As shareholders rush to pull money from private credit funds over troubling questions about software exposure, opaque loan values and non-payments, some bond investors are doing the opposite: buying their debt.

For more than four decades, PIMCO’s Secular Forum has provided a disciplined framework for stepping back from short-term market noise to assess the structural forces that will shape the global economy and markets over the next five years. Yet rarely has this exercise been more consequential than it has recently.

Equity issuance is all the rage. The SpaceX (SPCX) IPO on Friday, Alphabet’s (GOOGL) up-sized secondary announced last week, and a slew of other major go-public names over the remainder of 2026 (Anthropic, OpenAI) buck the years-long trend of intense buybacks and shareholder-friendly activities by the world’s most valuable companies.

All major U.S. stock indices fell last week, ending a remarkable run of nine straight weekly gains for the S&P 500. But the headline numbers hide an unusually lopsided story.

Attractive yields and strong credit fundamentals are setting the municipal bond market up for a solid second half of the year, said Paul Malloy, the head of municipals at The Vanguard Group Inc.

Begin with the print itself, because the headline flatters the internals only slightly. The bulk of May's gains came from leisure and hospitality, which added 70,000 jobs, nearly half of them in food services and drinking places; local government contributed 55,000, health care 35,000, and manufacturing a modest 7,000, while financial activities actually shed positions.

LPL Research analyzes bond markets as yields rise, exploring Fed policy expectations, inflation trends, and whether bad news is already priced into Treasuries.

Equity markets should remain supported by strong earnings and capital investment trends through 2026, but market concentration and macro risks leave less room for error.

The takeaway for both HY and EM corporates is straightforward. Once oil prices are above breakeven, further moves in oil tend to matter less for credit performance.

Investors have enjoyed a favorable run. If the year ended today, it would mark the seventh time in the last nine years that stock portfolios generated double-digit returns. Housing prices remain near historic highs, while bond investors have benefited from elevated yields over the past three years.

Interest rates remain one of the primary concerns for investors as Kevin Warsh has officially assumed leadership at the U.S. Federal Reserve (Fed). While we believe the possibility of a rate cut has diminished considerably, we are not yet expecting additional rate hikes.

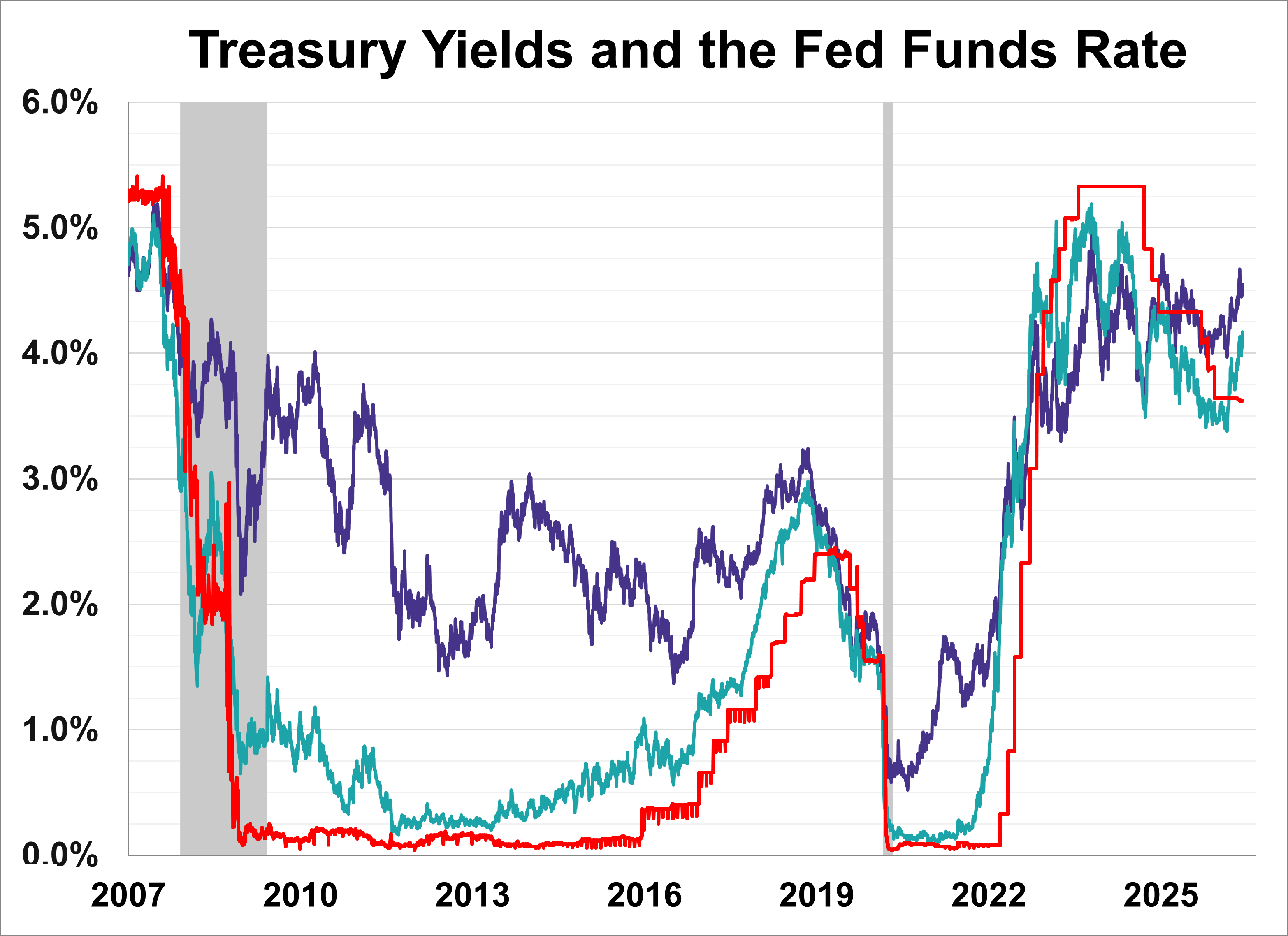

The rise in US yields has extended across the entire Treasury curve, creating a charged backdrop for Fed policymakers and their new chairman, Kevin Warsh, who helms his first meeting and press conference next week.

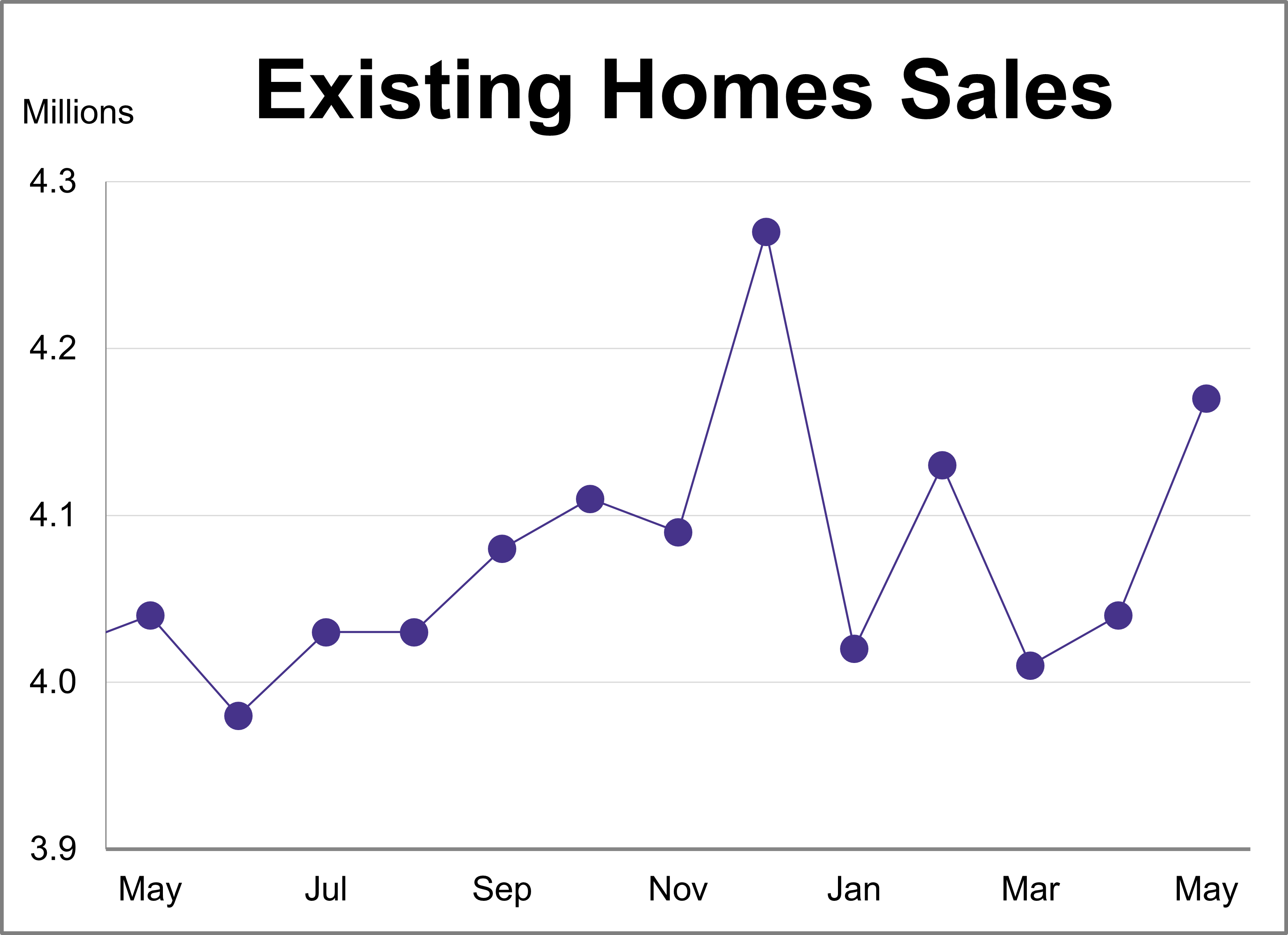

Existing home sales reached their highest level of the year in May, rising 3.2% after a 0.7% increase in April. According to the National Association of Realtors (NAR), sales reached a seasonally adjusted annual rate of 4.17 million units, surpassing the projected 4.07 million.

In case you’ve been living under a rock for the past few months, three of the world’s largest and most consequential private companies—SpaceX, Anthropic and OpenAI—are preparing to go public in the same year. Together, they could add nearly $4 trillion in market cap to public markets.

As we go to press, fighting in the Mideast has escalated, sending crude higher, but stocks, in early Monday trade, have shown remarkable stability following Friday’s deep selloff.

Chris Galipeau and Taylor Topoussis discuss high-conviction insights that go beyond media headlines.

Our broad message for the second half of 2026 is this: Income still matters, but investors should be selective. Despite the recent rise in Treasury yields, we suggest investors favor a below-benchmark average duration with their bond holdings, favoring short- and intermediate-term maturities.

The U.S. labor market took center stage last week as three major labor market indicators outperformed forecasts. Robust payroll additions in both the public and private sectors, paired with a massive surge in job openings, point to a workforce on solid footing.

On June 4, Vanguard launched the Vanguard U.S. High-Yield Corporate Bond Index ETF (VCHY) on the Cboe BZX. VCHY provides ultra-low-cost exposure to higher-yield U.S. corporate bonds. It comes with an expense ratio of just five basis points.

The yield on the 10-year note finished June 5, 2026 at 4.55% while the 2-year note ended at 4.17%, its highest level since February 2025.

Bond ETFs secured a record $64 billion in monthly inflows, driving total fixed-income ETF assets above $2.5 trillion.

There are short duration bonds and corresponding ETFs. For advisors and fixed income investors who really want to minimize interest rate risk, there are ultra-short alternatives. Those products are worth considering this year.

The stock market keeps setting records. Bitcoin has minted millionaires. Gold has peaked at new levels. Yet one of the most popular trades is to sit in cash or, more precisely, money-market funds.

As a symbol of economic vibrancy and opportunity, it’s hard to beat the public market. Its storied venues, where everything from butter to trillion-dollar tech companies are bought and sold, are a foundation of the modern world.

The rise in U.S. Treasury (UST) yields, specifically the ten-year note, since late February has captured the attention of global investors in a very visible fashion. Just a couple of weeks ago, headlines were blaring that the UST 10-year yield had reached its highest level since the beginning of 2025, leaving market participants to wonder: What comes next?

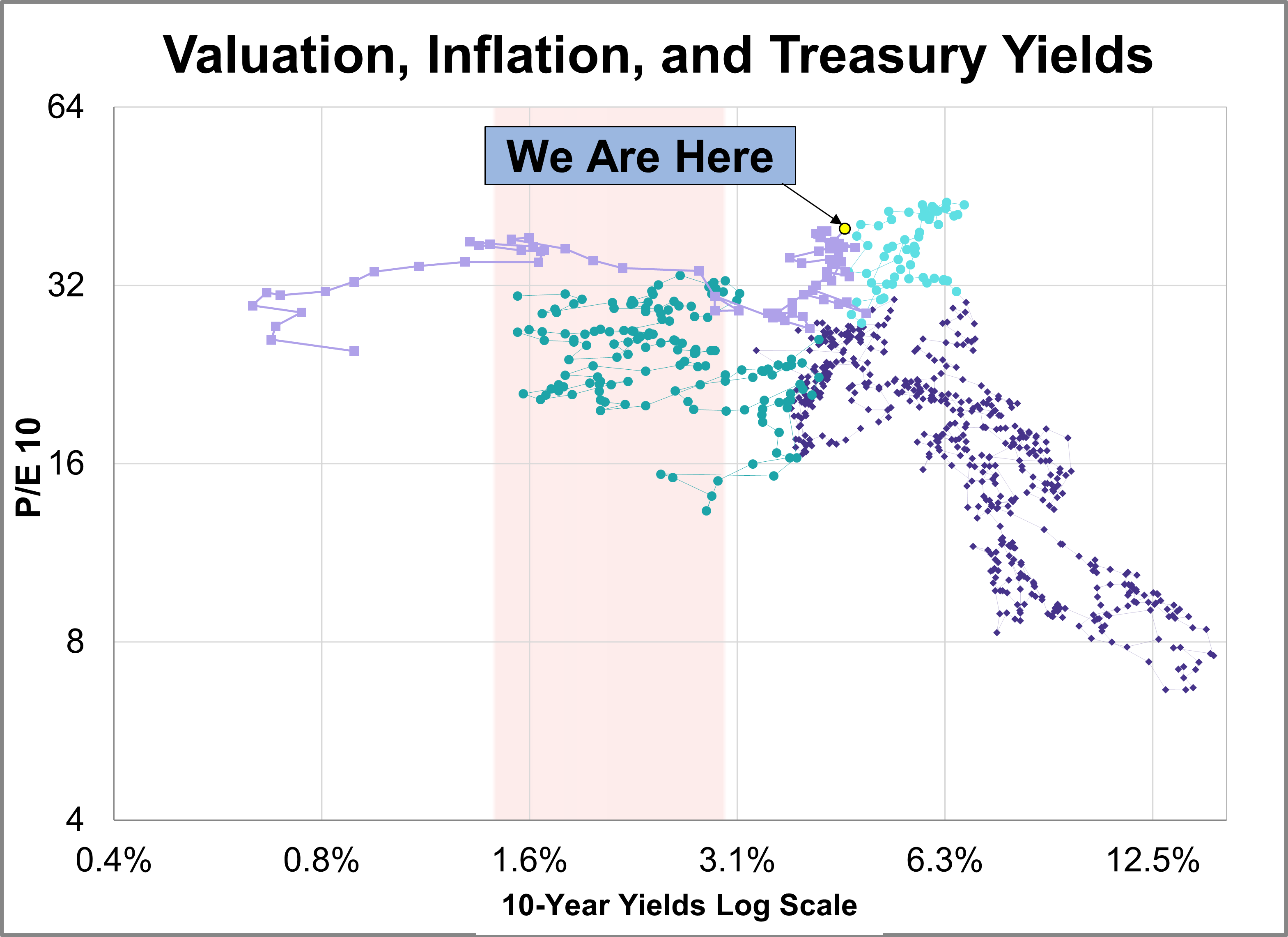

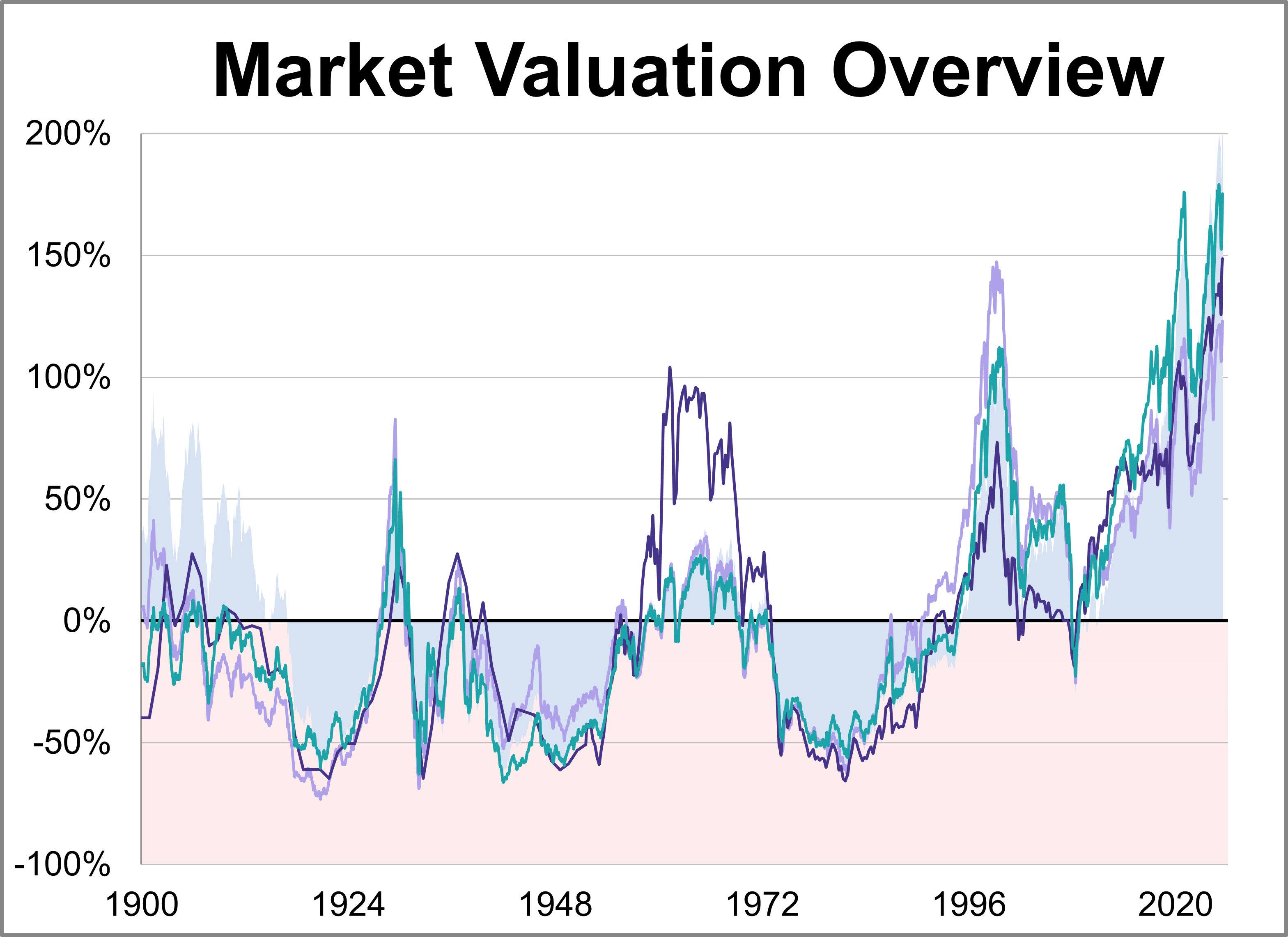

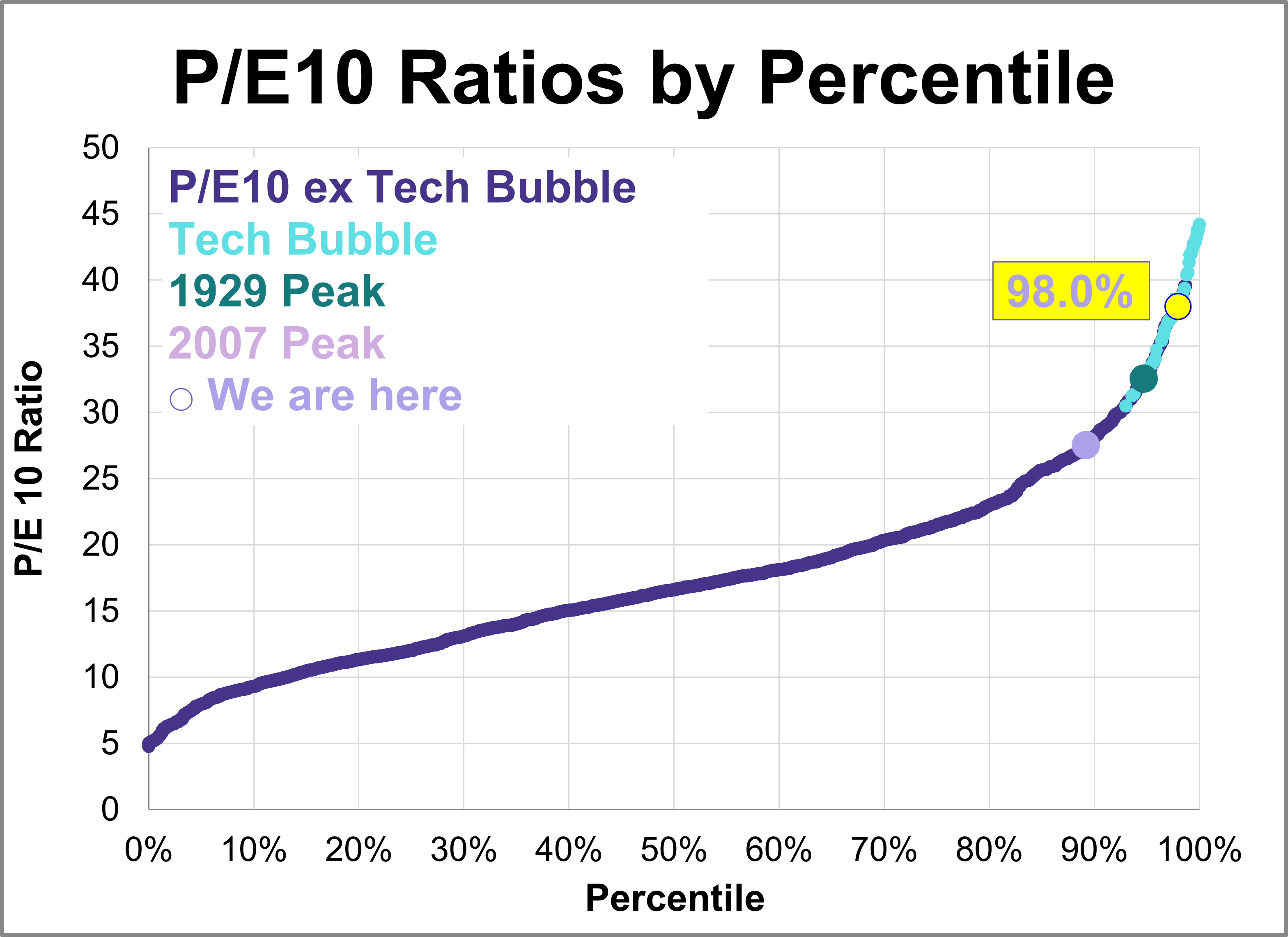

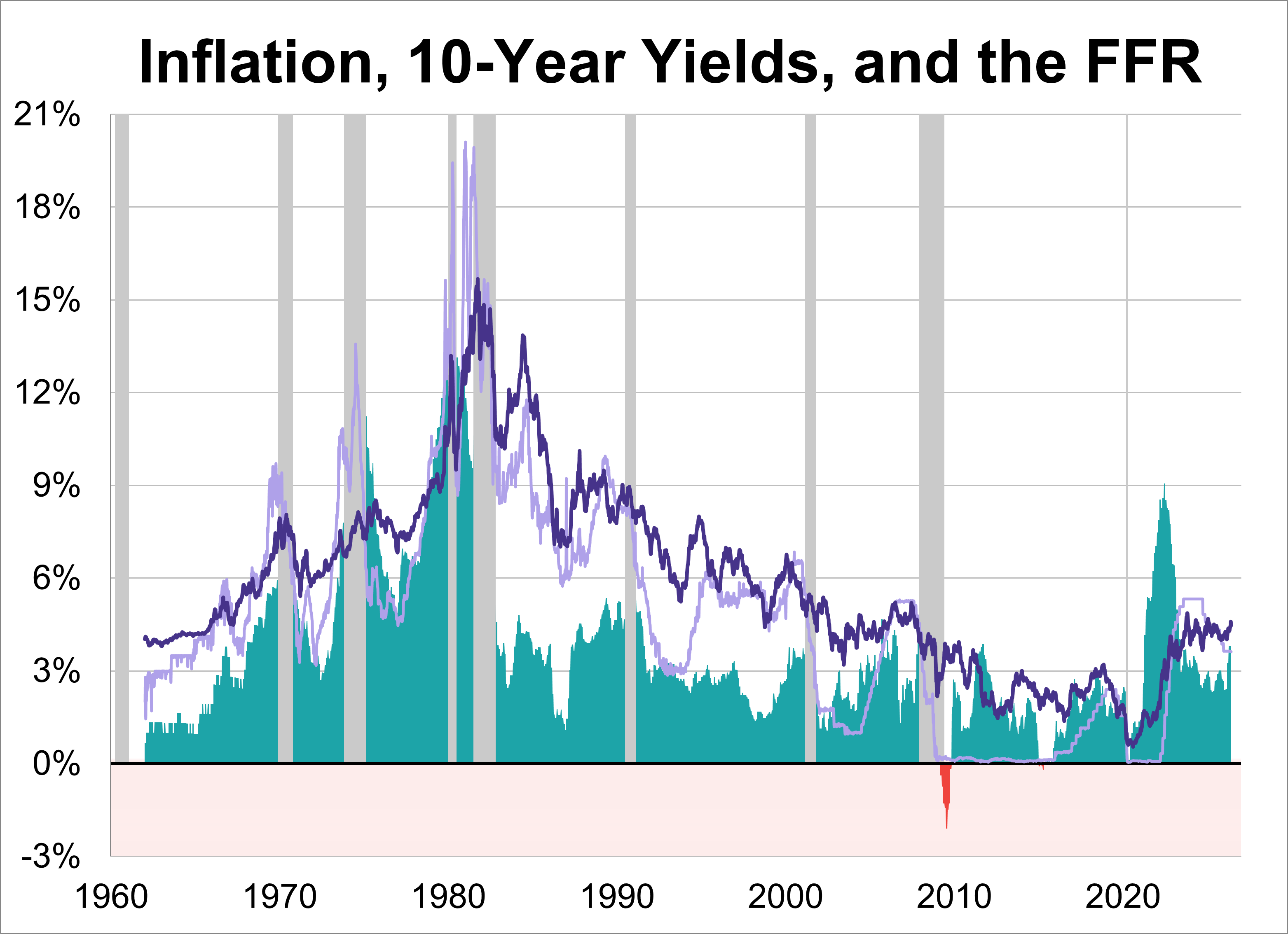

Our monthly market valuation updates have long had the same conclusion: US stock indexes are significantly overvalued, which suggests cautious expectations for investment returns. This analysis focuses on the P/E10 ratio, key indicator of market valuation, and its correlation with inflation and the 10-year Treasury yield.

Despite rising global yields and renewed inflation concerns, equities moved higher in May on the back of a strong US earnings season and continued momentum in AI-related stocks. The tech-heavy Nasdaq Composite gained 8.4% for the month, while the S&P 500 rose 5.3% and the Dow Jones Industrial Average was up 2.9%.

Emerging markets offer important exposure to economic growth through rapid industrialization, natural resource endowments, and strong demographic dynamics.

Even if the Middle East war does find a lasting settlement, the specter of inflation appears poised to hang over the markets. Indeed, while employment data had, up until recently, been the primary focus for investors, arguably, inflation reports have now moved into the ‘leaderboard’ position.

Learn what's in store for the remainder of 2026 and the challenges that lie ahead in our mid-year outlook for U.S. stocks and the economy.

Space ETFs have seen strong inflows coupled with standout performance, capturing significant market attention. For investors, the rapid pace of capital deployment into the space economy underscores a compelling investment opportunity. For this edition of Bull vs Bear, writers Zandile Chiwanza and Elle Caruso Fitzgerald debate the use cases for space ETFs in portfolios.

A key source of demand for corporate bonds may be fading now that managers of company pension funds have more than enough money on hand to pay their retirees.

For the dollar-denominated investor weighing how to position for the back half of 2026, last week tightened a thesis we have been building all year.

Would I be better off waiting for the Fed to make its move on rates before investing?” “Should I wait to increase duration because a blocked Strait of Hormuz could push oil prices higher and push rates even higher?” “Should I invest in bonds gradually to reduce the risk of missing the rate peak?

Taylor Topoussis and Chris Galipeau discuss high-conviction insights that go beyond media headlines.

LPL Research analyzes stock valuations, finding them fair given growth, rates, inflation, and AI-driven earnings outlook despite risks.

AI is a transformative technology with both near-term and long-term implications for the economy. For investors, while the debt-funded AI buildout has the potential to become a secular driver of risk premia, we believe any such shift would only play out through a multi-year adjustment and would not override the cyclical forces that affect markets.

May’s 5.3% S&P 500 gain masked a deeply uneven market: technology surged 16% on AI spending momentum while most sectors declined, and a surprise inflation rebound flipped the Fed narrative from cuts to potential hikes.

Here is a summary of the four market valuation indicators we update on a monthly basis.

As advisors, our role is not to solve fiscal policy; it is to ensure our clients are positioned to weather the uncertainty that comes from that gap, stay committed to their long-term plans, and not let macroeconomic anxiety drive short-term decisions they will regret.

Here is the latest update of a popular market valuation method, Price-to-Earnings (P/E) ratio, using the most recent Standard & Poor's "as reported" earnings and earnings estimates, and the index monthly average of daily closes for the past month. The latest trailing twelve months (TTM) P/E ratio is 25.9 and the latest P/E10 ratio is 39.9, the highest level since 2000.

Caution has become the most expensive position on Wall Street. A hot inflation reading this week — sending the annual gauge to its highest in about three years — landed alongside fresh strikes in the Persian Gulf and enduring expectations that the Federal Reserve may need to keep policy tight.

Investors are pouring money back into municipal bonds as higher yields and the approaching summer reinvestment season draw cash into the tax-exempt market.

The market continues to demonstrate remarkable resilience. Lower oil prices, easing Treasury yields, and the relentless buildout of artificial intelligence infrastructure are still providing a favorable backdrop for risk assets.

Economies around the world aren’t just reliant on AI investments for growth. The appreciation of AI stocks has supported spending, which is following “K-shaped” patterns. A significant correction to the valuations of tech leaders would therefore be even more likely to result in recession.

Vocabulary is a power builder. Every time I use the word “hegemonic” in a conversation, I see my listeners’ eyebrows go up as if to say, “what does this guy know that I don’t?” Then again maybe they’re just signaling that I’m full of more than baked beans.

The 10-year Treasury yield has experienced dramatic fluctuations, ranging from a peak of 15.68% in October 1981, during the height of the Volcker era, to a historic low of 0.55% in August 2020, amidst the economic uncertainty of the pandemic. At the end of May 2026, the weekly average stood at 4.47%.

New York City is facing one of the most significant fiscal challenges in recent memory. The NYC Comptroller has projected a $2.2 billion budget shortfall for FY2026, growing to a $10.4 billion gap in FY2027 (Source: New York City Comptroller, January 2026). That is a two-year deficit of roughly $12.6 billion.

Before I recommend what to do, I want to first state what not to do. Don’t invest as if you think you know what long-term inflation will be. Will we return to the double-digit inflation of the late ‘70s and early ‘80s? The answer is: Nobody knows.

The industry is entering a more customized phase of liability-driven investing, he said. While earlier stages focused on adding duration and raising fixed-income allocations, better-funded plans are now tinkering at the margins to more precisely match their holdings with their obligations.