Rupture and Resilience

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIntroduction and key themes

For more than four decades, PIMCO’s Secular Forum has provided a disciplined framework for stepping back from short-term market noise to assess the structural forces that will shape the global economy and markets over the next five years. Yet rarely has this exercise been more consequential than it has recently.

The world today is undergoing a rupture. The geopolitical risk we highlighted in our 2025 Secular Outlook, “The Fragmentation Era,” has become kinetic reality in 2026. Fragmentation is becoming evident around the world in energy prices, supply chain data, growth rates, and investment returns. The cost of complacency has surged. Investors can no longer rely on outdated assumptions about globalization, policy backstops, and suppressed volatility.

Yet investment opportunities in this world remain abundant. That’s because the generational reset in bond yields a few years ago – the theme of our 2024 Secular Outlook, “Yield Advantage” – enables us to pursue resilient, globally diversified portfolios anchored by high quality fixed income in both public and private markets.

Key macroeconomic takeaways

-

Rupture, not transition.

The fragmentation of trade, security, and financial alliances we identified last year is accelerating. The global economic trajectory has shifted from a narrow range of plausible outcomes to an uncertain and wide distribution of possible scenarios. That said, we expect the U.S. dollar will remain the world’s dominant currency for the foreseeable future. -

Resilience to be tested.

Politics, geopolitics, and economic security policy now shape growth and inflation directly, increasing dispersion across countries, sectors, and firms rather than just raising market and macro volatility. These forces will likely test economic resilience, especially since fiscal space is limited. Under our baseline, we do not expect a sudden stop U.S. fiscal crisis or loss of market access for other major sovereign issuers. The more likely path is episodic volatility as markets periodically refocus on debt sustainability and fiscal credibility. -

Fat tails – in both directions.

The AI investment boom, rising defense spending, and energy security investments could add up to $14 trillion to global capital spending over the next five years. AI’s potential to compress wages and raise productivity could become a powerful disinflationary force, but geopolitical shocks and supply chain reconfiguration will likely put upward pressure on prices. In other words, we see a range of outcomes (i.e., “fat tails”) on either side of the baseline. It is our firm conviction that central banks will do what it takes to keep inflation expectations anchored over the next five years.

Read more: Energy Credit Market Returns Reflect Sector Discipline

Key investment takeaways

-

The credit loss cycle is upon us.

After years of effortless returns, the default cycle is reasserting itself, and we expect significantly higher losses in lower-quality credit such as leveraged and private direct lending. We view this as the beginning of a secular trend where quality and credit selection will matter more than ever. At this stage of the cycle, we are seeing an acceleration in credit-ratings-based and liquidity-based financial engineering, particularly in private markets, although we do not see systemic risk on the scale of 2005–2006. In this environment, asset-based finance and publicly traded credit markets look relatively attractive, and we believe credit stress will lead to considerable opportunities to provide capital solutions to borrowers. -

The yield advantage has only grown more compelling.

Investors can seek to construct globally diversified, high quality fixed income portfolios with yields of 5%–7% in local-currency terms – competitive with long-run equity returns at lower potential volatility. High starting yields can help income to do more of the work across a variety of possible scenarios, reducing reliance on capital gains or accurate macro forecasts. -

Bonds can still provide portfolio diversification, particularly in economic downturns.

Central banks have much more room to cut rates in future economic downturns than in the decade before the pandemic, and we expect them to use it. An actively managed bond portfolio can offer investors diversification and potential for capital appreciation in future recessions.

Secular theme: rupture and resilience

The global economy is no longer gliding along a familiar path of ongoing globalization and increasing integration. In the words of Canadian Prime Minister Mark Carney, the world is undergoing a rupture rather than a mere transition away from the post–World War II rules-based regime.

Last year, in “The Fragmentation Era,” we argued that the traditional relationship between politics and economics had inverted, with politics and protectionism increasingly driving economic outcomes. We warned that fragmentation would become an independent source of volatility, shaping business cycles and creating distinct winners and losers across companies, sectors, and countries. Since then, the world has witnessed significant changes:

- Escalating trade and economic security confrontations

- Resilient global growth – at least so far – in the face of these shocks

- A massive AI investment boom

- Emerging stresses and strains in lower-quality private credit and opaque financial structures

As we write this, the global economy is navigating a conflict in the Middle East that has triggered one of the biggest oil supply shocks in history. The implications are inflationary in the short term while the shock also signals the potential for demand destruction and a growth slowdown over time.

Resilience to be tested

We believe several powerful forces related to geopolitics, fragmentation, and AI will drive the global economy and markets over the next five years.

Geopolitical risk has become reality. Events in the Middle East underscored the vulnerability of global energy and trade networks to disruption at a handful of critical chokepoints. Risk premia that had been embedded in implied volatility are now being tested through realized outcomes. These dynamics complicate forecasting and increase the likelihood of episodic market stress, even if worst-case scenarios are avoided.

The pace of fragmentation is accelerating. Governments are playing a more direct role in shaping economic outcomes, extending state intervention well beyond traditional industrial policy toward the broader goals of economic security. Trade restrictions, export controls, subsidies, investment screening, and public procurement are now core tools of economic strategy. The U.S., China, Europe, and an increasingly assertive group of middle powers are pursuing distinct models of economic security. Supply chains are being reshaped not only for efficiency, but also for resilience and security.

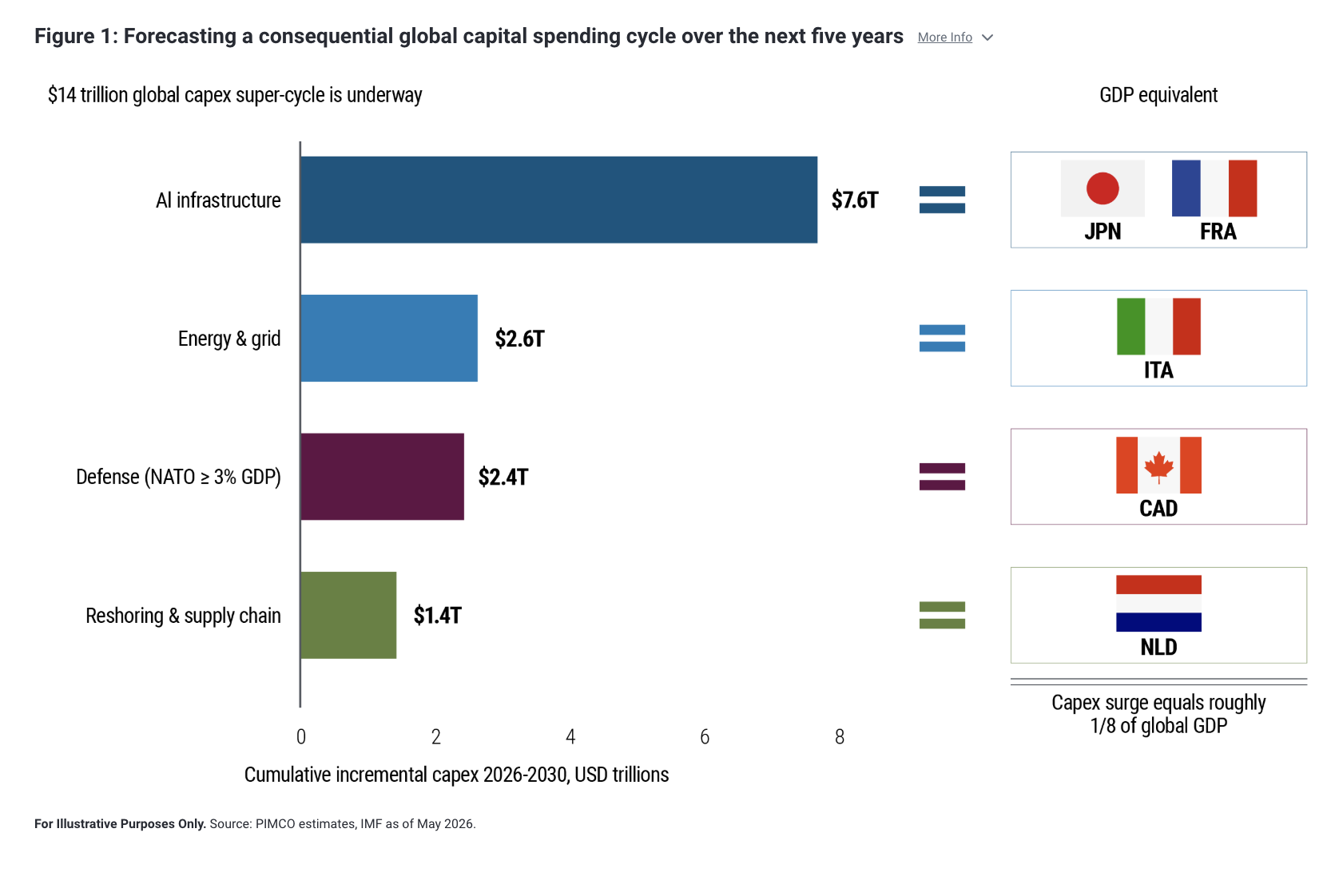

Artificial intelligence has crossed a threshold. AI investment is now large enough to drive macroeconomic activity. The buildout of AI infrastructure, combined with rising defense spending and energy security investments, could add roughly $14 trillion to global capital spending over the next five years (see Figure 1).

Capex on data centers, processing capacity, and power infrastructure is reshaping corporate balance sheets and sectoral dynamics. The productivity payoff could arrive faster, and prove more disinflationary, than many investors now expect. At the same time, AI is amplifying dispersion across companies, across industries, and across capital structures.

These forces are not independent. Fragmentation accelerates AI investment through support of national champions and the provision of sovereign infrastructure. AI, in turn, reinforces fragmentation by making computing capacity and energy strategic assets. Geopolitical risk overlays both, creating a secular environment in which baseline scenarios must be balanced against increasingly fat tails.

Geopolitics, domestic politics, and industrial policy are no longer external forces that occasionally disrupt the economy. They have become central drivers of growth, inflation, market returns, and volatility. For investors, the implication may be not just higher volatility, but also greater dispersion in returns across asset classes.

Energy and uncertainty

Uncertainty around the endgame for security alliances has increased downside risks to growth. Trade, payments systems, and energy flows have become tools of statecraft. As a result, shocks may propagate more quickly and with greater market impact than in the past.

Energy sits at the center of this uncertainty. Energy security is now inseparable from economic security, defense readiness, and the deployment of energy-intensive technologies such as artificial intelligence. Outcomes range widely: from higher-for-longer prices that pressure growth and inflation, to periods of sharp disinflation if supply responses accelerate or demand weakens abruptly. Regardless of the path, geopolitical risk premia in energy markets are likely to remain elevated over the secular horizon.

Relative to our baseline, risks to global growth are skewed to the downside. Broader or more prolonged conflicts – particularly those affecting major energy chokepoints – would raise the probability of policy mistakes and nonlinear market reactions. In this environment, uncertainty itself becomes a macro variable, shaping investment behavior and reinforcing the case for resilience.

China: transition under constraint

China continues an inevitable transition toward a lower long-term growth model, paired with an aggressive push to dominate strategic industries while maintaining an annual growth target. While trade tensions with the U.S. remain acute, China’s export capacity continues to exert disinflationary pressure on global goods prices. At the same time, rising debt levels and limited fiscal space constrain policymakers’ ability to rely on demand-side stimulus.

China remains a pivotal player in global fragmentation, is an ongoing source of global disinflation, and holds significant strategic and geoeconomic leverage that it brings into international trade and security discussions.

Emerging markets: an unusual inflection point

The same forces driving rupture in the developed world – U.S. dollar rebalancing, supply chain rewiring, energy security investment, and AI infrastructure buildout – are creating a differentiated opportunity set across emerging market (EM) sovereign and corporate bond issuers. Countries with credible central banks, commodity export capacity, and the scale to capture larger shares of the global supply value chain are seeing fundamentals converge toward, and in some cases surpass, those of lower-rated developed market (DM) peers.

AI has arrived

AI is no longer a wild card but has become a core component of our secular outlook. Investment is already reshaping demand, while the productivity uplift may arrive sooner than many expect. Over time, AI is likely to be disinflationary across many sectors, particularly if it compresses labor costs and improves efficiency.

For investors, the key implication is not simply to identify beneficiaries, but to recognize that dispersion is widening and that poorly positioned, highly leveraged businesses are increasingly exposed.

Policy space: monetary and fiscal

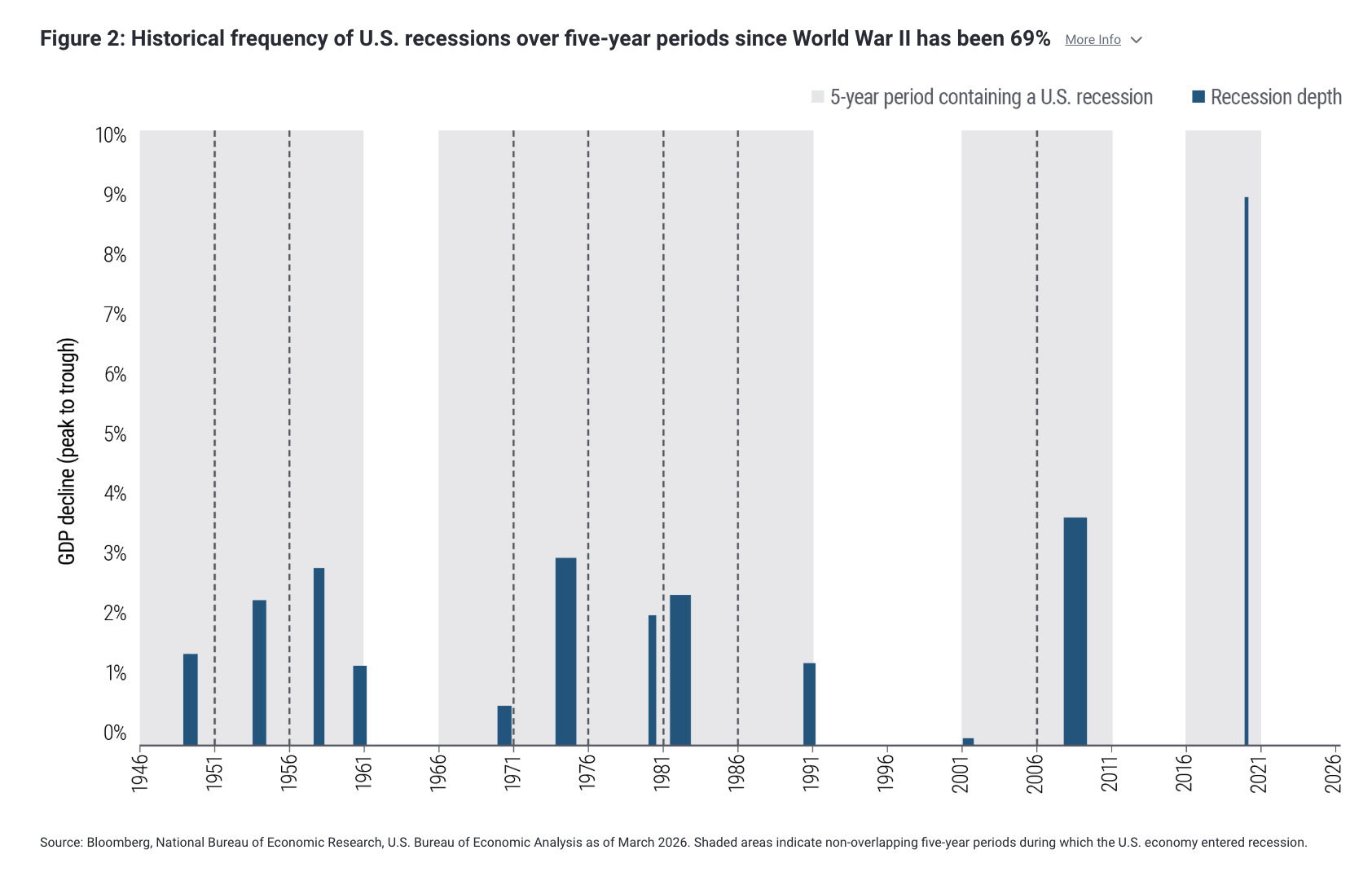

We expect central banks to do what it takes to keep inflation expectations anchored. That said, central banks today have much more conventional policy space than in the decade before the pandemic, and we expect them to use it and cut rates in a future recession. For this reason, sovereign bonds offer income plus the potential for capital gains in a future downturn – a noteworthy point given the historical frequency of recessions (see Figure 2).

By contrast, fiscal space is limited across almost all advanced economies. In the U.S., elevated debt and persistent deficits also limit fiscal space, but do not, in our baseline view, imply that a U.S. fiscal crisis is imminent. Moreover, the dollar should remain the dominant global currency, though its valuation may gradually adjust as global portfolios rebalance and demand for hard assets rises.

The dollar’s reserve status affords the U.S. more flexibility than other sovereign issuers. While debt remains sustainable in the short to medium term in most DM economies, the U.S. remains on an unsustainable trajectory under current policy, which continues to kick the can down the road. High deficits will need to be addressed eventually. In the meantime, a weaker fiscal backdrop tends to lead to higher real interest rates, which should benefit investors.

Investment implications: resilience, not reach

In 2024, we titled our Secular Outlook “Yield Advantage” to highlight a generational reset in bond yields. Two years on, we believe that thesis has only strengthened. In a world characterized by rupture – geopolitical, economic, and institutional – the case for building resilient portfolios without reaching for risk is stronger today than it has been in years.

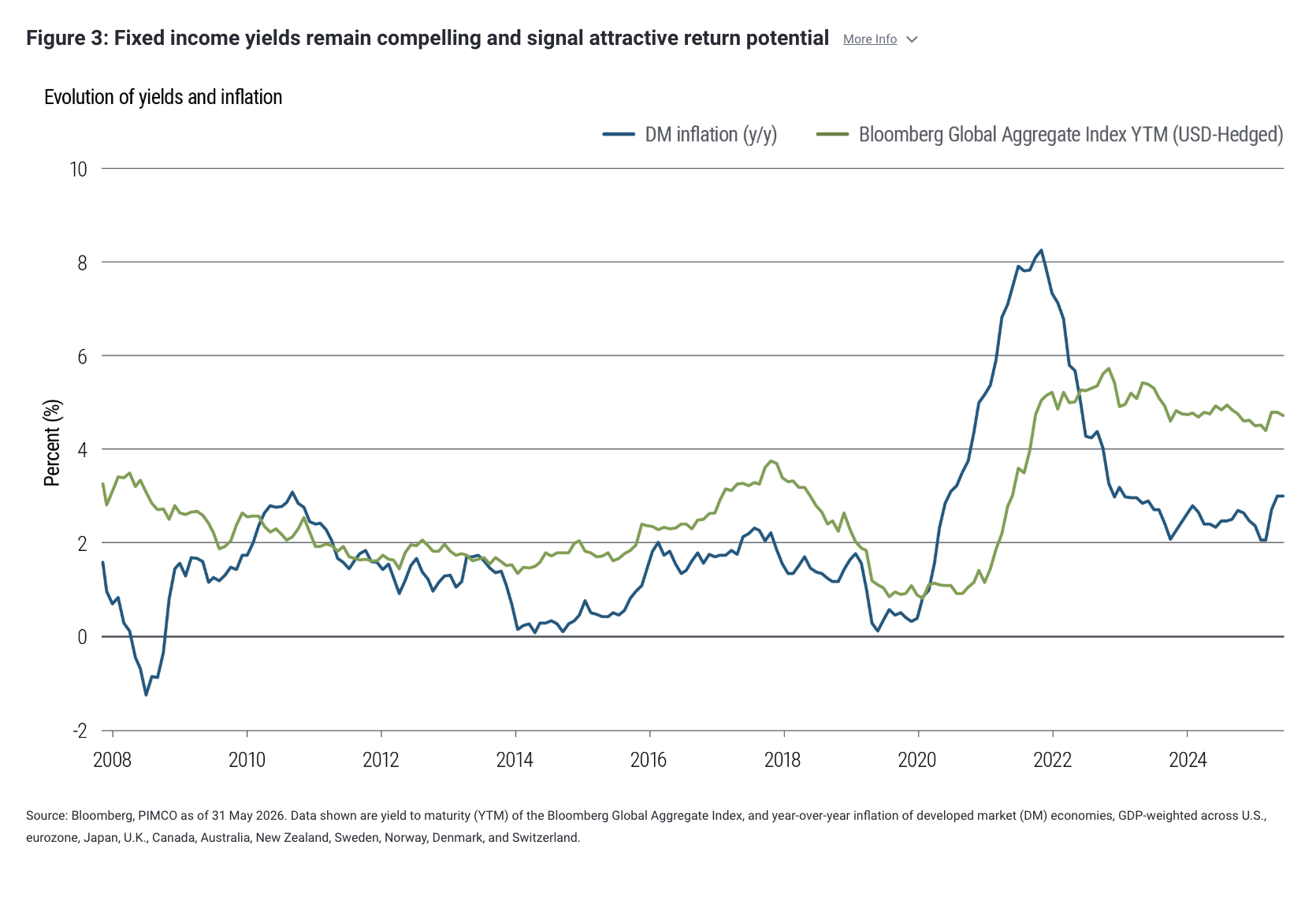

The low-yield era following the global financial crisis was a historical anomaly. The reset in global yields over the past several years (see Figure 3) has restored fixed income’s role as both a return generator and a shock absorber, at a time when equity valuations and private market leverage leave less margin for error.

This greater yield “cushion” can provide bonds a secular advantage, with the opportunity for strong performance across a wide variety of potential scenarios:

- Deflationary pressures arising from AI-related efficiency gains

- A potential disappointment in AI-related efficiency gains that slows equity-led economic gains

- Growth shocks that lead to central bank rate cuts

In the past, bond investors often had to choose between desirable characteristics such as attractive yield, high credit quality, and diversification benefits. Today, investors may be able to realize these attributes together.

The defining investment implication of our secular outlook is not that risk should be avoided, but that investors should be paid for risk – and that investors no longer need to stretch to achieve reasonable long-term returns. High quality fixed income may once again offer income levels competitive with long-run equity returns, with materially lower volatility and strong potential across a variety of scenarios, particularly in a downturn. In an environment of fatter tails, that matters.

Fixed income’s value proposition, in absolute and relative terms

Over multiyear horizons, fixed income returns have historically been largely anchored by starting yields. Today, those starting yields look compelling. The yields on the Bloomberg U.S. Aggregate and Global Aggregate (hedged to U.S. dollar) indices, two common benchmarks for high quality bonds, are about 4.71% and 4.75%, respectively, as of 4 June 2026.

Using that as a baseline, managers with global mandates can construct diversified portfolios yielding 5%–7% in local-currency terms without necessarily compromising quality or liquidity. Bond yields continue to appear more attractive relative to cash for a modest increase in risk.

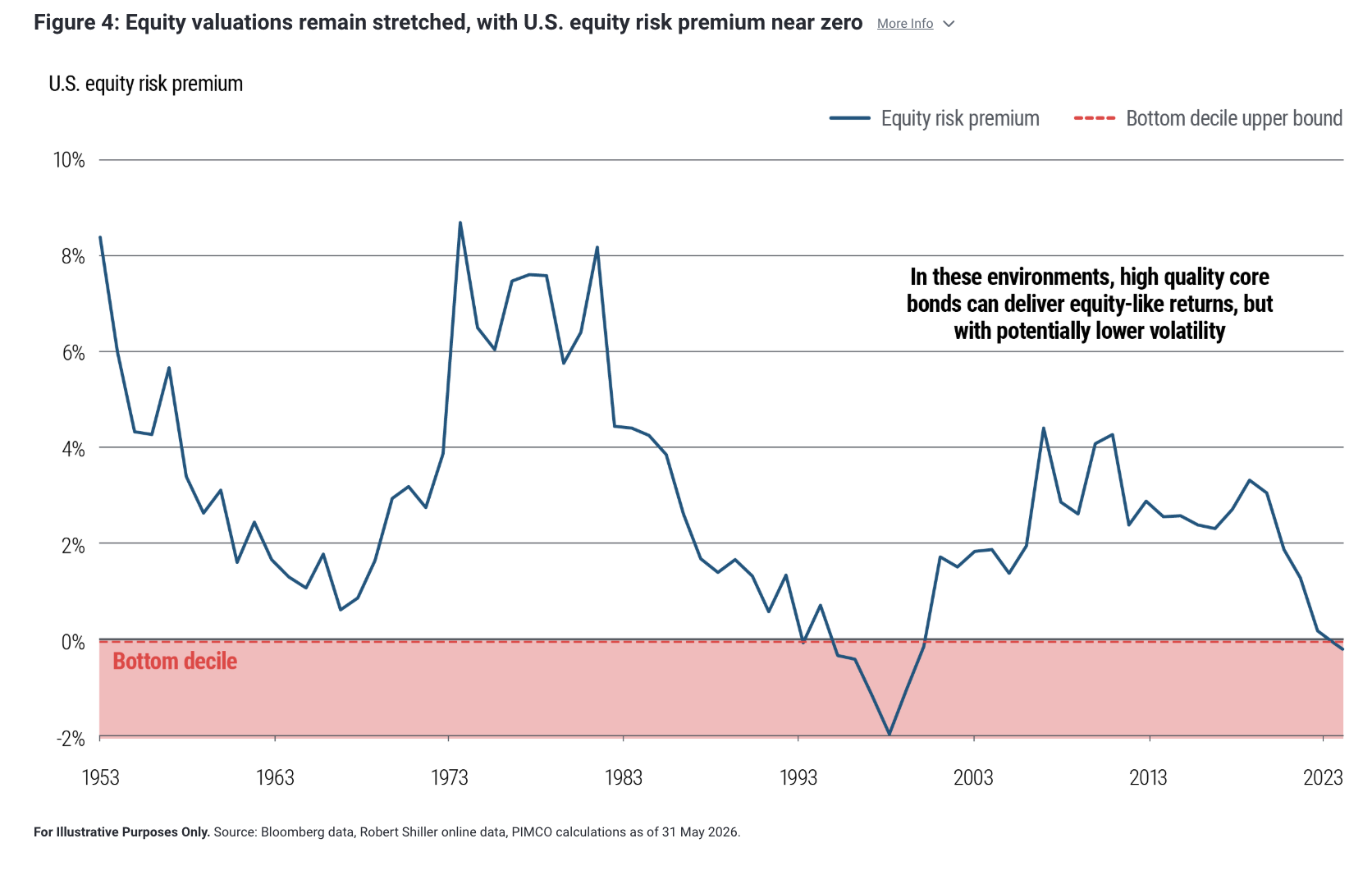

The comparison with equities is increasingly stark. Equity valuations remain elevated relative to history, and the equity risk premium – particularly in the U.S. – sits near the low end of its post–World War II range (see Figure 4).

We are not calling for an imminent equity correction. But we do believe that the prospective Sharpe ratio – a gauge of risk-adjusted return – of high quality fixed income now compares favorably with equities for the first time in many years. This argues for reconsidering portfolio allocations that were shaped during the low-yield, low-volatility decade following the global financial crisis.

We continue to believe that the traditional 60/40 stocks/bonds framework again warrants attention after equity exposures for many investors have drifted higher. Fixed income can once again do more of the work it was always meant to do: generate income, dampen volatility, and provide ballast during risk-off episodes.

High quality fixed income: where the opportunity sits

Within high quality fixed income, our highest-conviction opportunities remain concentrated in a few areas.

First, intermediate-duration bonds continue to offer an attractive balance of yield, roll-down, and risk. The five- to 10-year segment of global yield curves looks well compensated relative to both shorter-dated cash and the long end, where fiscal dynamics and term premium uncertainty argue for caution.

Second, agency mortgage-backed securities stand out. These securities trade in a deep and liquid market. Spreads remain wide relative to history, credit quality is high, and supply/demand dynamics are improving as bank balance sheets stabilize and the Federal Reserve’s footprint recedes. In our view, this combination can offer an attractive source of income and diversification.

Third, global government bonds merit renewed attention. Business cycles are increasingly desynchronized, and monetary policy paths are diverging across countries. A global fixed income allocation can seek the potential benefits of global diversification and strengthened risk-adjusted returns over time. It can create opportunities for active country selection – including EM countries with credible policies and strong fundamentals – and curve positioning that were largely absent during the era of synchronized global easing. At today’s starting yields, global bond exposure should help provide diversification alongside the potential for higher income. With the U.S. on an unsustainable long-term debt path, owning non-U.S. debt can be a prudent way to diversify.

Finally, inflation-linked bonds and select real assets often play an important role in resilient portfolios. With inflation tails fatter and geopolitical risks to energy elevated, real (inflation-adjusted) yields that are positive by historical standards can help provide a meaningful buffer to volatility. Gold, in particular, has continued to serve as a neutral store of value in a world of partial confidence in fiat currencies.

Credit: the dispersion is the opportunity

Credit markets, in aggregate, continue to price a benign outcome. Credit spreads across investment grade, high yield, and private credit remain near the tight end of historical distributions despite elevated secular uncertainty. We interpret this as complacency rather than strength.

Years of abundant capital and “buy the dip” behavior have encouraged aggressive underwriting, high leverage, and widespread use of floating-rate structures. Now, the credit loss cycle is upon us. We are particularly cautious in lower-quality, economically sensitive corporate credit. Even in a strong economy, AI will disrupt old economy companies, especially highly levered ones.

As growth slows and refinancing costs remain elevated, stresses are emerging – most visibly in segments of private corporate credit and middle market direct lending. We are witnessing increased instances of maturity extensions and payment-in-kind structures that allow borrowers to repay debt with more debt. In our view, a more genuine default cycle is now unfolding, and investors should not expect past patterns of rapid recovery to repeat with the same reliability.

By contrast, we continue to see more attractive risk-adjusted opportunities in asset-based finance. Areas such as equipment finance, consumer lending, residential mortgages, real estate credit, and select infrastructure finance benefit from strong collateral, granular diversification, and cash flows that are less directly tied to corporate earnings. At current valuations, these characteristics can offer what we see as a superior balance of income and source of downside protection.

Watch the financial engineers

As capital becomes scarcer and balance sheets seek growth, we expect financial engineering to accelerate. This is most evident in private credit, private-equity-adjacent structures, and insurance balance sheets, where incentives to source higher-yielding assets are powerful. We also see it playing out in more specialized ETFs, such as passive and leveraged exposures to less-established areas of the market. We do not view this as systemic, nor do we see parallels to the buildup of risk that preceded the global financial crisis. But it bears scrutiny.

Credit selection matters and investors should get paid to provide liquidity. An investment grade label does not always imply investment grade risk, particularly when ratings rely heavily on structure rather than underlying asset resilience. Highly engineered financings related to AI or reinsurance vehicles warrant especially careful analysis.

At the same time, the AI buildout is also driving significant infrastructure financing needs, particularly in bonds and loans, creating opportunity for lenders with discipline and scale. Focusing on deals with claims on hard assets and strong documentation can help investors seek steady returns while mitigating risk (for more, see our 29 May commentary, “Investment Discipline Amid the AI Infrastructure Boom”).

Opportunities across EM

The starting yields available today across EM local and hard currency markets are among the most compelling in over a decade. There is also potential for secular U.S. dollar weakness, historically among the most powerful tailwinds for EM local currency returns.

Emerging markets have become an underappreciated tool for risk management. The intuition is straightforward: EM can often offer yields meaningfully above those of comparable-duration DM instruments. The deeper insight in today’s macro backdrop is that EM now also provides important portfolio diversification against the very disruptions emanating from the developed world itself. In a regime where U.S. fiscal dynamics, dollar rebalancing, and DM policy uncertainty are the primary sources of portfolio risk, EM exposure can offer a genuine hedge rather than simply an additional source of yield.

In hard currency, select sovereign and quasi-sovereign credit – particularly among commodity-exporting frontier and investment grade issuers – can offer spread compensation that often more than accounts for idiosyncratic risk. Beyond public markets, EM private credit and structured finance, including infrastructure finance, asset-based lending, and development finance institution (DFI)-partnered structures, represent an expanding opportunity set that can combine those potential yield benefits of EM with the collateral discipline of asset-based finance.

Putting it together

In a post-rupture world, the most consequential investment mistake is reaching for risk when that risk is poorly compensated. We believe the current yield environment offers a compelling alternative.

We believe resilient portfolios today are built around liquid, high quality fixed income, an up-in-quality bias in credit, broad global diversification, and selective exposure to real assets and asset-based finance. Over the next five years, discipline is likely to matter more than daring – and resilience more than reach.

Disclosure

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or private guarantee, there is no assurance that private guarantors will meet their obligations. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing a strategy.

Investments in asset-based lending and asset-backed instruments are subject to a variety of risks that may adversely affect the performance and value of the investment. These risks include, but are not limited to, credit risk, liquidity risk, interest rate risk, operational risk, structural risk, sponsor risk, monoline wrapper risk, and other legal risks. Asset-backed securities across various asset classes may not achieve business objectives or generate returns, and their performance can be significantly impacted by fluctuations in interest rates. Investments in residential and commercial mortgage loans, as well as commercial real estate debt, are subject to risks that include prepayment, delinquency, foreclosure, risks of loss, servicing risks, and adverse regulatory developments. These risks may be heightened in the case of non-performing loans. Structured products, such as collateralized debt obligations, are also highly complex instruments that typically involve a high degree of risk; the use of these instruments may involve derivative instruments that could result in losses exceeding the principal amount invested. Private credit involves investments in non-publicly traded securities, which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Additionally, investments in private credit may be subject to real estate-related risks, which include new regulatory or legislative developments, the attractiveness and location of properties, the financial condition of tenants, potential liability under environmental and other laws, as well as natural disasters and other factors beyond a manager’s control. Investing in banks and related entities is a highly complex field subject to extensive regulation, and investments in such entities may give rise to control person liability and other risks. Investing in distressed loans and bankrupt companies is speculative, and the repayment of default obligations contains significant uncertainties. High-yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Collateralized Loan Obligations (CLOs) may involve a high degree of risk and are intended for sale to qualified investors only. Investors may lose some or all of their investment, and there may be periods during which no cash flow distributions are received. These investments are exposed to risks such as credit, default, liquidity, management, volatility, interest rate, and credit risk.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0604-5550145

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All