial... The looms of the country worked with unusual activity to supply rich laces, silks, broad-cloth, and velvets, which being paid for in abundant paper, increased in price four-fold. Provisions shared the general advance. Bread, meat, and vegetables were sold at prices greater than had ever before been known; while the wages of labour rose in exactly the same proportion. The artisan who formerly gained fifteen sous per diem now gained sixty. New houses were built in every direction; an illusory prosperity shone over the land, and so dazzled the eyes of the whole nation, that none could see the dark cloud on the horizon announcing the storm that was too rapidly approaching.”

Charles Mackay (1814 – 1889)

English poet and author

Excerpt describing the Mississippi Scheme

Memoirs of Extraordinary Popular Delusions and the Madness of Crowds

The forceful rise of the markets from March depths continued in the fourth quarter. After stalling out in early Fall, market participants floored the accelerator in November with vaccine approval in tow and the election overhang in the rearview. November finished among the top ten all-time best months for the stock market. From the March lows, the S&P 500 Index of large company stocks, the Russell 2000 Index of small company stocks, and the tech-heavy Nasdaq Composite were up 71%, 94%, and 104%, respectively. Average yields on high yield bonds exceeded 11.0% in March. Today they are sub-4.5%, a new all-time low.1

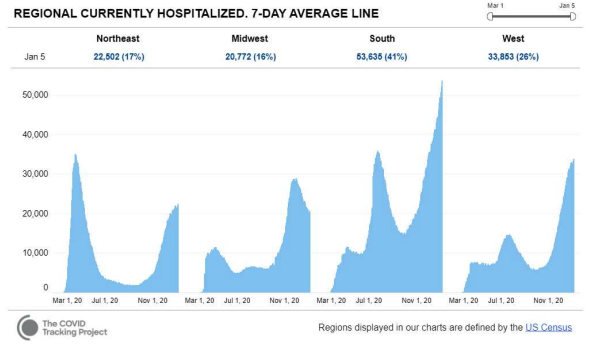

And yet, here in January of 2021, the world finds itself in a dramatic and deadly race against time and the novel coronavirus. The CDC reports the U.S. is on track for 400,000 more deaths in 2020 than the 2.8 million experienced in each of 2017, 2018, and 20192. This sobering figure is more than a statistic; it represents the loss of friends and family members. And we are not out of the woods yet. Studies indicate at least three to four times more people would need to catch the virus before it would burn itself out naturally. Coupled with exploding case counts and overburdened healthcare systems, this makes for some dark math.

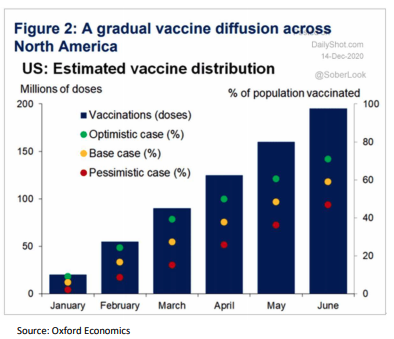

On the positive side, the impressively effective Pfizer and Moderna vaccines have been approved and are (slowly3) being administered. More help is on the way: approval for the Oxford vaccine is on the doorstep and the much-easier-to-administer Johnson & Johnson version awaits anticipated study results this month, with approval hopefully following the next.

New, more infectious strains of the virus are in the U.S. and social distancing fatigue is percolating. Perhaps the recent “surge on a surge” should not come as a surprise. Which will be the first to make it into the bodies of the remaining 250 million-some Americans - the virus or the vaccines?

While rollout of the first vaccines has been less than flawless, we still have our money on the vaccines. We are in the darkest days of the pandemic right now... which is another way to say we are about to turn the corner. Our secret weapon is vaccinating the oldest and most vulnerable people first, which should lead to a significant drop in mortality and hospitalizations4. As one example, nursing home residents represent only half a percent of the U.S. population but one-third of COVID deaths. Our previous forecast, that daily life will be 90% normal virus-wise in the 3rd quarter of 2021, is looking pretty good and may even prove to be slightly pessimistic5.

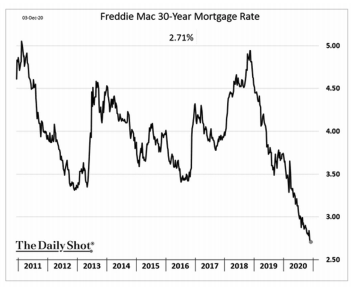

Stocks and other financial assets are looking past the virus and generally soaring. But are Americans really thriving financially? It depends on which arm of the K-shaped economic recovery you reside. Early in the pandemic there was much debate over whether the recovery would be V-shaped (quick), Nike’s “swoosh”-shaped (slow), or L-shaped (non-existent). A grossly uneven economic recovery is the reality. The upper arm of the K is doing better than ever; these are the white-collar workers who kept their jobs, safely telecommuted, received stimulus and saved money on dining out. As mortgage rates fell, they watched the value of their homes rise and refinanced their mortgage payments lower.

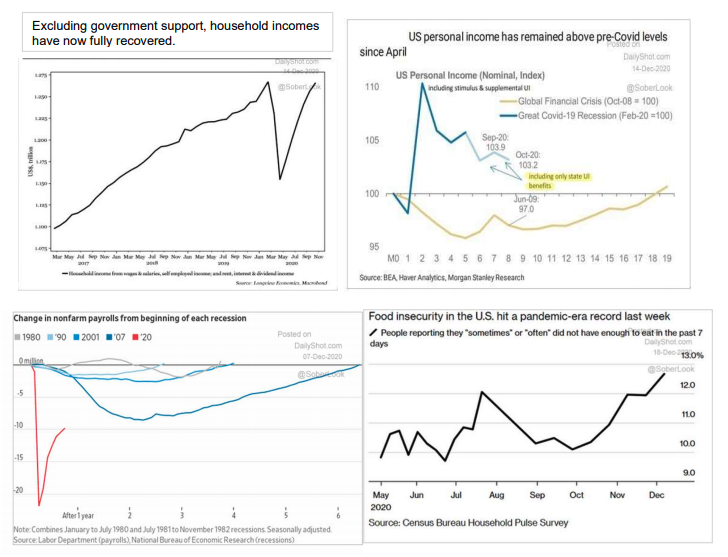

Meanwhile, the in-person service workers who either lost their jobs or were considered “essential” and had to report to work and maybe got sick, reside in the lower arm of the K. Most of these individuals are renters who do not own stocks and thus do not benefit from rising markets. On average, Americans are doing fine economically. Overall income levels, even before government transfers, are back to their pre-virus peak6. However, this income is not at all evenly split because so many people are unemployed (still more than at the worst point of the Great Recession). You’re either in the upper arm or lower arm of the K.

The asset-owning classes have benefited as the Fed buys $120 billion dollars’ worth of bonds each month7... but is that really helping the one in eight Americans who are food insecure? November, a banner month for the stock market, also saw the largest annual increase in poverty since the 1960s. One in eleven Americans are not current on their rent or mortgage or don’t know how they will pay their next bill8.

Businesses are experiencing a Kshaped recovery as well. Large national businesses, with ready access to capital and resources to deal with the complexities of 2020, are doing just fine. Small businesses are shuttering left and right. This is one reason why stocks can thrive while the economy falters: the stock market is dominated by very large enterprises.

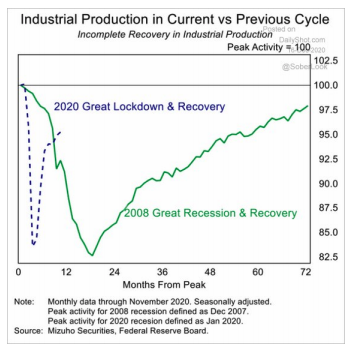

Still, the economy writ large should continue to rebound. Real GDP growth forecasts for 2021 are near 4%. The populace is tired of sheltering-in-place. Pent-up demand from the upper K-branch should enable the travel and leisure industries to bounce back quickly and re-hire heavily9. Manufacturing activity surveys (always a great leading indicator) are supportive. And yet, none of these developments can fully justify what has happened in the markets.

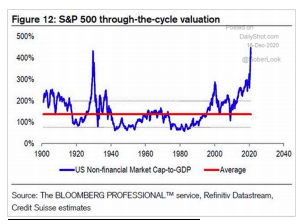

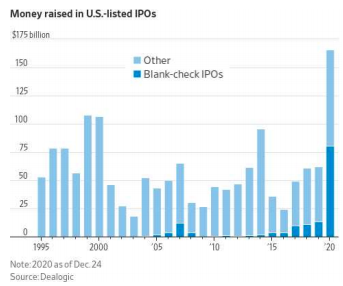

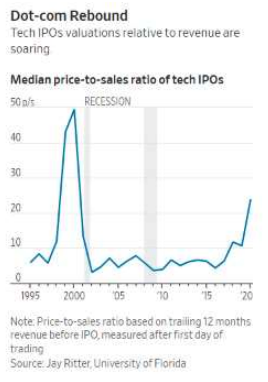

Questionable enthusiasm is driving soaring valuations in many corners of the market (see chart to the left 10). For brevity, we will focus on Initial Public Offerings (IPOs). The aggregate value of businesses being sold to the public has exploded. Owners want to sell their companies (IPO) when the market is hot and they’re likely to get a good price.

A number of quarters ago we wrote that private markets were frothy, while the more sober public markets had humbled some highflying “unicorns”, such as WeWork. Hundreds of billions of dollars of money-printing and bond-buying by the Fed has reversed the situation. Note the large volume of “Blank-check IPOs”, more commonly known as “SPACs11”. A SPAC investor gives a “blank check” to a SPAC sponsor, who then buys a company. The SPAC sponsor typically gets ten to twenty percent of the company for free. Why give away so much? The answer is that a traditional IPO takes a year or more to execute, whereas with a SPAC, you can sell your company now. Apparently, many owners think waiting a year might cost them far more than ten to twenty percent.

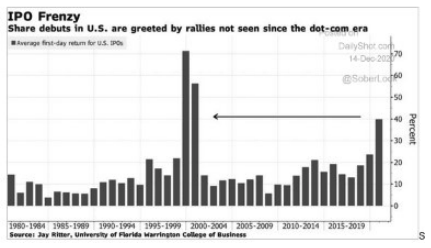

IPOs are recording wild first day gains, leaving them with valuations not seen since the dotcom era. Take AirBNB, which, after it debuted, was worth more than Marriott, Hilton, and Hyatt put together. Decade-old data mining company Palantir, which has never turned an annual profit, traded at 50 times revenue following its direct listing. Not impressed, cloud data company Snowflake came public at a valuation of 200 times revenue. These are extreme examples, but the average tech IPO came to life last year at 23.9 times revenue (compared to six times revenue for most of the past decade). All this reminds us of what former Sun Microsystems CEO Scott McNeely said about his own company in 2002 after the dotcom bubble burst:

“At 10 times revenues, to give you a 10- year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

How quaint.

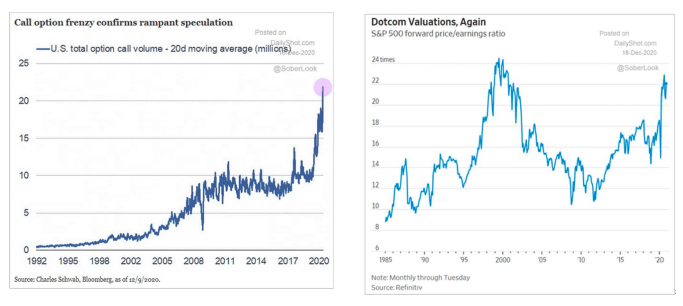

Perhaps more troubling than all these charts and data is that we are now receiving unsolicited stock tips from strangers. Evidence is mounting that new retail traders are driving the market higher. Fidelity said trading volumes rose 97% in the third quarter. We were blown away when shown just how easy and “gamified” it is to trade options on Robinhood12.

Options are an absolutely incredible way to magnify returns when you’re right and incinerate money when you’re wrong. To be fair, anyone brand new to trading probably has outperformed us. In a bubble, it is the most reckless that do the best on the way up.

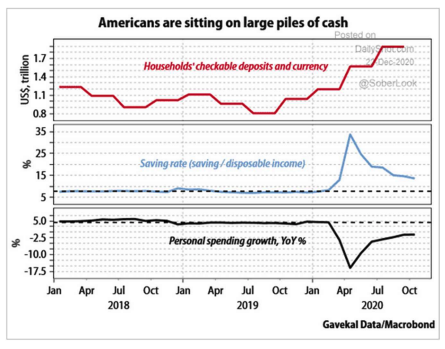

So what are the implications? Sell everything and head for the hills? No. We could be in the early innings of the advance. Valuations are high but not at dotcom levels yet... and there is no reason they need to stop there13. Things can always get more extreme. Recent stimulus checks will probably add fuel to the fire. Note the chart to the right which shows very high levels of household deposits and currency which can be used to push asset prices higher via additional purchases. It can still make sense to invest in assets that are overvalued as long as expected returns are above zero (i.e. better than the alternative of cash). This is where we believe we are today.

Asset prices have risen and we feel richer. We enjoy Trump’s tax cuts while the government increases spending and even gives money back to us. Are we all better off than before the virus? Is there more wealth to go around? No. When millions are out of work, not creating value, it represents real wealth destruction. We must incur new costs just to live life like we used to. We are cloaked in an illusion of wealth. It is an illusion of prosperity. For example, stimulus check recipients feel richer, unaware that the increase in government debt offsets this by making them poorer. The illusion will likely continue and intensify. But don’t be taken in; don’t go crazy spending. Be conservative with your gains. Don’t expect endless annual double-digit returns. The illusion of prosperity will eventually deflate to reality, whether from higher taxes, lower asset values, persistent inflation, long periods of insipid returns, or some combination of the four.

We believe lower (though not necessarily negative) investment returns are in store. Stock market earnings have not increased spectacularly. We’ve all just collectively “decided” we’re going to pay more for them. With bonds, the lower returns are more explicit – interest rates are simply lower than in decades past. Bonds can temporarily soar if interest rates head lower still... but ultimately the return experienced is somewhat limited by the return promised.

It’s our job to help you navigate these challenges, and we will bring all our skills and abilities to bear in this task. It is also our job to act as your financial enthusiasm dampener – to buoy you up when markets are dour, and to bring you back to earth when exuberance becomes irrational. Today is a time for the latter.

We thank you for the continued trust you place in us.

Sincerely,

John G. Prichard

Miles E. Yourman

Kurt Beimfohr

Jeff Vieth

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 Bond yields move inversely to bond prices. The high yield bond index also finished 2020 at an all-time high.

2 This “excess deaths” figure is one of the best measures of loss of human life due to the virus, as it cuts through arguments about deaths being mislabeled as COVID related. The bottom line is clear: more people are dying. Tallies of excess deaths routinely exceed official counts of COVID deaths.

3 Less than five of the planned 20 million vaccinations were actually administered by year-end.

4 Focusing only on deaths and hospitalizations is a simplification which ignores that many COVID 19 survivors suffer long-term effects.

5 As the pandemic fades into the rearview mirror, perhaps the question of how it arose in the first place will be given greater attention. The possibility that it arose as a lab accident from well-meaning scientists is one that deserves serious consideration: https://nymag.com/intelligencer/article/coronaviruslab-escape-theory.html

6 Incomes are above pre-crisis levels when government payments are considered.

7 For comparison, the total bill for last year’s much talked about direct stimulus checks to regular people was $166 billion. Small business owners will receive up to $284 billion in second round PPP grants. These are one time, not monthly, figures.

8 The federal moratorium on evictions, set to expire in December, got pushed back again. The eventual re-imposition of evictions and foreclosures will surely have an impact on housing valuations.

9 We may finally see inflation when everyone is free to spend again. This might signal the end of the stock market party and we will be watching closely.

10 While the chart is indeed worrisome, there are some “good” reasons why stock market capitalization to GDP ought to have risen: there are more public companies, lower interest rates do justify higher valuations to a certain extent, and over time a greater percentage of S&P 500 revenues have come from abroad and thus aren’t directly tied to U.S. GDP.

11 Special Purpose Acquisition Vehicles.

12 Follow this twitter link to witness this incredible journey yourself https://twitter.com/petershk/status/1344286419380916228?s=20

13 This chart is a little unfair because today’s forward earnings estimates are understandably, temporarily depressed given the ongoing pandemic. This somewhat artificially inflates the above P/E.

Read more commentaries by Knightsbridge Asset Management