The era of easy returns came to a screeching halt in 2022.

U.S. stocks are rising in pre-market trading, looking to rebound from yesterday's drop.

Bear markets end with widespread capitulation while a chorus of the stock trader’s prayer (God, if you get me out of this mess, I swear I will never buy another stock) spreads through out the land.

U.S. stocks continue to oscillate around the unchanged mark.

Ever so subtly, the high interest rates of the past year have started to separate the viable businesses from the ones sustained by cheap money.

U.S. stocks are rising in pre-market action in the first trading session of the week following the long holiday weekend.

The market dislocations and skyrocketing inflation of the last year put longstanding retirement maxims to the test and that test isn’t over yet.

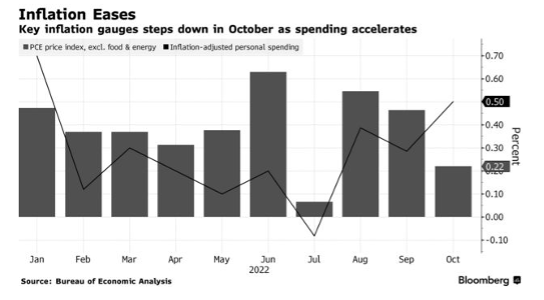

The Federal Reserve’s preferred inflation measures eased in November while consumer spending stagnated, suggesting the central bank’s interest-rate hikes are helping to cool both price pressures and broader demand — with more tightening on the way.

In a year when soaring inflation and sinking growth rocked corporate boardrooms and Wall Street trading floors, some nooks of the stock market gave investors shelter to hide out.

Great articles don’t always get the readership they deserve. We’ve posted the 10 most-widely read investment, planning and practice management articles over the last two days. Below are another 10 that you might have missed, but I believe merit reading.

Private credit can be an attractive asset that has provided high yield and protection against the risks of rising inflation. In addition, the asset class has a strong credit history – specifically senior, secured, sponsored debt.

The big question heading into 2023 is the dreaded “R” word.

U.S. equities are modestly higher but near the unchanged mark in pre-market action.

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

I’m not sure where I’m going these days.

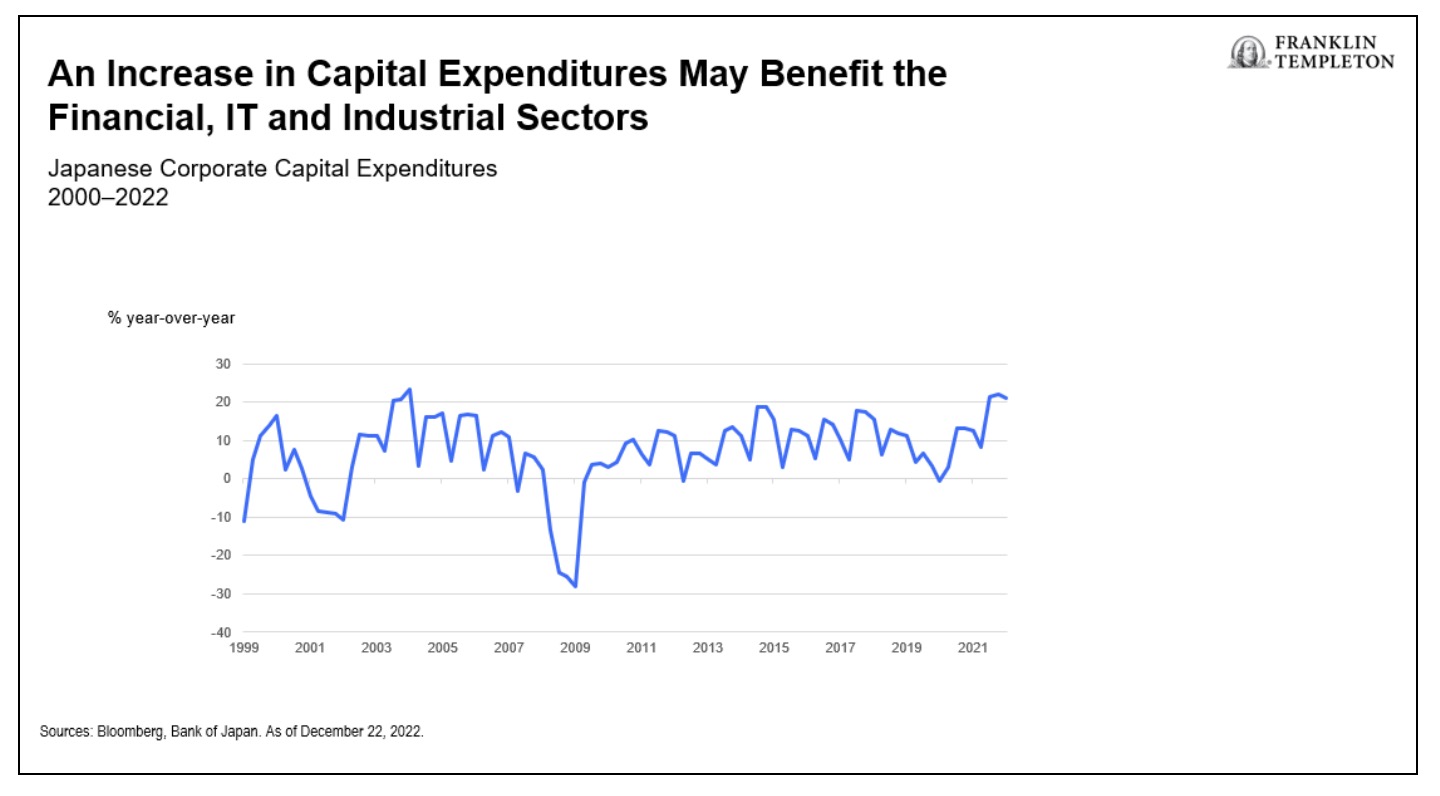

Templeton Global Equity Group weighs in on inflation’s emergence in Japan, recent monetary policy shifts, and the implications for investors.

The bond market humbled Wall Street’s best and brightest in 2022.

Putting 60% of a portfolio in stocks and 40% in bonds is supposed to hedge against both assets dropping simultaneously. But it didn’t pan out that way in 2022.

U.S. stocks are falling sharply, giving up yesterday's rally.

Rick Rieder and team outline how to think about portfolios as we enter 2023.

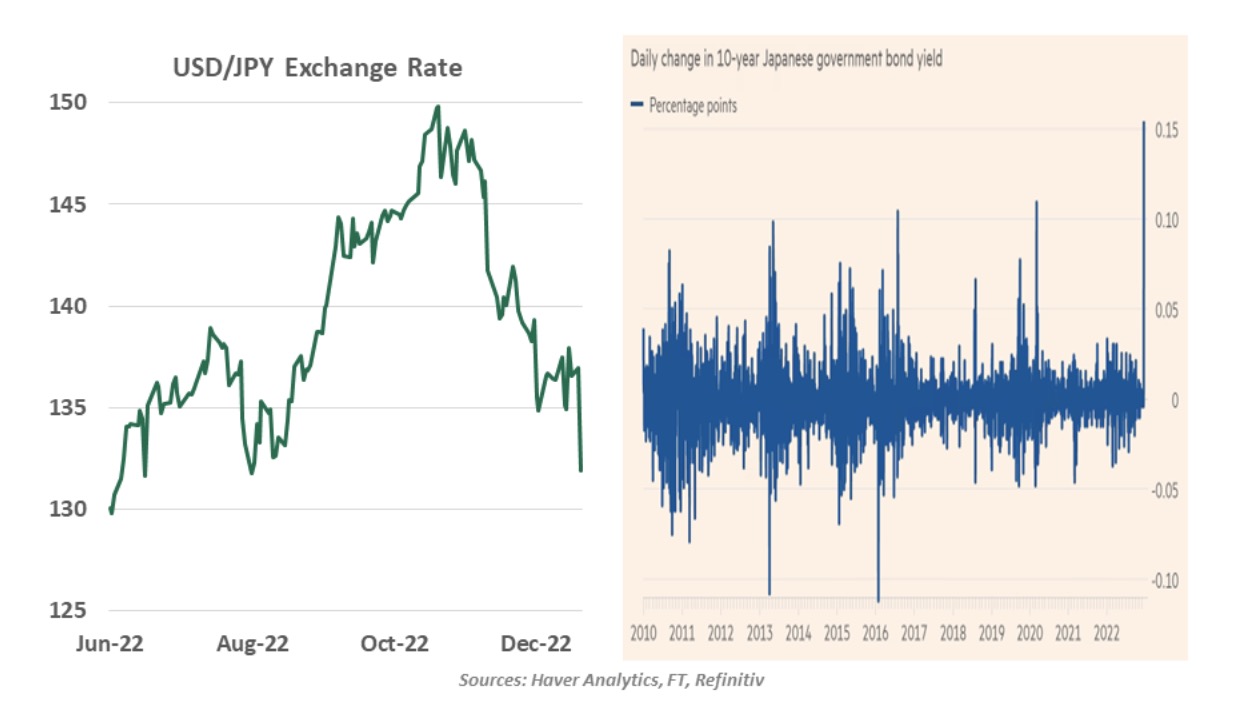

A surprising shift in Japan's monetary policy.

The year isn't yet done with rattling investors' cages. The Bank of Japan’s surprise widening of its yield curve-control policy on 10-year government bonds will have an impact far beyond its shores.

Wall Street’s stock market soothsayers weren’t entirely wrong about 2022. In fact, S&P 500 Index earnings are on pace to match the consensus forecasts that analysts submitted about a year ago. Stock prices, however, are another story.

In a recent San Francisco Federal Reserve Publication titled “Monetary Policy Stance is Tighter Than Fed Funds Rate,” the authors argue that the “all in” policy rate is actually higher than the Fed Funds rate would suggest.

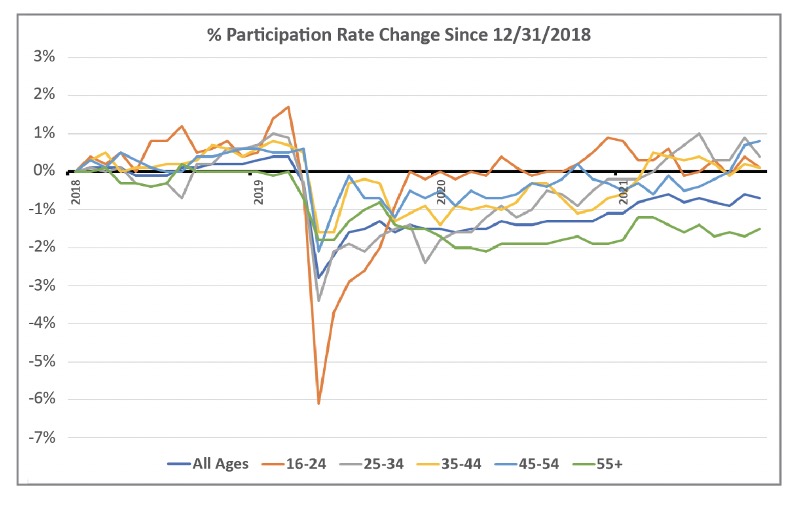

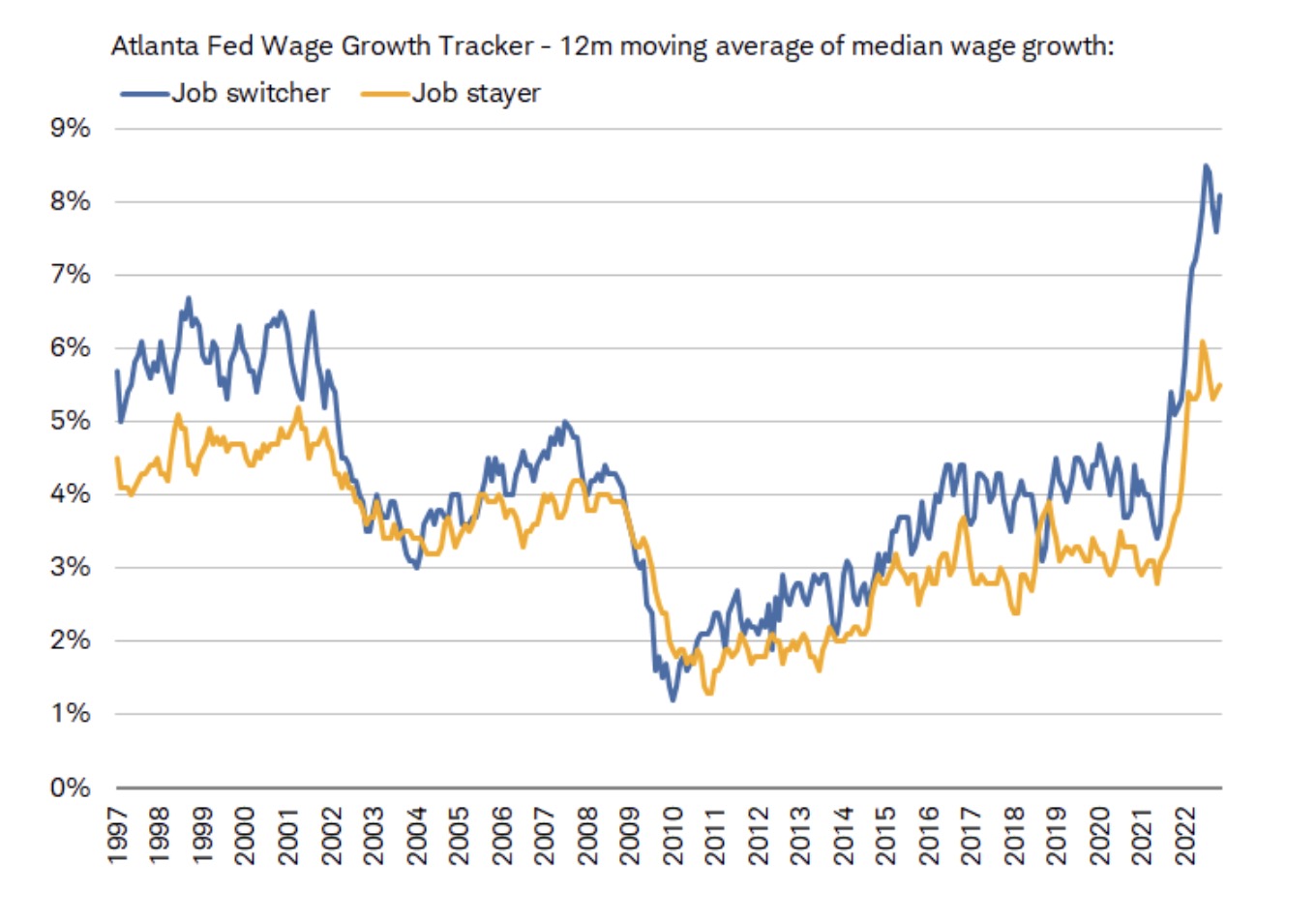

Structurally tight labor markets are providing support for tighter monetary policy, but the Fed may be fighting an uphill battle.

Monetary policy is more like the World Cup than it is like mathematics or great literature.

Investors are spurning mutual funds at a record clip, driving a $1.5 trillion gap in the flow of money from the old-school investment vehicles and into ever-popular ETFs.

“I have never seen so much bearishness in the market,” Jeremy Siegel said, “which is a great sign for stock investors.”

The economic tea leaves suggest that 2023 could be another challenging year for both stocks and bonds. However, the outlook is more balanced given that equity valuations are much lower and bond yields much higher.

Inflation trends are moving in a favorable direction, but the change is likely too slow for the Fed to take its foot off the brake anytime soon.

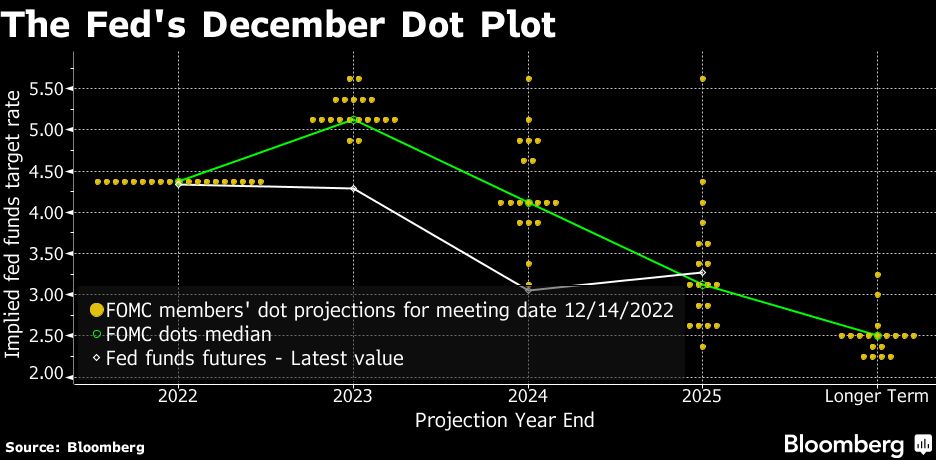

This will be my last letter of 2022. I want to use this letter as a set-up for my annual forecast issue the first week of January. That means we will touch on a variety of topics, kind of a snapshot into where my mind is today. Get ready to travel the world but let’s start at home with the Federal Reserve meeting this week.

This important milestone is the culmination of decades’ worth of research and lots of trial and error, and it makes good on the hope that humanity will one day enjoy 100% clean and plentiful energy.

Stephen Dover, Head of Franklin Templeton Institute, shares his scorecard on some market prognostications for 2022, and what his team is watching in 2023—from blockchain to balanced portfolios.

In part 1 I covered a model portfolio that was built on August 24, 2021, with the primary objective of generating a higher level of current income safely.

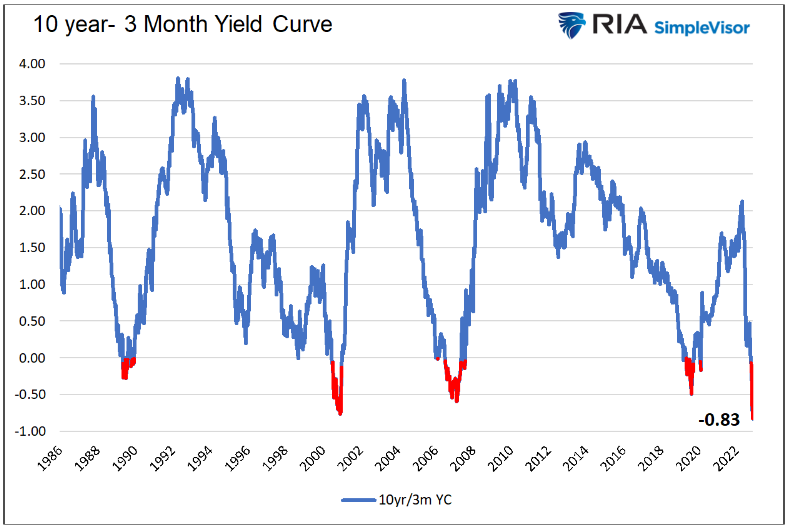

The financial foghorn is blowing. Historical odds greatly favor a recession, stock market drawdown, and a much lower Fed funds rate.

For investors trying to gauge levels of hawkishness at the Federal Reserve, Wednesday was an example of words carrying more weight than actions.

If you think high-yield savings accounts offer juicy rates to park some cash, wait until you see what money-market funds are paying.

U.S. stocks are solidly lower as the markets continue to digest the economic implications of yesterday's 50-bp rate hike from the Fed.

In our 2023 outlook, we outline three key themes for the new year and highlight several implementation solutions investors can use to navigate potential challenges and grow client portfolios in the new year.

The Federal Reserve downshifted its rapid pace of interest-rate hikes while signaling that borrowing costs, now the highest since 2007, will outstrip investors’ expectations as the central bank works to rein in inflation.

Starting in 2012, it became more and more difficult for prudent dividend growth stock investors looking for income.

In his latest memo, Howard Marks writes that the investment world may be experiencing the third major sea change of the last 50 years. Events in recent years – especially the spike in inflation and the Federal Reserve’s response – appear to have caused a reversal of the market conditions that prevailed after the Global Financial Crisis and for much of the last four decades. Howard discusses what this potentially new era could mean for lenders, especially bargain hunters.

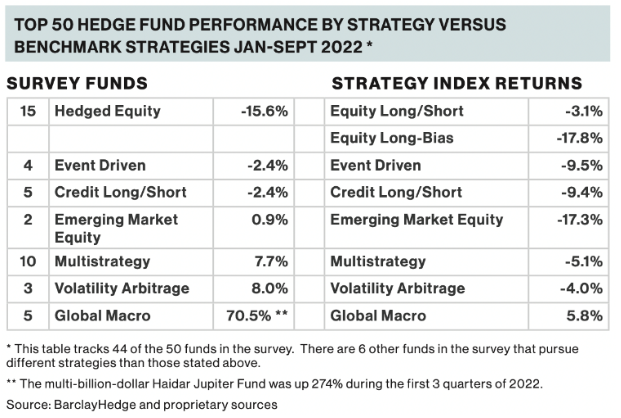

Global Investment Report's 3Q Update of the 2022 hedge fund survey.

Things are looking up for people who are close to retirement, according to a Morningstar report published Monday.

Professional speculators with billions in bearish trades on the line endured a rough ride after Tuesday’s report on US consumer prices brought the latest sign that the Federal Reserve is making progress in its battle against inflation.

The world’s biggest bond market got the ammo it needed from a below-forecast consumer price figure to fully lock in a Federal Reserve downshift in their policy-rate tightening pace, though not enough to wave an all clear sign for Treasuries.

Yield is set to be a more important component of total return for investors during the next few years as the “Fed Put” exerts less influence on markets.

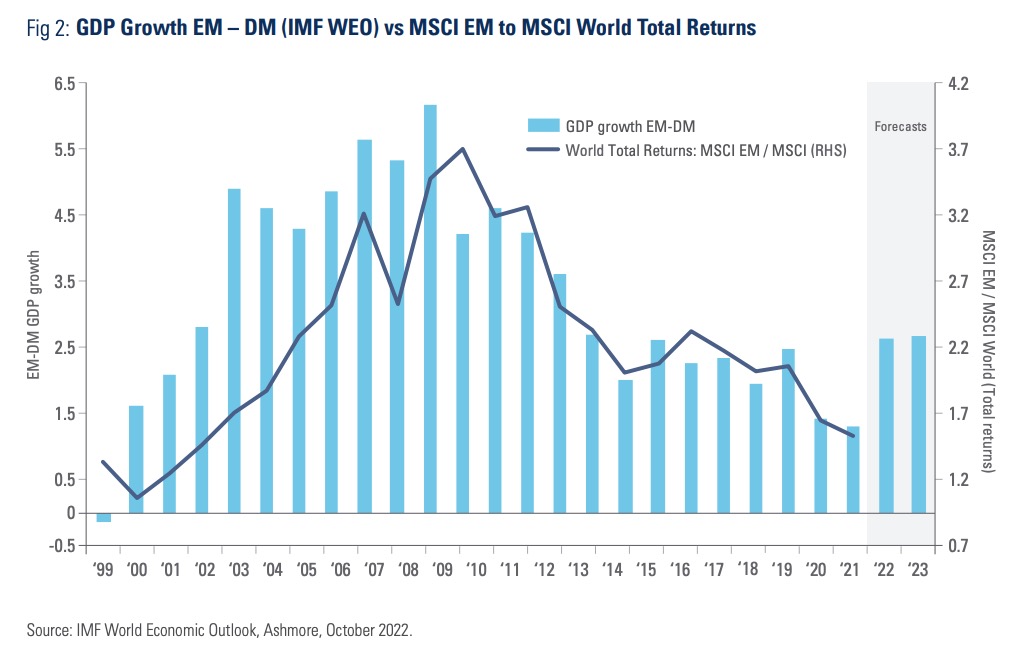

Emerging Markets (EM) assets were subject to three strong headwinds in 2022, namely, China’s zero Covid-19 and real estate crisis, aggressive interest rate tightening from the US Federal Reserve (Fed), and the Russia invasion of Ukraine.

The chorus of buy calls on government bonds is growing louder but BlackRock Inc. begs to differ.

U.S. stocks are soaring in pre-market trading amid a softer-than-expected November consumer price inflation report.