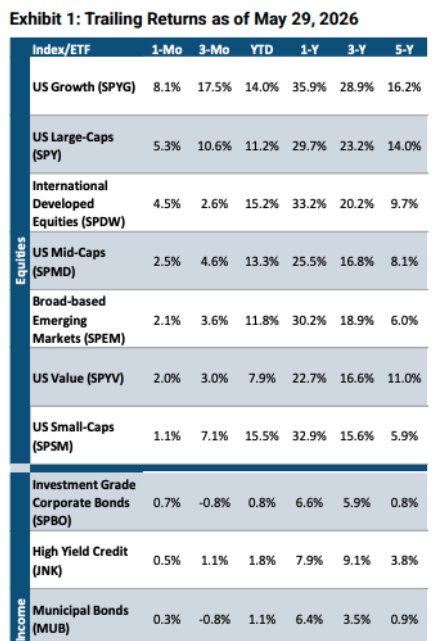

All Three Major Indices Close May at Record Highs

Despite rising global yields and renewed inflation concerns, equities moved higher in May on the back of a strong US earnings season and continued momentum in AI-related stocks. The tech-heavy Nasdaq Composite gained 8.4% for the month, while the S&P 500 rose 5.3% and the Dow Jones Industrial Average was up 2.9% All three indices closed the month at record highs. The S&P 500 also saw its best two-month gain since May 2020, climbing over 16% since the end of March. International developed equities and US mid-caps also rose for the month (+4.5% and +2.5%, respectively). Bonds mostly fared well as investment grade corporates were up 0.7%, high yield credits gained 0.5%, and municipal bonds rose 0.3%. Aside from silver (+2.5%), commodities struggled as crude oil fell 12.2%, broad-based commodities declined 3.4%, and gold decreased 1.5%.

New Fed Chair Inherits Challenging Backdrop

Kevin Warsh was officially sworn in as Federal Reserve Chair at the White House on May 22, pledging to “lead a reform-oriented Federal Reserve” and to preserve the central bank’s independence over monetary policy. The economic backdrop he inherits remains challenging. The May reading of the Consumer Price Index (CPI) came in at 3.8%, its highest level since May 2023, while the Producer Price Index (PPI) inflation reached a 6.0% annual rate, the highest since late 2022. Higher energy prices driven by conflict in the Middle East were a primary contributor to inflationary pressures. Bond markets repriced in response, with the 30-year Treasury yield reaching approximately 5.2% in mid-May, its highest level since 2007, while the 10-year yield climbed above 4.6%. Conditions eased late in the month amid reports of progress toward a peace agreement and the potential reopening of the Strait of Hormuz. Fed Governor Lisa Cook noted that “the risks remain tilted toward higher inflation” and indicated she would be prepared to raise rates if price pressures persist. Despite the administration’s open desire for lower rates, markets expect the Fed to hold through year-end while pricing in roughly a 41% probability of a December hike

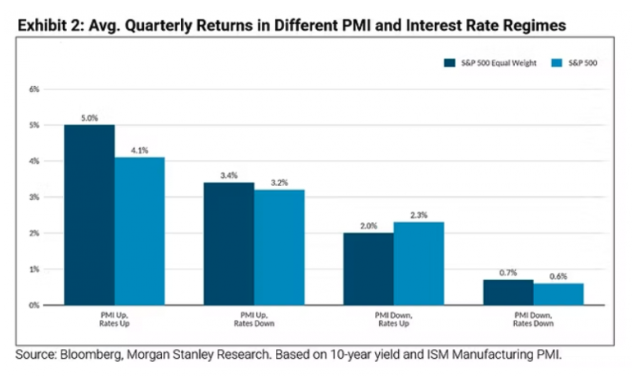

Can Equities Tolerate Higher Yields?

Many investors expect rates to remain structurally higher for longer given the persistence of geopolitical supply disruptions and broadening price pressures. Although the recent move in rates has been driven largely by an inflation repricing, which is typically a less favorable backdrop for equities, the underlying growth picture remains encouraging. Morgan Stanley Research notes that average quarterly returns have historically been strongest when PMIs are rising alongside rates, with the S&P 500 Equal Weight returning approximately 5.0% and the cap-weighted S&P 500 returning roughly 4.1% in such regimes. In other words, equities have historically been able to tolerate sticky yields when accompanied by healthy growth. Nearly two-thirds of S&P 500 companies are growing their top line by at least 5%, the highest share since 2023. This broadening earnings strength is visible across the wider market as well, with the median Russell 3000 stock posting EPS growth of 10% in Q1 2026, the highest since Q3 2021. If growth continues to hold up at these levels, it may provide a fundamental cushion that allows equities to absorb higher rates.

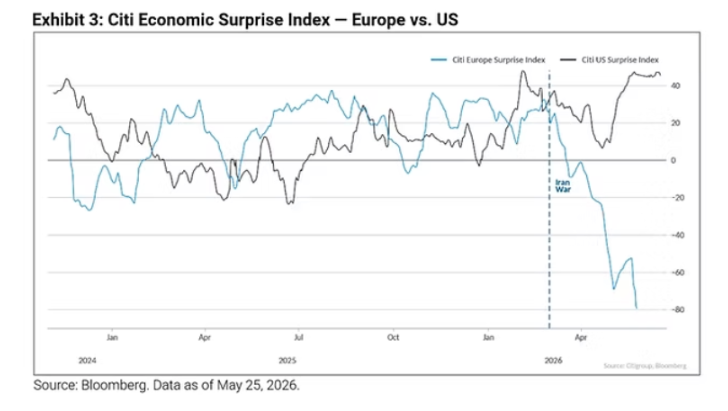

Economic Surprises Diverge Between Europe and the US

Economic data in Europe and the US have moved in opposite directions in recent months. The Citi Economic Surprise Index, which tracks whether macroeconomic releases are coming in above or below consensus forecasts, illustrates this divergence. The Europe index has fallen to around -80, suggesting data has consistently missed expectations, while the US index has risen to roughly +40, as releases have generally exceeded forecasts. The widening gap coincided with the onset of the Iran conflict, with Europe’s relatively greater exposure to Middle Eastern energy supply disruptions likely contributing to the softness in its economic data. This gap reinforces the relative resilience of the US economy and helps explain the outperformance of US equities versus their European counterparts since the war-driven lows.

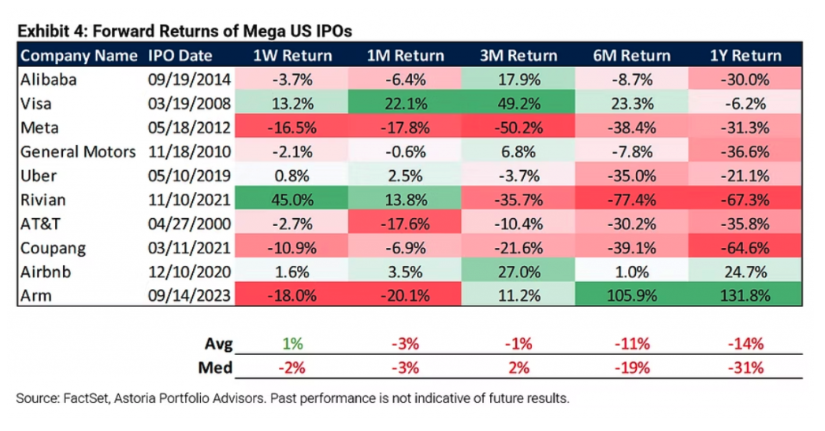

The History of US Mega-IPOs. Will SpaceX Be Different?

Across various US Mega-IPOs, the vast majority posted negative one-year forward returns from their IPO date, with a median decline of 31%. Even those with strong early performance, such as Rivian (+45% at one week) and Visa (+49% at three months), ultimately gave back their gains over the subsequent year. Among the list below, only Airbnb (+25%) and Arm (+132%) bucked the trend over their first twelve months. With SpaceX set to debut on the Nasdaq in June at a valuation of approximately $1.8 trillion, this pattern warrants attention. However, several structural factors could differentiate this cycle. Major indices have adopted or are considering new fast-entry rules that would allow SpaceX to be included shortly after listing, potentially pulling forward significant passive buying from ETFs and index funds. Beyond index mechanics, SpaceX sits at the intersection of several secular growth themes, including satellite connectivity, commercial space infrastructure, and AI. Whether these structural tailwinds from passive flows and thematic positioning are enough to overcome the historically poor track record of mega-IPOs remains a consequential question for the second half of 2026.

Click here to view this report as a PDF.

For more news, information, and strategy, visit the ETF Strategist Content Hub.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in SPYG, SPY, SPYV, SPDW, SPMD, SPSM, SPEM, SPBO, SPAB, MUB, IEF, SPIP, GLD, SLV, USO, BCI, META, MSFT, GOOGL, BABA, V, META, GM, UBER, RIVN, T, ABNB, ARM, and AMZN on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by Astoria Portfolio Advisors